Canadian Mortgage Rate Forecast to 2028

Last updated:

The Bank of Canada is holding the line, but the cost of borrowing is poised to climb. Here is what buyers and owners ought to be doing now.

HIGHLIGHTS

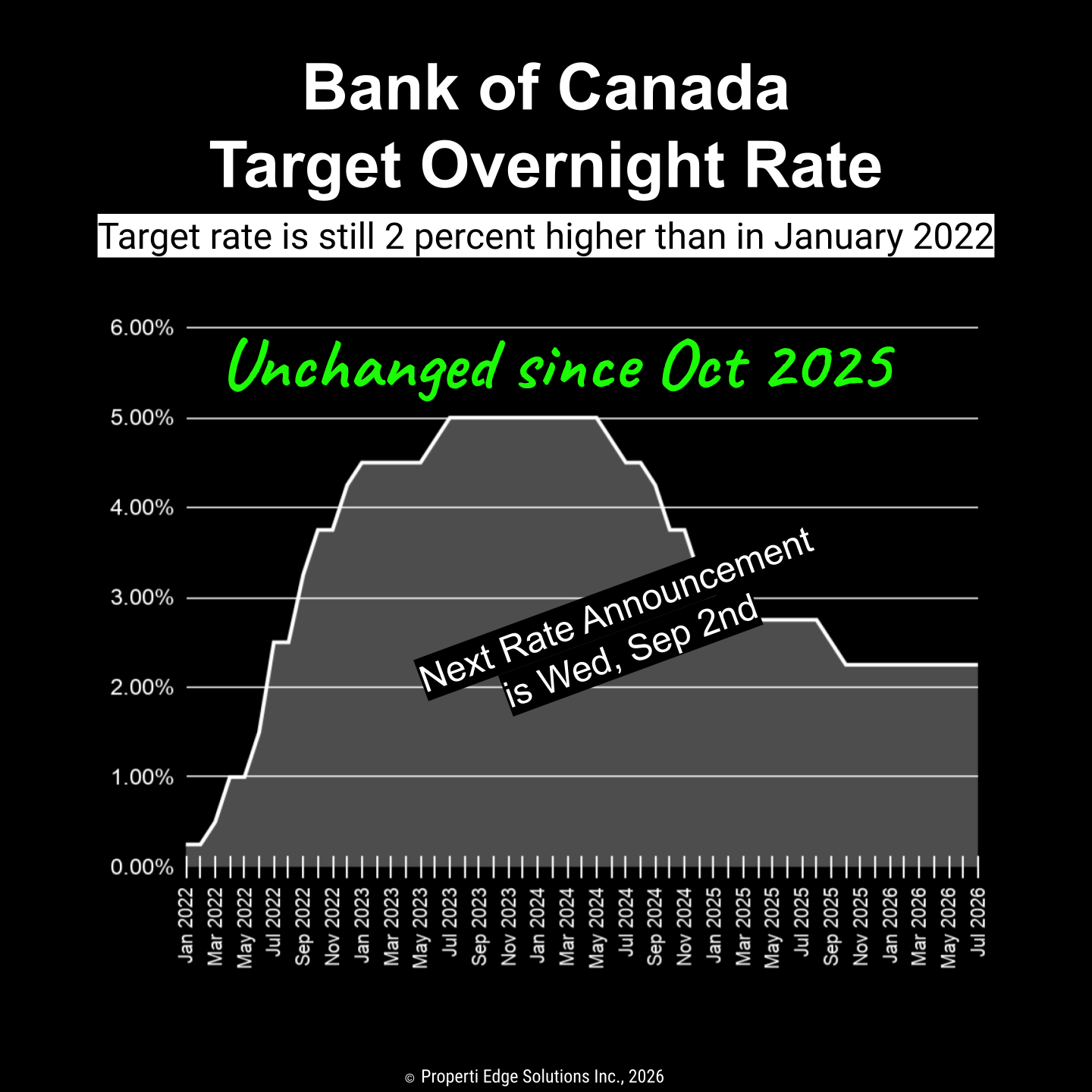

The pause holds, and the cuts are over. The Bank of Canada has again left its policy rate at 2.25 percent, judging the current setting appropriate to sustain the recovery and steer inflation back to 2 percent. The brisk easing of 2025 has run its course, and when the Bank next moves, the balance of risks tilts toward a hike rather than a cut.

