Metro Hamilton

Real Estate Trends and Price Forecast

HIGHLIGHTS

Metro Hamilton home values have been moderately volatile since 2021 and are now gently trending downward as the market normalizes going into 2027.

The Metro Hamilton housing market is now a balanced market, with buyers and sellers having similar negotiating power and inventory gradually shifting conditions in favour of buyers.

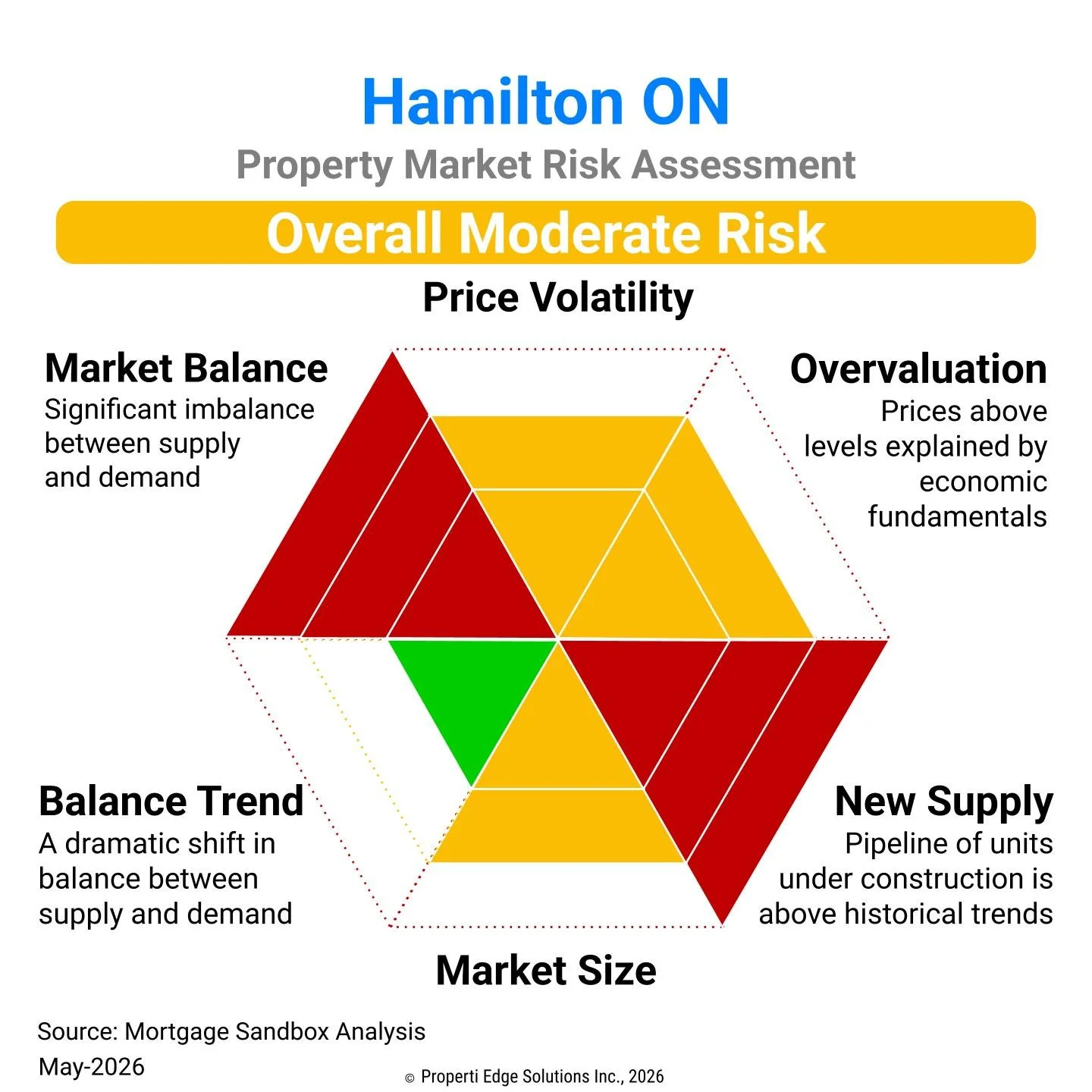

Multi‑factor analysis identifies Metro Hamilton as a moderate‑risk real estate market, with elevated valuations relative to incomes and above‑normal construction levels.

