Five Forces Driving Quebec Home Prices

Last updated:

At the highest level, supply and demand set house prices and all other factors drive supply or demand. At Mortgage Sandbox, we have created a five-factor framework for gathering information and performing our market analysis. The five key factors are core demand, non-core demand, government policy, supply, and popular sentiment.

In the long run, the market is fundamentally driven by economic forces, but sentiment can drive prices beyond economically sustainable levels in the short run.

Summary

Core and non-core demand in Montreal and Quebec have both strengthened significantly compared to previous years, driven by rapid population growth, declining mortgage rates, and increased activity from property investors. As more people move to these cities for job opportunities and affordability relative to other major Canadian markets, competition for housing has intensified.

However, the recent migration policy pivot and the threatened imposition of tariffs by the Trump administration threaten to disrupt this momentum, introducing new economic uncertainty.

Presently, supply is balanced and could tighten as construction levels have dropped. While the market remains balanced, conditions are shifting in favour of sellers.

1. Core Demand

Core demand is a function of:

Population Growth: The pace at which people are moving to an area. An average of roughly 2.5 people live in one household.

Home Price Growth: Changes in the market value of the desired home.

Savings-Equity: How much disposable after-tax income you’ve been able to squirrel away plus any equity you have in your existing home.

Financing: Your maximum mortgage is calculated using income, monthly expenses, and interest rates.