A recovery taking hold, but slack remains. Growth has resumed after a choppy year, with second-quarter growth estimated at about 2½ percent. The Bank projects GDP growth of just 0.7 percent in 2026, firming to 1.8 percent in both 2027 and 2028. The labour market is still soft: unemployment was 6.5 percent in June and has hovered between 6½ and 7 percent since late 2024. That genuine economic slack gives the Bank room to look past a temporary inflation spike.

A geopolitical jolt to energy. Renewed and intensifying conflict in the Middle East, and Iran's threats to the Strait of Hormuz, through which roughly a fifth of the world's seaborne oil passes, has put a fresh risk premium into the market. Brent crude has climbed back above US$84 a barrel after a near-10 percent jump, though it remains well below its wartime peak of nearly US$120. A supply shock of this kind lifts headline inflation even as it weighs on growth, leaving the central bank little room to cut.

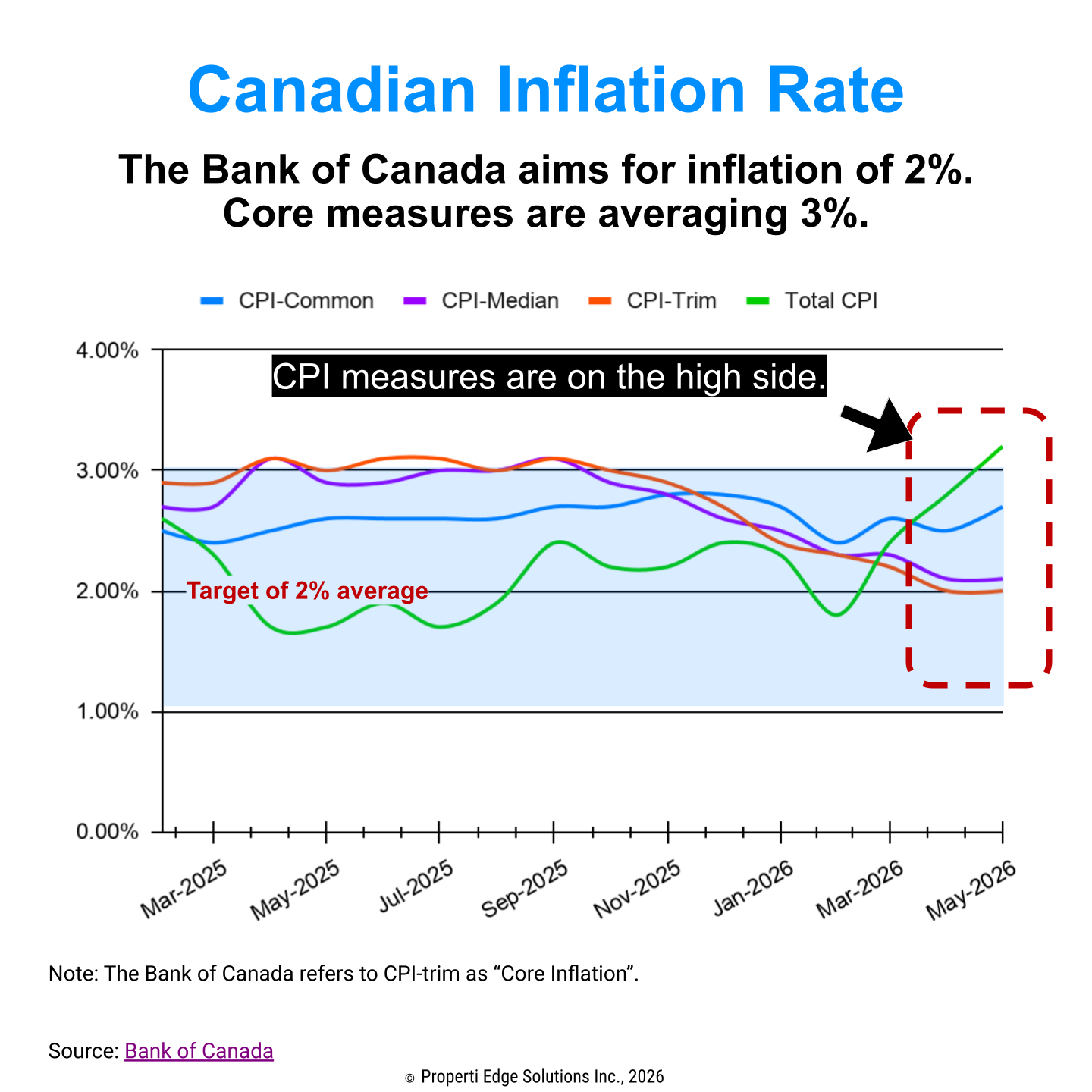

Inflation elevated, but expected to ease. CPI inflation rose to 3.2 percent in May, driven mainly by higher gasoline prices tied to the conflict. Stripping out gasoline, inflation was 2.2 percent and core measures stayed close to 2 percent. The Bank expects inflation to remain elevated in June before easing back toward 2 percent in early 2027. However, that path hinges on where oil and gasoline prices settle.

Trade uncertainty deepens. The United States has declined to extend CUSMA, which triggers fresh negotiations rather than ending the agreement. The deal does not expire until 2036., but because it was not extended it is now subject to annual reviews, and while this adds uncertainty, more businesses report finding ways to navigate it. Canada continues to diversify its trade relationships to reduce its exposure to U.S. policy swings.

The case for raising rates. Scotiabank now expects three increases in the second half of 2027, and TD notes markets have priced in at least one. Even if the Bank stands pat through the year, what National Bank calls "inflation-related anxiety" could force its hand in early 2027.

The case for cutting. The economy contracted late in 2025 and shed roughly 100,000 jobs early this year, and demand remains soft—a genuine argument against tightening. But the Bank answers first to its inflation mandate, and energy prices are tugging that number the wrong way. As well, recent employment numbers have been positive.