Mortgage rates are easing but are expected to trend higher; they currently support buyers' budgets but have not yet translated into strong price growth.

Economic uncertainty remains elevated due to immigration policy shifts and U.S. tariffs and trade tensions, which could continue to weigh on the market outlook through 2028.

This article covers:

What is the state of the Hamilton property market?

Where are prices headed?

Should investors sell?

Is this a good time to buy?

1. What is the state of the Metro Hamilton property market?

Hamilton Property Market Overview

Metro Hamilton, Ontario, has a population of approximately 600,000 and is a dynamic city known for its industrial heritage, growing economy, and vibrant cultural scene.

Thriving Job Market: Hamilton has undergone a significant economic transformation in recent years. While its economy was once heavily reliant on steel and manufacturing, it now boasts a diverse job market, including strengths in healthcare, education, technology, and the arts. With major employers like Hamilton Health Sciences and McMaster University, job opportunities are on the rise.

High Quality of Life: Hamilton offers an affordable cost of living compared to other major Ontario cities, making it an attractive option for families and young professionals. The city is known for its close-knit communities and a balance of urban amenities and access to nature.

Access to Nature: Often referred to as the "City of Waterfalls," Hamilton is surrounded by natural beauty, with over 100 waterfalls, extensive hiking trails, and the scenic Niagara Escarpment. The city's parks and proximity to the waterfront provide ample opportunities for outdoor activities year-round.

Education Hub: Home to McMaster University, one of Canada’s top universities, and Mohawk College, Hamilton is a center of higher education and research, offering numerous opportunities for students and professionals looking to advance their education.

Cultural & Historical Appeal: Hamilton boasts a growing arts and culture scene, with vibrant music venues, galleries, and annual festivals. The city’s history as an industrial powerhouse is reflected in its unique architecture and museums, including the Canadian Warplane Heritage Museum and the Royal Botanical Gardens.

Diverse & Expanding Community: Hamilton's multicultural population is reflected in its diverse neighbourhoods, restaurants, and cultural festivals. The city’s inclusivity and welcoming atmosphere make it a great place for newcomers from all walks of life.

Efficient Transportation: Hamilton is well-connected by public transportation, with an expanding light rail transit (LRT) system in development and easy access to major highways, making commuting to nearby cities like Toronto and Niagara Falls convenient.

Overall, Hamilton offers a thriving job market, a strong sense of community, a rich cultural landscape, and abundant green spaces, making it an ideal city for families, students, and professionals seeking a balanced and affordable lifestyle.

Statistics Canada defines Metro Hamilton as the cities of Hamilton, Burlington, and Grimsby.

Metro Hamilton home values have been volatile since 2021 and, going into 2026, are gently trending downward as the market normalizes. The outlook for 2028 points to a cooler, more balanced environment where buyers and sellers have similar negotiating leverage, though conditions are slowly tilting toward buyers.

Metro Hamilton Detached House Prices

The Metro Hamilton detached house segment now reflects a balanced market, with buyers and sellers negotiating on more equal footing and supply gradually becoming more favourable to buyers. Months of inventory have been edging higher compared with last year, indicating that listings are taking longer to sell and that buyers have more choice.

Detached benchmark prices have been easing slightly in recent months, showing a mild downward drift that favours buyers rather than the rapid swings seen earlier in the decade. Median detached values are also softening, suggesting that typical buyer budgets are under pressure and that sellers must be realistic about pricing. Going into 2026, detached homes are expected to trade within a relatively narrow range, with gentle downside or flat conditions more likely than a renewed surge.

