How soon will lower mortgage rates boost housing demand?

It is difficult to say for sure how long it will take before lower interest rates result in increased demand for real estate. However, there are some factors that may affect how quickly this happens.

One factor is the overall health of the economy. If the economy is strong, people are more likely to be confident about buying a home. This is because they are more likely to have a steady job and income.

Another factor is the availability of credit. If banks are willing to lend money to people with lower credit scores, this could make it easier for people to buy homes.

Finally, the cost of homes also plays a role. If the cost of homes falls, this could make them more affordable for people.

Overall, it is difficult to say how long it will take before lower interest rates result in increased demand for real estate. However, there are some factors that may affect how quickly this happens.

The Effects of Lower Interest Rates on the Real Estate Market

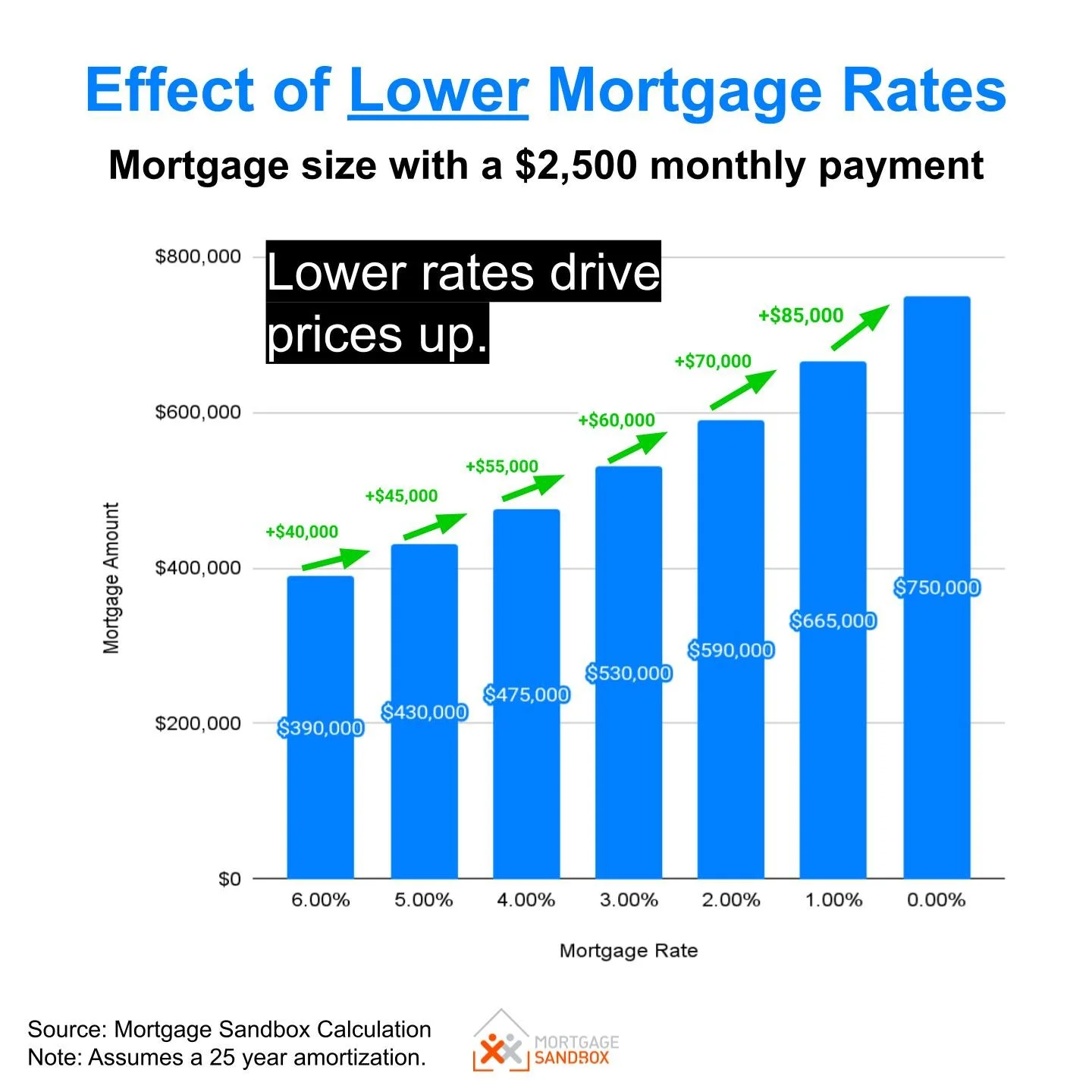

Lower interest rates can have a significant impact on the real estate market. When interest rates are low, it becomes cheaper for people to borrow money so they can qualify for bigger mortgages, which can lead to increased demand for homes. This can also lead to higher prices for homes, as sellers can demand more money for their properties.

There are a number of factors that can affect the relationship between interest rates and the real estate market. These include the overall health of the economy, the availability of credit, and the cost of homes.

The Overall Health of the Economy

One of the most important factors that affects the real estate market is the overall health of the economy. When the economy is strong, people are more likely to be confident about buying a home. This is because they are more likely to have a steady job and income.

When the economy is weak, people are more likely to be hesitant about buying a home. This is because they may be worried about losing their job or having their income reduced.

The Availability of Credit

Another important factor that affects the real estate market is the availability of credit. When banks are willing to lend money to people with lower credit scores, this can make it easier for people to buy homes.

When banks are less willing to lend money, it can make it more difficult for people to buy homes. This is because people with lower credit scores may not be able to qualify for a mortgage.

Another factor at play is the ability of banks to accumulate funds from depositors and investors to loan to homebuyers. Recently there have been a series of banking blowups in the U.S and Europe. While Canadian banks are perceived to be lower risk, with a recession on the horizon, they might further lower their risk profiles by lending less generously than in the past.

Mortgage originations (i.e., completions) reached a decade low in the last three months of 2022. With industry instability and the threat of a recession, there are very few compelling reasons for a dramatic turnaround in 2023.

The Cost of Homes

The cost of homes also plays a role in the real estate market. When the cost of homes falls, this can make them more affordable for people.

When the cost of homes rises, this can make them less affordable for people.

From a value below $600,000, house prices skyrocketed during the pandemic. The national benchmark house peaked at $954,900 in March 2022. While prices have dropped since mid-2022 to $781,300 in February 2023, they are still 30% higher than before the pandemic. Interest rates today, are much higher than before the pandemic so even though falling prices have priced some people back into the market, the vast majority of Canadians are priced out of the market.

Consumer Confidence

Falling prices have shaken Canadian’s faith in real estate as a low-risk and high-return investment.

While confidence has improved lately, it is still negative. Only 30% of Canadians believe home values will be higher in 6 months.

This not only spooks first-time homebuyers it has an even greater impact on investors. Investors can choose from all the available investments, including a savings account and investing in Google or Tesla.

Given the choices, and the current economic uncertainties, many would-be investors are choosing to put their cash somewhere other than real estate.

Summary

If you are considering investing in real estate, it is important to do your research and to consult with a financial advisor. You should also ensure you are comfortable with the risks involved with investing in real estate.

Lower interest rates can be a great opportunity to buy a home or invest in real estate. However, interest rates, the economy, and home values can fluctuate so it is important to be aware of the potential risks and benefits before making any decisions.