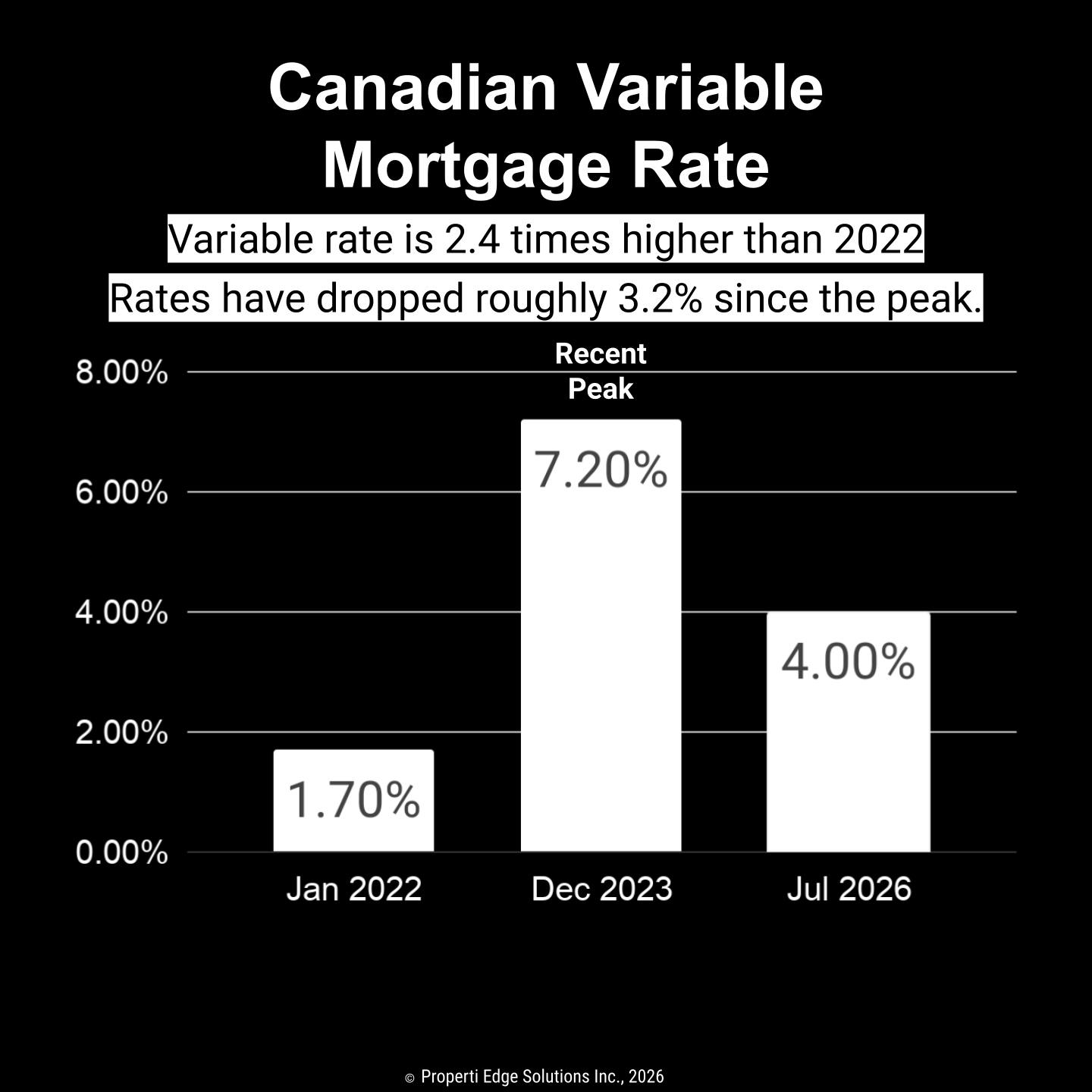

What it means for mortgages. Fixed rates have already climbed 0.35 to 0.40 percentage points since the conflict flared and are likely to hold firm or edge higher. Variable rates should stay put for a few more months before beginning to rise late in 2026. Barring a deep recession, a meaningful drop in mortgage rates is simply not in the cards.

Bank of Canada Overnight Rate

After a run of cuts through 2025, the Bank of Canada has stepped back to take stock, holding the policy rate at 2.25 percent. Attention has shifted to how quickly, and how convincingly, inflation can find its way back to the 2 percent target against an oil shock and an economy only now regaining its footing. CPI inflation rose to 3.2 percent in May, driven mainly by gasoline prices linked to the war in the Middle East, though excluding gasoline it was 2.2 percent and core measures held close to 2 percent.

Unlike 2022, the economy today carries genuine slack. Unemployment stood at 6.5 percent in June and has hovered between 6½ and 7 percent since late 2024, population growth has cooled, and demand is only gradually broadening. Growth has resumed after a choppy year and the Bank estimates second-quarter growth at about 2½ percent, but it projects GDP will expand just 0.7 percent in 2026 before firming to 1.8 percent in both 2027 and 2028. That slack gives the Bank latitude to look past a temporary inflation spike, and it expects inflation to ease back toward 2 percent by early 2027, provided oil and gasoline prices cooperate.

The risks, however, run in both directions. Should higher energy costs prove sticky and seep into core measures, the next move will be a hike. Trade adds a further layer of uncertainty: the United States has declined to extend CUSMA, triggering fresh negotiations and leaving the agreement subject to annual reviews, even as more businesses report finding ways to navigate the disruption. For Canadian borrowers, the era of falling rates has ended. The question is no longer whether rates will rise, but when, and by how much.

This forecast draws on the latest economic data and the published projections of major banks and credit unions, among them Desjardins, Scotiabank, National Bank, RBC and TD.

Fighting Inflation

Your mortgage rate in 2026 remains tethered to inflation. When inflation runs too hot, the Bank of Canada raises rates; the target inflation rate is 2 percent a year.

Headline inflation rose further to 3.2 percent in May, driven largely by higher gasoline prices linked to the war in the Middle East; excluding gasoline it was 2.2 percent and core measures held close to 2 percent.

Core inflation has been cooling, but the danger is that a drawn-out conflict keeps energy prices elevated long enough to push up wages and other costs. That is precisely the scenario that would compel the Bank to tighten, even with a weak economy at its back.

Canada's Trade Diversification: Progress and Friction

Canada is working to loosen its heavy reliance on the United States, and the effort has become more urgent as trade with Washington grows less predictable. The strategy is twofold: open new markets that give Canadian exporters genuine alternatives, and reduce the leverage any single partner can wield through tariffs and other pressure. The results so far are mixed. There is real progress on several fronts and persistent friction on others.