We believe politicians are implementing policies to guide the market toward a typical seasonal real estate cycle with modest price growth over the long run in line with income growth. Demand in Hamilton remains constrained by affordability: many people still aspire to buy a home, but budgets are stretched, and borrowing capacity is limited. New homebuyers continue to struggle to get onto the first rung of the ladder, while move‑up buyers often cannot qualify for larger mortgages under current lending standards. At the same time, the total number of active detached listings is trending higher than in recent years, and this additional supply is expected to keep conditions balanced to slightly buyer‑friendly into 2027.

Demand (i.e., purchases) in Hamilton is low. Many people want to buy a home, but affordability is so poor that would-be buyers have been sidelined.

New homebuyers can’t afford to get on the first step of the homeownership ladder, and households who want to climb the next rung (i.e., upgrade to a larger home) can’t qualify for a new mortgage at the current rates.

Meanwhile, the total active listings are trending upward. They are at their highest level in three years.

Hamilton-Burlington New Construction Home Prices

The prices of new homes are currently under downward pressure and are softening as inventory works its way through the market. Some buyers in newer developments who committed to purchasing at peak prices may notice that subsequent buyers in similar projects are paying less or receiving more incentives. Based on economic fundamentals, this trend of decreasing new home prices is expected to continue as the market adjusts to elevated construction levels and developers compete for a limited pool of buyers.

As a pre-sale buyer, it is important to negotiate for meaningful discounts or added value, as developers may be more willing to negotiate than they were in the past.

Does this concern you? Read the Pros and Cons of Buying Pre-sale Homes

While the market is softening and new construction starts have begun to slow, the existing pipeline is expected to provide a steady supply of new homes through 2027.

Market Risk

Based on Mortgage Sandbox analysis, Hamilton remains at a moderate risk of a market correction.

Prices have shown moderate volatility rather than stability, reflecting shifts in rates, policy, and sentiment over the past few years.

Valuations remain high relative to local incomes, which means a meaningful portion of the housing stock could still be overvalued if economic conditions worsen.

Construction activity has been running well above normal levels, raising the likelihood of market absorption challenges and prompting developers to consider price discounts or bonus amenities to attract buyers.

Metro Hamilton is a mid-sized market with an average buyer pool. In a slower market, sellers may find it more challenging to attract buyers than a seller in Toronto, even with a well-priced listing.

Currently, interest rates are relatively low due to the easing phase of the rate cycle, leading to a decline in borrowing costs. This gradual decrease boosts purchasing power and often stimulates property markets. However, it may take considerable time for the full effects of lower rates to translate into actual sales and prices. As well, current rates are still well above the average from 2008 to 2021.

Need a great local Realtor?

Our app matches you with local pre-screened, values-aligned agents.

Metro Hamilton Condo Apartment Prices

After breaking records during the pandemic, Metro Hamilton apartment prices have flattened and, more recently, begun to drift lower. The condo apartment benchmark has been moving down in favour of buyers over the past several months, signalling softer demand and increased negotiating room for purchasers. At the same time, typical (median) condo values have been holding relatively steady, suggesting that while higher‑priced units are under more pressure, more modestly priced units are seeing firmer underlying support.

With more people working from home, we expect developers to continue pivoting toward larger floor plans to meet evolving buyer preferences. As the supply of bigger units comes to market, values for smaller condos could face additional downward pressure. At Mortgage Sandbox, we would like developers to build four-bedroom condos because not everyone can afford a house, remote workers need more space, busy Canadians often prefer low‑maintenance living, and many people value higher‑density neighbourhoods with key amenities within walking distance.

Metro Hamilton Townhouse Prices

Still a challenge for first-time homebuyers

It is still quite challenging for first-time homebuyers in Hamilton. The city's housing prices have become much less affordable. A household with a first-time homebuyer earning $91,000 (the median before-tax income in Metro Hamilton) can secure a $320,000 mortgage. With a $80,000 down payment, they would only be able to purchase a home valued at $400,000. However, the benchmark price for a condo apartment is over $500,000. This means that in order to buy a typical condo apartment, a household would need to receive an inheritance or a very generous gift from family, which is not feasible for most people.

