Metro London, Ontario

Real Estate Trends and Price Forecast

HIGHLIGHTS

Metro London home values have been trending downward over the past year.

Multi-factor analysis identifies Metro London as a moderate-risk real estate market.

Mortgage rates have eased from their peak, but remain high relative to the 2010–2020 average, limiting buyer budgets.

Economic uncertainty is rising due to Canada’s immigration policy shift and the Trump administration’s tariffs, which could further weigh on the market.

This article covers:

What is the state of the London property market?

Where are prices headed?

Should investors sell?

Is this a good time to buy?

1. What is the state of the London property market?

London Ontario Property Market Overview

Metro London, Ontario has a population of approximately 500,000 and is a growing city known for its strong economy and vibrant community.

Thriving Job Market: London benefits from a diverse economy with strengths in healthcare, education, manufacturing, and technology. With a mix of large employers like the London Health Sciences Centre and Western University, the city offers a wide range of job opportunities.

High Quality of Life: Known for its affordable cost of living and family-friendly atmosphere, London consistently ranks as one of the best places to live in Ontario. The city offers a mix of urban amenities with a relaxed, small-town feel.

Access to Nature: London is rich in parks, gardens, and green spaces, such as the Thames River, Victoria Park, and the nearby Fanshawe Conservation Area. Outdoor enthusiasts enjoy a variety of recreational activities year-round.

Education Hub: As home to Western University and Fanshawe College, London offers excellent educational opportunities, making it an attractive destination for students and academics.

Cultural & Historical Appeal: London boasts a vibrant arts scene, with numerous galleries, theatres, and music festivals, alongside a rich history that includes landmarks such as the Banting House National Historic Site.

Diverse & Growing Community: London’s multicultural atmosphere is reflected in its many cultural events, restaurants, and local markets, making it a welcoming and inclusive city for newcomers.

Efficient Transportation: London’s public transportation system is well-connected and continues to grow, with ongoing infrastructure improvements, including expanded bike lanes and better connectivity between key areas.

London’s housing market clearly favours buyers, with negotiating power shifting further in their direction as supply has thickened. Inventory has risen over the past year, giving buyers more choice, while typical home values have held steady in recent months, signalling a period of price stability rather than sharp declines or rebounds. This combination of stronger supply and flat prices points to a market where buyers can take their time and negotiate firmly without fearing rapid upward pressure on values.

The real estate statistics for Metro London include St. Thomas, Middlesex, and Elgin Counties.

Metro London Detached House Prices

Detached houses are also in a buyer’s market, with conditions tilting further toward purchasers as available supply has grown. Buyers benefit from more listings to choose from, and recent softening in both benchmark and median detached prices shows sellers becoming more flexible on price. Together, increased inventory and modest price declines suggest that buyers looking for detached homes can secure better terms than they could earlier, especially if they are patient and selective.

We believe politicians are implementing policies to guide the market toward a typical annual real estate cycle with price growth of 1 to 3% annually, in line with income growth.

Metro London New Construction Home Prices

Prices of new homes are dropping. Some homeowners in new developments who bought pre-sales in 2022 might find they will have paid much more than their new neighbours. Based on economic fundamentals, this trend is likely to continue.

Does this concern you? Read the Pros and Cons of Buying Pre-sale Homes

Construction activity is in a typical range and should be absorbed without major price disruption, and easing borrowing costs are gradually supporting demand; however, in a smaller market, it can take time for lower rates to translate into stronger sales and firmer prices.