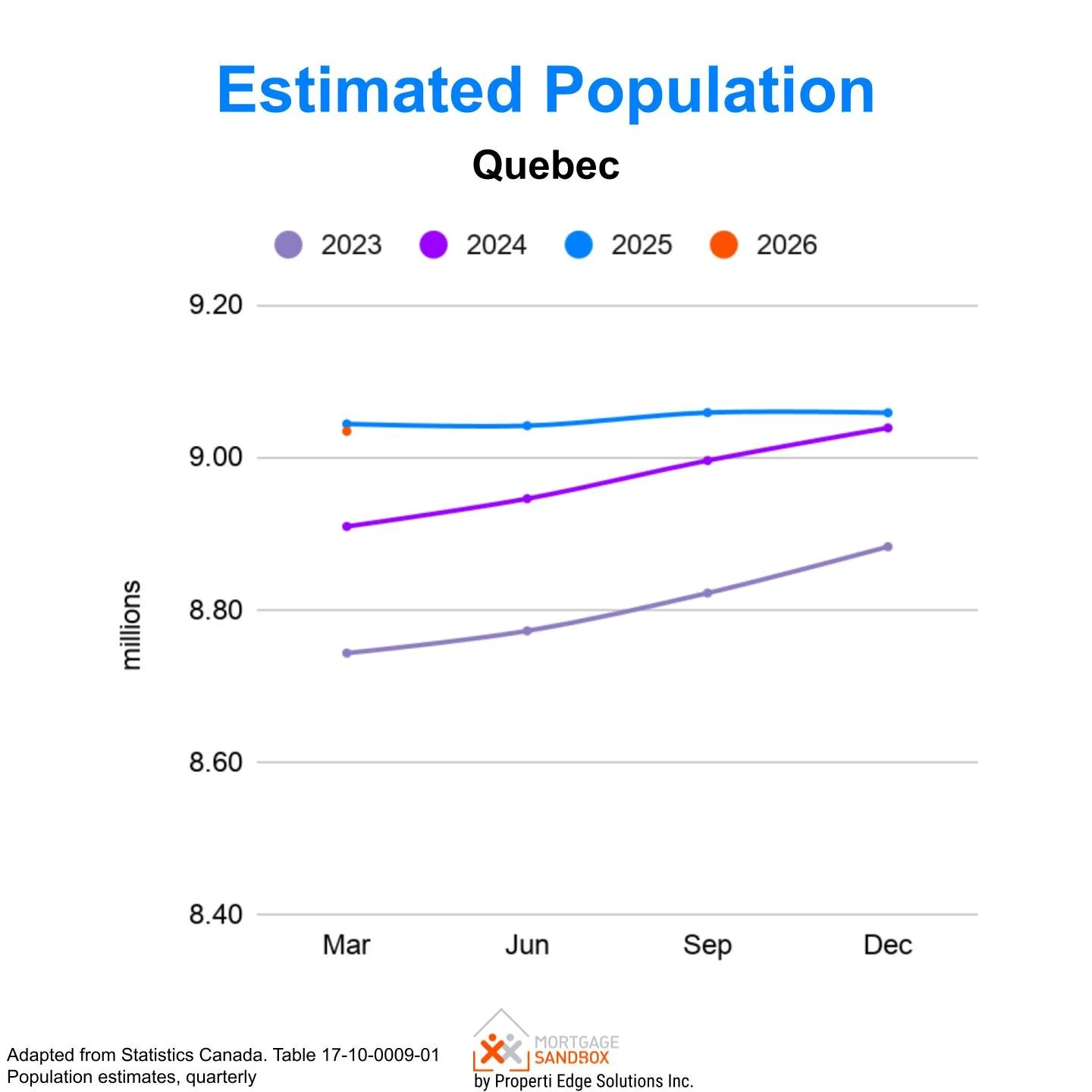

Population Growth

Quebec’s population has long been on an upward trajectory, but the rate of growth is what truly matters for housing markets. If population expansion merely keeps pace with historical trends, it exerts little additional pressure on property prices. A sharp acceleration fuels demand and drives valuations higher, while a slowdown—or outright contraction—could have the opposite effect.

After stalling in 2020, Quebec’s population growth rebounded, making up for lost ground during the pandemic but causing challenges. The federal government’s recent pivot on immigration policy, which aims to curb overall inflows, raises the prospect of a population decline in 2025. A shrinking population could weigh on economic growth and housing demand, challenging the market dynamics that have driven prices upward in recent years.

Early data suggests this has begun to affect population growth, which has already plateaued in Quebec.

Home Price Changes

Price growth reduces affordability and reduces the pool of qualified potential buyers. In an ironic twist, rising prices create downward pressure on prices. This is a factor for first-time homebuyers trying to buy an entry-level apartment.

As a rule of thumb, homeownership costs are considered unaffordable when they exceed 40% of household income.

According to RBC Royal Bank, homeownership costs in Metro Montreal were 47% of the median household income. Quebec City was 28%. In other words, Montreal home prices are above sustainable levels based on long-term economic fundamentals.

Prices peacked in Spring of 2022 and have stayed relatively flat since.

Savings-Equity

Equity

Existing homeowners benefited from price appreciation, so they have more home equity to use when buying another home.