How much home can you afford?

Our mortgage calculator takes uses up-to-date mortgage rates and calculates the price of a home you could afford.

What about the rest of Canada?

Read the Toronto Forecast, London Ontario, Montreal Forecast and the Vancouver Forecast.

2. Metro Hamilton House Price Forecast

There is considerable uncertainty in the outlook through 2028. Many of the forecasters we follow hold different views on how key drivers will evolve over the next couple of years. There are open questions about how much the federal government’s immigration policy pivot will eventually slow population growth. There is also uncertainty about how far mortgage rates will fall in this easing cycle and whether they will return to the very low levels that households became accustomed to earlier in the decade. In addition, trade tensions and global economic risks raise the possibility of slower growth or even recession, which would weigh on both incomes and housing demand.

Break up with your Realtor?

Our FREE app Matches you with local agents who are predisposed to work well with you!

How do we arrive at our forecast range? Check out our full assessment of the five factors that drive these forecasts. These five forces help explain why several forecasters continue to anticipate either flat prices or mild declines over the coming years, rather than a rapid re‑acceleration.

At Mortgage Sandbox, we provide a price range rather than attempting a single prediction because many real estate risks can impact prices and may or may not materialize. As a result, we review various forecasts from leading lenders and real estate firms and then present the most optimistic estimates, the most pessimistic predictions, and the average forecast.

Do you want to learn more about real estate risk? We have written a comprehensive report explaining the level of uncertainty in the Canadian real estate market.

Our forecast inputs:

3. Is this a good time to sell a Hamilton property?

From a seller’s perspective, the directional forces in the market currently lean toward softer prices rather than significant appreciation, so selling in the near term may be more favourable than waiting several years.

In a balanced market, well‑presented and correctly priced properties can still attract solid interest, but sellers need to be realistic and prepared for more negotiation.

The typical annual real estate cycle usually favours sellers in the first half of the year, when buyer activity tends to be seasonally stronger.

Sellers should always consult a mortgage broker early to prioritize flexible loan conditions and reduce the risk of mortgage cancellation penalties. Find out more about the benefits of a mortgage broker.

Planning to Sell? Check out our Complete Home Seller’s Guide.

Fixed or Variable rate mortgage?

Find out where mortgage rates are headed before you start to negotiate.

4. Is this a good time to buy a home in Hamilton?

Prices have been softening, and supply is relatively high, so there is a reasonable chance that buyers will continue to see gentle downward or flat price trends into 2027.

Mortgage rates are relatively low but are forecast to rise. Rising rates reduce the size of the mortgage you can qualify for, which reduces affordability. The typical annual real estate cycle usually favours buyers in late summer and autumn, when listings are plentiful, and competition is often less intense.

These factors would lead many buyers to conclude that patience can still be rewarded, and that the coming year could present as good or better buying conditions than today.

However, there is a tension. Waiting for lower prices help you a nicer home, but if morgage rates rise as expected, it reduces your home buying budget.

It is almost impossible to know which factor will be most impactful over the coming year, but if you are purchasing a forever home with a long holding period, the risk of short‑term price noise is less significant than it was a year or two ago.

If you are considering buying, be sure to drive a hard bargain and aim to pay as close to current market value as possible rather than chasing peak‑period pricing. Also, do not overextend yourself when it comes to financing; leave room in your budget for rate changes, maintenance, and life events.

Planning to Buy? Check out our Complete Home Buyer’s Guide so we can walk you through the end-to-end process and get you ready to buy your new home!

Find a local Mortgage Broker

Our FREE app matches you with local pre-screened brokers who share complementary working styles.

Here are some recent headlines you might be interested in:

Canada’s GDP growth likely turned positive in Q1 after Q4 contraction (RBC | May 22)

Spring housing market sees slow rebound as prices edge up (MSN | May 19)

Mixed start to Canada’s housing markets’ busiest season (RBC | Apr 26)

March marks four years of declining home prices in Canada (RBC | Apr 26)

Like this report? Like us on Facebook.