Where it is working. Following Prime Minister Mark Carney's January 2026 visit to Beijing, Canada entered a new strategic partnership with China and the two countries agreed to ease a series of restrictions. Canada opened its market to Chinese electric vehicles at a reduced 6.1 percent tariff within a set quota, while China cut its tariff on Canadian canola seed to roughly 15 percent, a steep reduction from punitive levels. Beyond China, Ottawa is pursuing investment deals with partners such as the United Arab Emirates and weighing a major defence procurement from Sweden. These arrangements that could reshape trade and investment flows and give Canadian firms new outlets for goods and capital.

Where conflict persists. The relationship that matters most remains the most unsettled. The United States has declined to extend CUSMA, triggering fresh negotiations rather than ending the deal, which does not expire until 2036. The U.S. Trade Representative said Washington "did not agree to renew" the agreement in its current form and would keep pressing to address what it calls shortcomings and trade deficits, while a senior administration official noted the president reserves the right to withdraw on six months' notice. Canada and Mexico had both wanted the deal extended and remain open to amendments, but the pact is now subject to annual reviews—a standing source of uncertainty for cross-border commerce. Some of Canada's new pivots also carry a cost: closer ties with China, the UAE and Sweden can create fresh friction with Washington, particularly ahead of the CUSMA talks.

Why it matters for rates and housing. Trade uncertainty feeds directly into the economic outlook the Bank of Canada must weigh. Tariffs and stalled negotiations dampen business investment and exports, while a broader set of trading partners can cushion the blow. Encouragingly, more businesses report finding ways to navigate the disruption. For borrowers, the upshot is that trade policy is now one more variable, alongside energy prices and inflation, shaping how quickly the economy recovers and where interest rates head next.

The Bank of Canada Rate Forecast: A Pause for Assessment

The Bank's posture is one of deliberate caution. The rapid easing of 2025 is over, and it has held the policy rate at 2.25 percent. The central bank is in wait-and-see mode, watching how the oil shock plays out across both inflation and growth. Governing Council judges the current rate appropriate to sustain the recovery and bring inflation back to the 2 percent target, and it has signalled that it is prepared to adjust policy as needed.

Its first task is to keep inflation expectations anchored. With CPI inflation up to 3.2 percent in May, energy prices sharply higher, and trade uncertainty still elevated, the Bank is in no mood to hint at future cuts. Indeed, several leading forecasters now expect the next move to be a hike.

Scotiabank anticipates three increases in the second half of 2026. TD notes that markets have priced in at least one. National Bank, while expecting no move in 2026, concedes that "inflation-related anxiety" could force tightening in early 2027. RBC sees the policy rate reaching 3.25 percent by the fourth quarter of 2027, and Scotiabank pencils in 3 percent, while most of the remaining forecasters look for two hikes, to 2.75 percent, beginning in 2027.

That said, the economy gives the Bank reason for patience. Growth stalled through a choppy year but resumed in the second quarter at an estimated 2.5 percent, and the Bank projects GDP growth of just 0.7 percent in 2026 before a firmer 1.8 percent in both 2027 and 2028. Unemployment, at 6.5 percent in June, points to genuine slack. If that slack keeps a lid on core prices and energy costs retreat, inflation is expected to ease back toward 2 percent by early 2027, and the case for hiking weakens.

The Bank has made plain that if inflation pressures reaccelerate, it stands ready to raise rates again even with growth subdued. Taken together, the balance of risks around the policy rate now tilts toward higher rates, not lower. The consensus, in short, is that rates are headed up.

5-year Government Bonds

The path of fixed mortgage rates is closely bound to the yield on the five-year Government of Canada bond. Those yields capture the market's expectations for growth, inflation and the central bank's next steps.

Since the latest flare-up with Iran, five-year yields have risen by 0.35 to 0.40 percentage points and remain well above pre-conflict levels, even after brief bouts of de-escalation steadied nerves. Most forecasts see yields holding in a range of 3.0 to 3.5 percent through 2026, with an upward bias. A prolonged conflict, or a fresh escalation that genuinely disrupts traffic through the Strait of Hormuz, could drive yields toward 3.75 percent or higher and lift five-year fixed mortgage rates directly. A sharp downside surprise on inflation, or an outright recession, could pull yields lower, but that is not the base case.