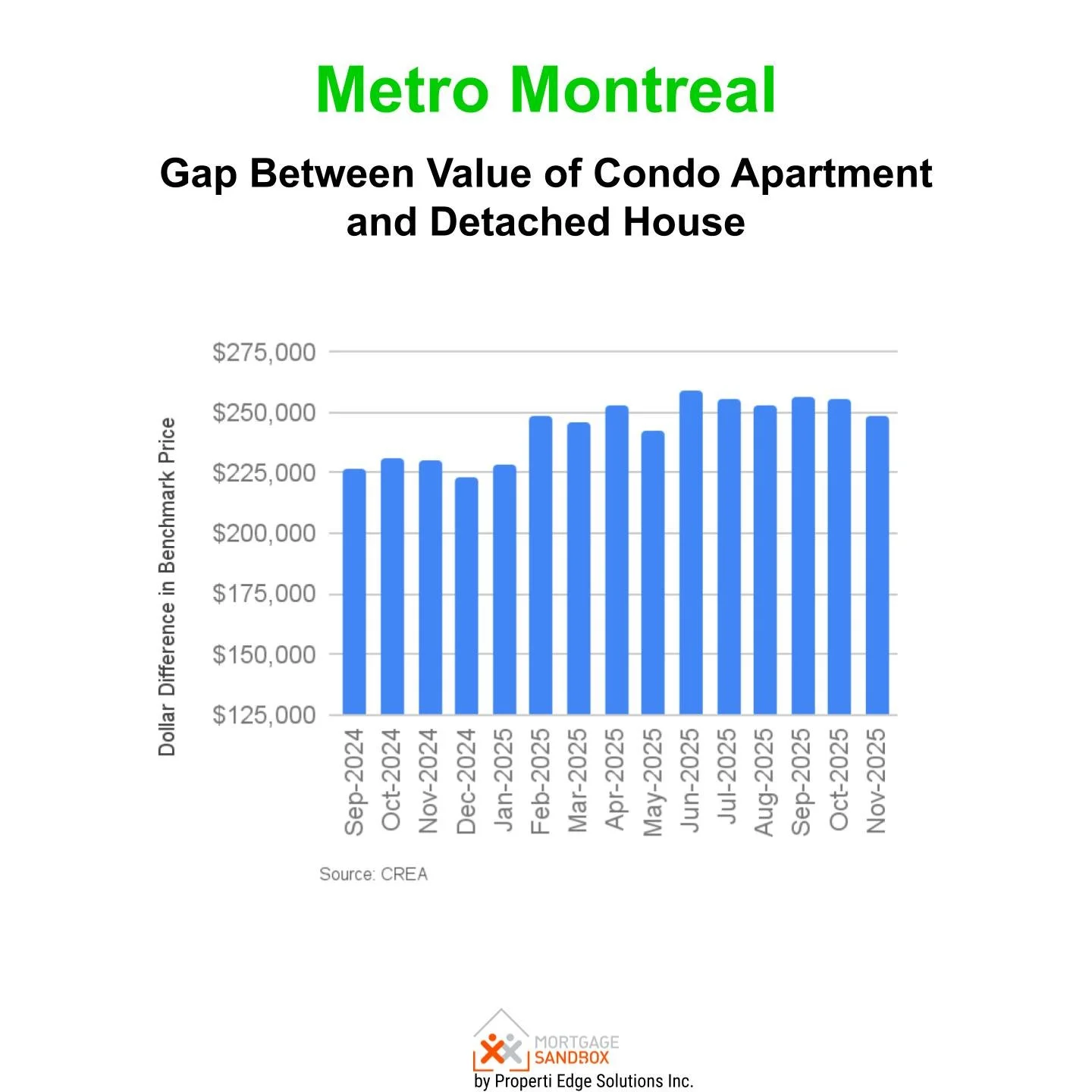

Condo-to-House Price Gap

A large gap means more savings and mortgage financing are needed for condo owners to upsize to a house.

Montreal house values have risen in parallel with condo values. The distance between the rungs on the property lader aven’t moved much farther apart.

Savings

With inflation rising faster than incomes, everyday items are becoming more expensive while paychecks are unchanged. If this trend continues, Canadians will run out of savings (including nest eggs for buying a home) and begin taking on debt to cover everyday expenses.

Financing

Mortgage Interest Rates

Since 2023, mortgage rates have been falling, however, they’ve not dropped since March. Variable mortgage rates have crept higher in the last few months. While rates are lower than the 2023 peaks, they are still nowhere near as low as they were during the pandemic. Many homeowners have mortgage renewals coming due in 2025, and they will likely face higher monthly payments going forward.

Lower rates also boost property buying budgets.

Employment and Incomes

While the employment picture has improved significantly, you must hold a job for 3 to 6 months before applying for a mortgage. Also, full-time employment in Quebec appears to have softened since the summer of 2022.

Job growth is critical because all the population growth in the world will not put upward pressure on home values if those new arrivals don't have meaningful work.

In 2024, jobes growth was not keeping pace with population gains, but 2025 has started strong. If full-time employment continues to trend upward, we can expect more demand, regardless of population growth.

Homeownership Costs

The cost of utilities (heating oil, natural gas, and power) has risen. In many cases, heating costs alone have risen $100 per month. Add the rising cost of groceries and gasoline to the equation, and it is clear that homebuyers have less disposable income to put toward mortgage payments.