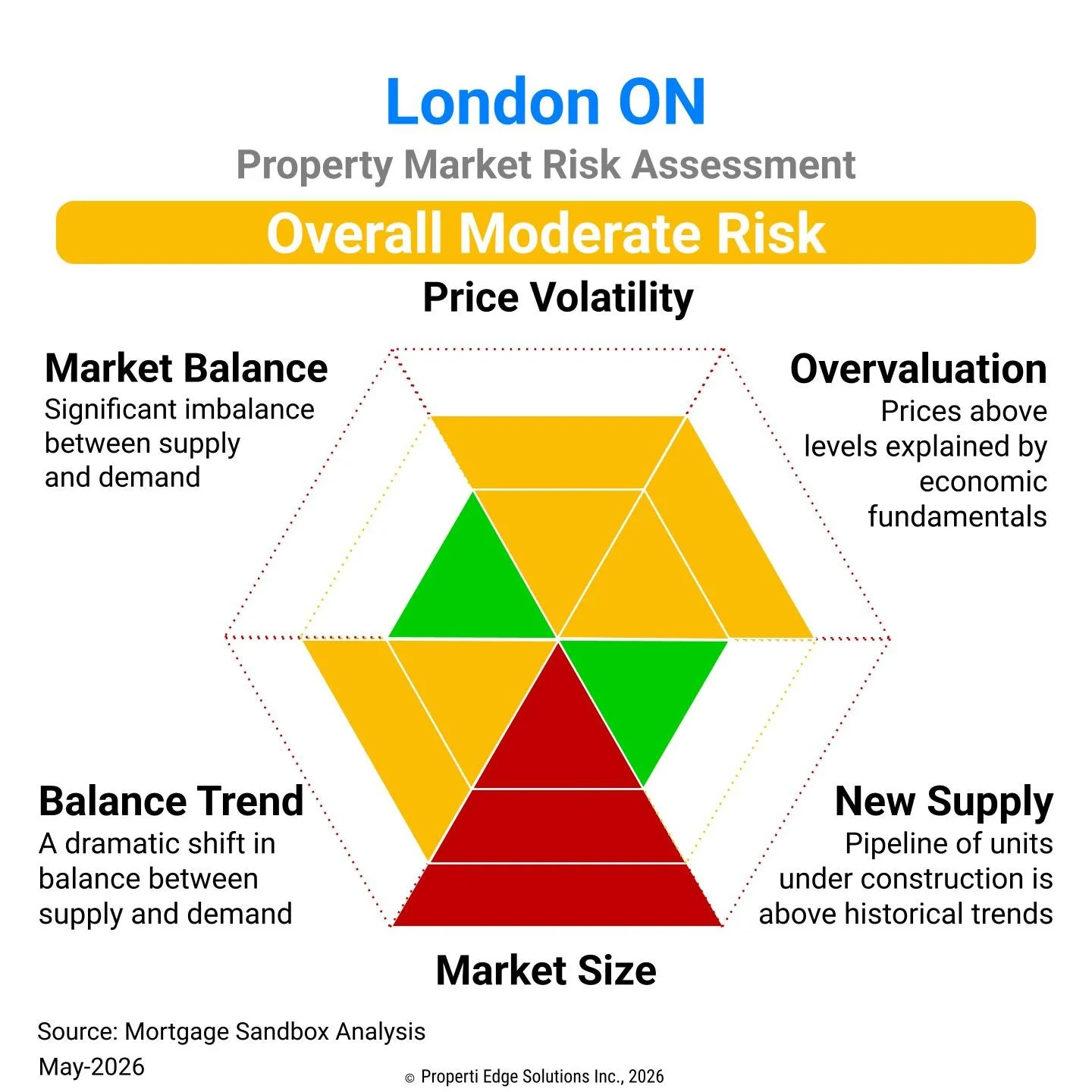

Market Risk

Based on Mortgage Sandbox Analysis, London is at moderate risk of a significant market correction.

London’s market sits at a moderate risk level, reflecting the tension between ample supply, relatively high prices versus local incomes, and a smaller buyer pool. While prices have been stable overall, affordability pressures suggest some properties could be priced above what many local buyers can comfortably pay, and sellers may struggle to find purchasers in slower periods.

Need a great local Realtor?

Our app matches you with local pre-screened, values-aligned agents.

Metro London Condo Apartment Prices

The condo segment remains a buyer’s market as well, but with supply conditions broadly similar to last year rather than dramatically looser. Even without a major shift in inventory, recent declines in both benchmark and median condo prices indicate that buyers are gaining leverage through pricing instead of sheer choice. This environment allows condo buyers to negotiate meaningful discounts, particularly on units that have been sitting on the market longer.

With more people working-from-home, we expect developers will begin marketing larger (i.e., 2 and 3 bedrooms) apartments to meet buyer preferences. As the supply of more generous floor plans comes to the market, it may depress the values for small floor plan condos.

At Mortgage Sandbox, we would like developers to build 4 and 5 bedroom condos because:

Not everyone can afford to buy a house for their family.

Canadians who now work from home need more room to segregate workspace from living space within their homes.