Sources

To build this analysis, we have surveyed the most prominent Canadian banks and their published forecasts.

Current Mortgage Rates in Canada

Recent Mortgage Rate Trends in Canada

Fixed Mortgage Rates

Fixed rates have already lifted off their 2025 lows and are unlikely to retreat. The best five-year fixed rates on offer today run from about 4.0 to 4.6 percent, depending on the lender and on insured status.

Looking ahead, most forecasts expect five-year fixed rates to hold near current levels or drift modestly higher. By the close of 2026, a typical five-year fixed rate could sit between 4.5 and 4.9 percent. By 2028, should inflation prove stubborn and the Bank deliver several hikes, fixed rates could approach 4.7 to 5.1 percent. A return to rates below 4 percent would require a recession, which is not expected under present conditions.

Variable Rates

Variable rates move in lockstep with the Bank of Canada's policy rate. With the Bank at 2.25 percent, most variable mortgages are priced at prime minus a discount, leaving effective rates in the neighbourhood of 4.00 to 4.50 percent.

Canada is at or near the floor of this interest rate cycle. The Bank is unlikely to cut again unless the economy deteriorates sharply. The more probable path is a stretch of no change, followed by hikes starting late in 2026. By the end of 2027, variable rates could be 1.00 to 1.50 percentage points above today's levels.