Overall Core Demand

While Quebec’s population growth has slowed, its full-time employment has grown significantly.

However, a change in federal immigration policy promises significantly lower population growth, which will make demand more volatile in the future.

Overall, core demand is significantly higher than it was six months ago, but falling population growth and trade tariffs could potentially derail demand in 2025.

Find out how much you can afford to buy!

2. Non-core Demand

This represents a short-term investment, long-term investment, and recreational demand (i.e., homes not occupied full-time by the owner). Here is where foreign capital, real estate flippers, and dark money come into play. It also includes short-term rentals, long-term rentals, and recreational property purchases.

Since non-core demand is ‘optional’ (i.e., not used to shelter your family), it is more volatile than core demand.

Between 20 and 30 per cent of Canadian residential property (all types of properties) buyers are investors. In the condo apartment market, the share of investors is likely higher.

Foreign Capital

The Federal Government, using its housing agency, has announced a temporary ban on home purchases by non-Canadians from January 1, 2023, to January 1, 2027. The foreign-buyer ban won’t apply to students, foreign workers, or foreign citizens who are permanent residents of Canada; however, the additional hurdles will reduce the flow of capital to Canadian real estate compared to previous years.

Long-term Rental Investors

Rental investments are a significant driver of home prices. Demand increased in the major cities as many people began to recognize they would need to return to the office or adopt a hybrid work model.

New risks exist in the rental market due to potential planned reductions in study permits, rising mortgage costs, and rising property taxes.

1. Immigration Policy

The Minister of Immigration, Refugees and Citizenship announced that the Government of Canada will set a two-year study permit intake cap. For 2024, the cap is expected to result in approximately 360,000 approved study permits, a decrease of 35% from 2023. It is unclear what impact this will have on rent rates.

Rent rates have dropped recently in Calgary and Edmonton, and this could be enough to move many potential investors to the sidelines until rents stabilize.

2. New Mortgage Rules

The new federal rules will reduce market demand by directly increasing borrowing costs and constraining leverage for a significant segment of buyers. By prohibiting the double-counting of rental income across multiple properties and classifying loans heavily reliant on that income as higher-risk, the regulations will suppress the purchasing power of investors, who constitute over a quarter of Canadian homebuyers. This impact will be disproportionately higher for condos. A sharp reduction in investor activity, particularly within this concentrated segment, could remove a foundational source of demand, placing considerable downward pressure on a market that is already structurally dependent on investment purchases.

Short-term Rentals

Airbnbs were huge in Quebec before the pandemic, and now that international travel has recovered, short-term rentals are again influencing real estate investment.

In October 2022, according to airdna.co, short-term rentals were:

Montreal: 8,500 rentals with 74% occupancy.

An occupancy rate between 70% and 95% is typically considered a supportive investment environment.

Tourism is finally on track to match or exceed pre-pandemic levels! This bodes well for short-term rentals.