Many Canadians with longer working hours find it challenging to stay on top of necessary house upkeep (i.e., mowing lawns, clearing eaves, shovelling sidewalks).

Many people prefer to live in higher-density neighbourhoods with all the essential amenities within walking distance.

Metro London Townhouse Prices

Still a challenge for first-time homebuyers

London house prices have become much less affordable. A homebuyer household earning $75,500 (the median Metro London household before-tax income) can get a $310,000 mortgage. That’s enough to buy a benchmark condo, but buying a house is out of reach for more than 70% of locals.

Houses are for the rich, but most of the land is zoned for single-family detached houses. 🤔

What about other parts of Ontario?

Read the Toronto Forecast, Ottawa Forecast and the Hamilton Forecast.

1. Where are prices headed?

There is a lot of uncertainty in the forecasts for looking out toward 2027. Many of the forecasters we've surveyed have different expectations for:

Will the federal government’s recent migration policy pivot lead to a shrinking population?

Will mortgage rates drop to the 2 to 3 percent range that Canadians have grown used to?

Will Canada’s trade wars with China and the United States lead to a recession?

How do we arrive at our forecast range? Check out our full assessment of the five factors that drive these forecasts. These five forces help explain why several forecasters are anticipating price drops.

Break up with your Realtor?

Our FREE app Matches you with local agents who are predisposed to work well with you!

At Mortgage Sandbox, we provide a price range rather than attempting a single prediction because many real estate risks can impact prices. Risks are events that may or may not happen. As a result, we review various forecasts from leading lenders and real estate firms, and we then present the most optimistic estimates, the most pessimistic prediction, and the average forecast.

Do you want to learn more about real estate risk? We've written a comprehensive report explaining the uncertainty level in the Canadian real estate market.

Our forecast inputs:

Mortgage Renewal?

Refinance?

Our platform helps you find local pre-screened mortgage brokers.

3. Is this a good time to sell an London property?

From a seller’s perspective, more changes in the market influence prices downward, so this year may be a better time to sell than in two years.

The annual real estate cycle usually favours sellers in the first half of the year.

Sellers should always consult a mortgage broker early to prioritize flexible loan conditions and reduce the risk of mortgage cancellation penalties. Find out more about the benefits of a mortgage broker.

Planning to Sell? Check out our Complete Home Seller’s Guide.

Fixed or Variable rate mortgage?

Find out where mortgage rates are headed before you start to negotiate.

4. Is this a good time to buy a London home?

Prices have been stable or declining, and supply is high, suggesting prices could drop further. While mortgage rates are currently high, they are trending downward. Additionally, the typical annual real estate cycle generally favours buyers during late summer and autumn.

These factors may lead potential buyers to believe that waiting until later in 2025 or 2026 could provide better purchasing opportunities than buying now.

While it's nearly impossible to perfectly time the market, if you are looking to buy your forever home and plan to stay for at least ten years, the risks of purchasing now are lower than they were a year ago.

If you are considering a home purchase, make sure to negotiate firmly and aim to pay close to the market value. Also, be cautious not to overextend yourself financially.

Planning to Buy? Check out our Complete Home Buyer’s Guide so we can walk you through the end-to-end process and get you ready to buy your new home!

How much home can you afford?

Our mortgage calculator takes uses up-to-date mortgage rates and calculates the price of a home you could afford.

Here are some recent headlines you might be interested in:

Canada’s GDP growth likely turned positive in Q1 after Q4 contraction (RBC | May 22)

Spring housing market sees slow rebound as prices edge up (MSN | May 19)

London home sales dip again, new figures show, forcing sellers to adapt (London Free Press | May 05)

Home sales jump in London region in March, prices continue to rise (CTV News | Apr 26)

Rate cuts seen as more likely next move for Bank of Canada: TD (Canadian Mortgage Trends | Apr 26)

Mortgages in arrears in Canada – what the numbers mean (Canadian Bankers Association | Apr 26)

Canadian Home Prices Fall 16th Straight Month on Higher Rates (Bloomberg | Apr 26)

Bank of Canada set to hold rates at 2.25% as oil shock likely short-lived (Reuters | Apr 26)

Market Outlook: Bank of Canada may cut rates despite hike expectations (BNN Bloomberg | Apr 26)

Like this report? Like us on Facebook.