Impact of Rates on Homebuyer Budgets

Impact of Rates on Homebuyer Budgets

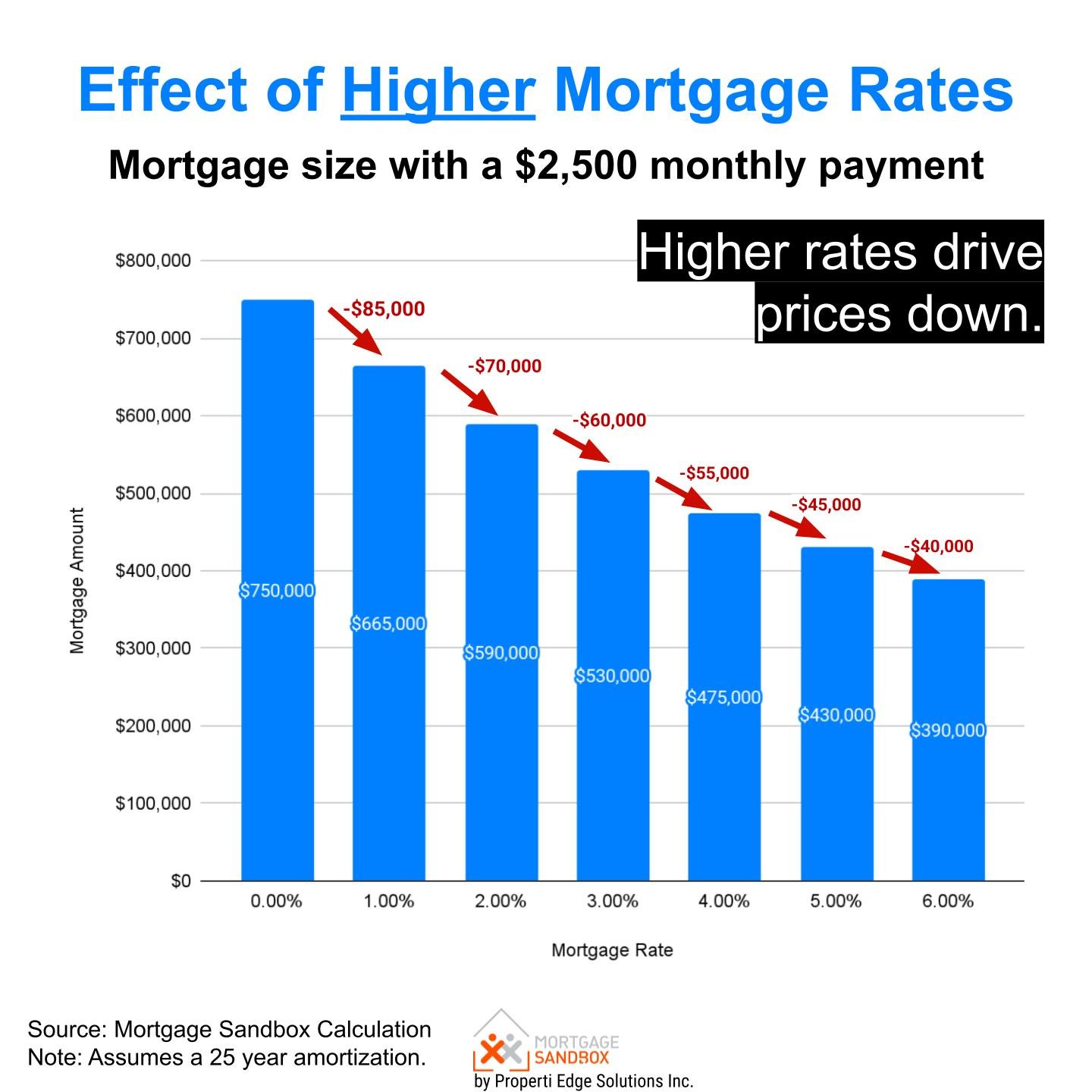

A one-percentage-point increase in the interest rate trims purchasing power by roughly 10 percent for a given monthly payment. With rates expected to be higher 12 to 18 months out, many would-be buyers will find themselves priced out of homes they could comfortably afford today.

The consequence will be either fewer purchases or meaningful price declines, as listings linger longer than sellers care to wait. It typically takes about 18 months for a change in rates to work its way fully through the housing market, shaping both prices and buyer behaviour. If you intend to buy, it is worth weighing your timing carefully before rates climb further.

Need a mortgage refinance?Talk to one of our affiliated Mortgage Brokers Powered by Properti Edge |

Mortgage Rate Predictions Through 2028

Will the 5 year fixed rate fall further?

Unlikely on the current outlook. Fixed rates track the five-year Government of Canada bond yield, which has climbed 0.35 to 0.40 percentage points since the Middle East conflict flared. With bond markets having absorbed the Bank's rate pause and inflation still elevated, the base case is for fixed rates to hold near today's levels or drift modestly higher. Only a sharp downturn in growth and employment would move them materially lower, and that is not expected.

How much further will variable rates drop?

On what we know today, very little. Variable mortgage rates track the Bank of Canada's policy rate closely. With the Bank on hold and inflation risks tilted upward, it will not cut again short of a deep recession. The risk profile has flipped: further cuts are now a remote prospect, while rate hikes are the more probable outcome for 2027 and 2028.