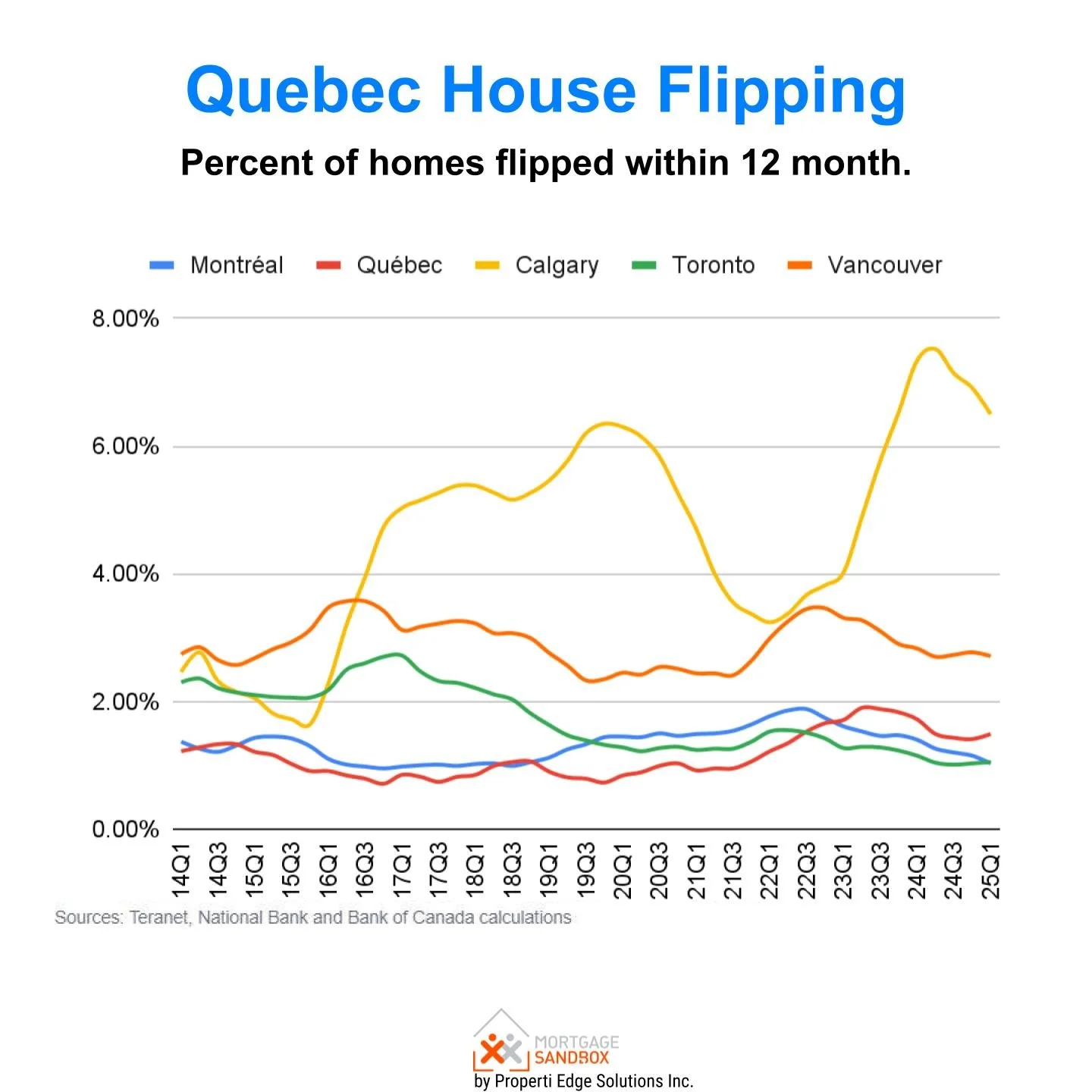

House Flippers

Nevertheless, when house prices were rising, it was an easier business for flippers.

The market has softened, and house flipping is beginning to look risky.

Note: The flaw with the chart below is that most flippers will "live in the property" for at least 1 year before selling so they can claim it as their principal residence and avoid capital gains tax on the sale. The regulators don’t count flips that occur within 18 months.

Dark Money

Dark money is the crime proceeds or money transferred to Canada illegally. This includes money earned legitimately and illegally transferred from countries with capital controls (e.g., China) and legitimate earnings moved from nations subject to international sanctions (e.g., Iran, Russia, and North Korea).

It is laundered in the real estate market to hide the illegal nature of the funds. Sometimes, the property's true owner is hidden by using a Straw Buyer, and other times a shell company owns the property.

Sometimes a real estate agent or lawyer will accept the illegal cash to help the nefarious individuals hide its true origins. In 2015, a B.C. realtor was caught with hundreds of thousands of dollars in her closet at home.

We see no evidence of a diminished role for dark money in Quebec real estate.

Overall Non-core Demand

Given the foreign buyer restrictions and volatility in the rental market, we assess that capital inflows toward residential real estate for non-core uses will soften in 2023. This adds some downward pressure on B.C. home prices.

3. Government Policy

Short-term Rental Crackdown

The provincial government implemented a short-term rental registry in 2024, to help better manage the industry.