Try our mortgage offer comparison tool to calculate the dollar difference (not percent) between two offers. Find out how much cash you’ll save with a lower rate and the potential fees that come with different choices.

Fixed vs. Variable: Which is better now?

The case for fixed. A five-year fixed rate buys predictability at a moment of unusual uncertainty. It shields you from future increases over a meaningful horizon and makes budgeting straightforward. With fixed rates already higher but still below where they could land if the Bank hikes repeatedly, locking in today's rate is a reasonable choice for anyone who values certainty.

The case for variable. A variable rate typically starts lower—currently about 0.50 percentage points below fixed. The trade-off is accepting the risk that payments rise if inflation lingers and the Bank tightens. This suits borrowers with strong cash flow and room to manoeuvre. Most analysts, however, believe the policy rate is near the bottom of the cycle. Absent a recession, variable rates are likely to stay flat rather than fall, and if they do rise, the gap with fixed rates will close in a hurry. Two hikes would push the variable rate above the five-year fixed rate you could lock in today.

A strategic middle ground. A three-year fixed term remains an appealing compromise. It offers medium-term stability while keeping you closer to the point at which the rate path comes into clearer focus. By a 2029 renewal, there should be far better visibility into how the conflict with Iran, trade policy and economic growth have unfolded.

Pros and cons of a 5-year fixed-rate mortgage

The case for fixed. A five-year fixed rate buys predictability at a moment of unusual uncertainty. It shields you from future increases over a meaningful horizon and makes budgeting straightforward. With fixed rates already higher but still below where they could land if the Bank hikes repeatedly, locking in today's rate is a prudent move for anyone who values certainty.

The case for variable. A variable rate typically starts lower, currently about 0.50 percentage points below fixed. The trade-off is accepting the risk that payments rise if inflation lingers and the Bank tightens. This suits borrowers with strong cash flow and room to manoeuvre. Most analysts, however, believe the policy rate is near the bottom of the cycle. Absent a recession, variable rates are likely to stay flat rather than fall, and if they do rise, the gap with fixed rates will close in a hurry. Two hikes would push the variable rate above the five-year fixed rate you could lock in today.

A strategic middle ground. A three-year fixed term remains an appealing compromise. It offers medium-term stability while keeping you closer to the point at which the rate path comes into clearer focus. By a 2029 renewal, there should be far better visibility into how the Middle East conflict, trade policy and economic growth have unfolded.

Not sure you've been offered a good renewal rate?Try our mortgage offer comparison tool Powered by Properti Edge |

Pros and cons of a variable rate mortgage

Lower opening rate. Variable rates usually start below fixed rates, which can save money up front.

Payments ease when rates fall. If the Bank lowers its policy rate, your interest costs, and often your payment, will fall with it.

A gentler penalty to break. Penalties for breaking a variable-rate mortgage are typically capped at three months' interest, often far less than the IRD penalty on a fixed term.

Payment uncertainty. With an adjustable-rate mortgage, your monthly payment can rise whenever the Bank hikes. With a standard variable-rate mortgage, the payment may hold steady, but a larger share goes to interest, stretching out your amortization. Make sure your budget has the flexibility to absorb higher costs.

Exposure to inflation. Your borrowing cost is tied directly to the central bank's response to inflation. Persistent inflation means higher rates and higher payments. The settled low-inflation years of 2010 to 2020 are behind us.

Not sure you've been offered a good deal?Try our mortgage offer comparison tool Powered by Properti Edge |

How to Get the Best Mortgage Rate

Start early and use a broker: Reach out to an accredited mortgage broker roughly 120 days before your closing or renewal. Brokers have access to many lenders and can negotiate on your behalf. If your current lender senses you are shopping around, it will often sharpen its offer to keep you.

Negotiate your discount: On variable rates, the posted "prime minus" discount is frequently negotiable. Do not settle for the first number. Be aware, too, that not every bank ties its variable-rate mortgages to the Bank of Canada's prime rate. Some, including TD Bank, use their own internal prime rate, which they control and which often sits higher.

Consider more than the rate: The interest rate matters, but so do the terms of the contract, among them prepayment privileges, portability and how penalties are calculated, particularly on fixed terms.

Further Reading: Our mortgage renewal guide that will help you navigate the process.

Is it a better time to buy or sell a home?

The higher-rate climate has cooled many Canadian markets and all but ended the bidding wars that defined the earlier part of the decade.

Advice for Homebuyers

Your purchasing power is set by today's rates, not by the cheap-money days of 2020. Be honest about your budget and secure a solid pre-approval to hold a rate while you shop. Concentrate on homes you can comfortably carry under the stress test rather than stretching to the very limit.

Bear in mind that the bank will qualify you for an amount it believes will keep you out of bankruptcy, not for a payment you will find comfortable. Lenders will let mortgage payments consume close to 40 percent of your income. With another 40 percent or so going to taxes, that leaves roughly 20 percent of your pre-tax earnings for food, transportation, entertainment, daycare and the occasional holiday. Borrowing to the maximum can leave you house-rich and life-poor.

Advice for Home Sellers:

The days of list it and watch it sell are gone. Pricing your home correctly from the outset is now essential to drawing serious buyers. Work with an agent who understands how today's financing costs are shaping demand in your neighbourhood. Well-presented, fairly priced homes are still moving; overpriced ones are sitting.

Like this report? Like us on Facebook.

|

Do you have a financing strategy?Try our our Financing Strategy Explorer Powered by Properti Edge |

Canadian Real Estate Forecasts

Toronto

Real Estate Trends and Forecast

Montreal

Real Estate Trends and Forecast

Hamilton-Burlington

Real Estate Trends and forecast

Victoria

Real Estate Trends and Forecast

Vancouver

Real Estate Trends and Forecast

Ottawa

Real Estate Trends and forecast

Calgary

Real Estate Trends and Forecast

Edmonton

Real Estate Trends and Forecast

London, ON

Real Estate Trends and Forecast

Okanagan Valley

Real Estate Trends and Forecast

Like this report? Like us on Facebook.