In January 2025, the City of Montreal announced new rules on short-term rentals with an aim to keep rising rents in check. The city will only allow short-term rentals between June 10 and Sept. 10 in primary residences across the city.

The rest of the year, short-term rentals will be allowed exclusively in properly registered units within zones permitted by the city.

Beneficial Ownership Registry

Quebec rules to identify foreign resident beneficial owners were enacted in October 2020.

A foreign resident buyer tax may follow soon after. The new disclosure rules require buyers to disclose their citizenship and residency status. If a company or partnership purchases the property, the notary must determine if a foreign resident owns 50 per cent or more of the property. For trusts, the notary needs to determine if the trust's beneficiary is a resident of Canada. Experts have spotted some loopholes in this setup, but the government is trying.

Foreign Buyer Restrictions

The Federal Government, using its housing agency, has banned home purchases by non-Canadians from January 1, 2023 to 2025. There are some exceptions for those with temporary work permits, refugee claimants, and international students.

The two-year ban was implemented to allow the government to study whether it reduces the property market's levels of speculation and commoditization.

Overall Government Influence

Overall, the government unwound many programs supporting home values through the pandemic and subsequently implemented restrictions on foreign investment. Compared to a year ago, there is significantly less support from the government to maintain home values.

4. Supply

Supply comes from two sources.

Existing sales: Existing home sales are sales of ‘used homes.’ They are homes owned by individuals who sell them to upgrade, move for work, or other reasons. The Toronto Real Estate Board only reports existing home sales and listings.

Pre-Sales and Construction Completions: Most new homes are sold via pre-sales before the construction has started. These are predominantly apartments and townhomes. Data on pre-sales is private and difficult to find, but construction starts (reported by the government) are a very accurate lagging indicator of pre-sale activity.

Rising supply releases the upward pressure on prices caused by demand.

Months of Supply of Existing Homes

While the total number of homes for sale is a key supply metric, shown below, the ratio of listings to purchases expressed in months of supply is a better indicator of where prices are headed. This is because months of supply show the relationship between supply and demand. If supply and demand drop together, the market balance is maintained, and price pressures remain unchanged.

Supply has been surprisingly tight throughout the pandemic and is now trending upward.

Pre-sales and Completions

New Construction:

Housing starts and homes under construction have been weakening.

In the next 18 months, lower housing completions could lead to tightening supply conditions. However, lower construction levels also lead to lost construction jobs, which softens demand.

Pre-sales:

Pre-sales are purchases of unbuilt and completed brand-new homes from developers. Typically, a developer must sell 70% of homes in a building before starting construction, so housing starts are a good indicator of successful pre-sales.

Montreal pre-sales are much lower than in the past few years.

Popular Sentiment

Popular sentiment can be volatile and easily influenced by the latest headlines. Sentiment can shift quickly, as witnessed in the past two years.

Canadian Consumer Confidence

The Ipsos-Reid and Nanos Canadian Confidence Index shows that Canadian consumer confidence has improved significantly, and confidence in real estate values has improved. Less than 40 per cent of Canadians believe home prices in their neighbourhood will rise over the next six months.

Although consumer sentiment is a key factor contributing to real estate price trends, sentiment on its own is not an accurate predictor of future prices.

Conclusion

Here is a quick summary:

Core demand is stronger because of lower mortgage rates and exploding population growth, but Canada’s population could shrink in 2025. Trump’s tariffs could cause a recession, further dampening demand.

Non-core demand is weaker due to the weak rent rates and mounting short-term rental regulation.

The government's imposition of a foreign buyer ban removes some potential buyers, though foreign buyers were never a significant factor in Quebec.

Existing home supply (months of inventory) is rising, but there are dwindling numbers of new homes under construction. The two sources of supply might counter-balance each other.

Consumer confidence in real estate is neutral.

While it is not guaranteed, the current conditions dramatically increase the risk of a signifiacant market correction.

See our Montreal Home Price Forecast

Like this report? Like us on Facebook.