Bank of Canada More Likley to Raise Rates as Inflation Pressures Re-Emerge | June 2026

The era of rapid interest rate relief has officially run its course. Following a series of aggressive cuts throughout 2025, the Bank of Canada is poised to hold its overnight policy rate steady at 2.25 percent on June 10. A confluence of geopolitical shocks and stubbornly elevated core consumer prices has forced policymakers into a watchful posture, with the balance of risks now firmly tilted toward future rate increases rather than cuts.

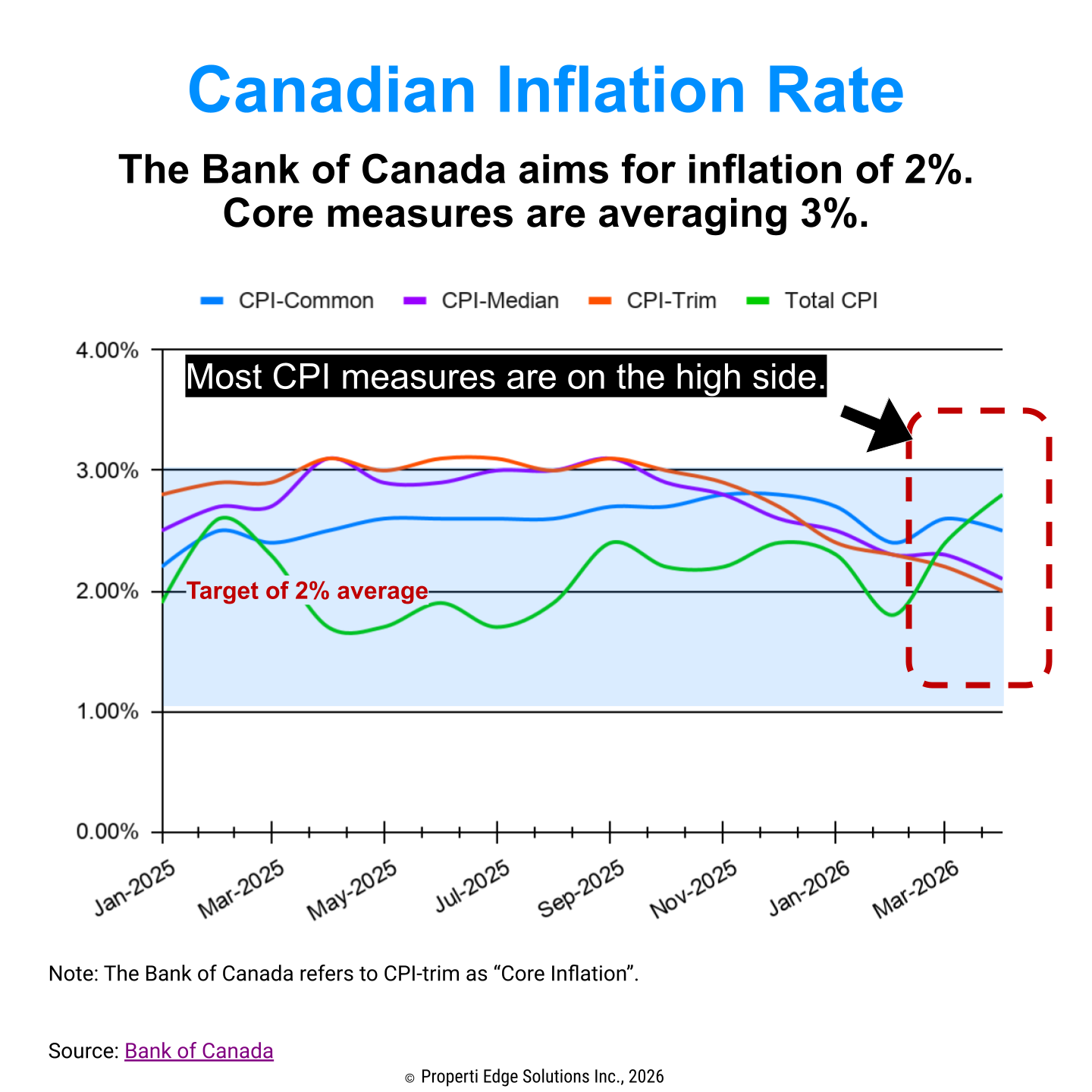

The uploaded data underlines the central bank's dilemma. While the headline inflation rate (Total CPI) has fluctuated and recently ticked upward toward 3 percent, underlying core metrics tell a more troubling story for monetary policy. Core measures have been averaging 3 percent, stuck well above the Bank of Canada’s official 2 percent target. This persistent underlying heat, combined with a volatile global economic landscape, heavily restricts the central bank's ability to offer further monetary easing.

Key Drivers: Geopolitics, Energy Shocks, and Evolving Trade

The Energy Supply Shock: The primary catalyst disrupting the rate-cut cycle is the war in Iran, which has severely restricted shipping through the Strait of Hormuz. This geopolitical crisis has pulled roughly 10 percent of global oil supply off the market, sending West Texas Intermediate surging from US$75 to nearly US$100 a barrel. This supply shock injects stagflationary pressure into the Canadian economy, driving headline inflation up while simultaneously acting as a drag on broader economic growth.

A Cooling Domestic Backdrop: The domestic economy is showing distinct signs of fatigue, creating a complex policy environment. Gross Domestic Product contracted in the final quarter of 2025 and dipped 0.1 percent annualized in the first quarter of 2026. Furthermore, the labour market shed roughly 100,000 jobs early this year, pushing the unemployment rate to 6.6 percent in May. While these cracks in growth reflect genuine economic slack, the Bank of Canada’s primary mandate remains inflation control, forcing it to prioritize price stability over economic cooling.

Strategic Trade Diversification: On the macroeconomic front, Canada is actively attempting to insulate itself from U.S. trade volatility ahead of upcoming USMCA renegotiations. Following Prime Minister Mark Carney's recent bilateral visit to Beijing, Ottawa established a new strategic partnership with China. A preliminary agreement lowered Canadian tariffs on a quota of Chinese electric vehicles in exchange for reduced Chinese tariffs on key agricultural exports, including canola, lobster, and peas. While intended to establish long-term economic alternatives, these shifting alliances introduce short-term trade uncertainties that could influence domestic corporate investment.

The Mortgage Landscape: Fixed vs. Variable

The sudden shift in monetary expectations has altered the outlook for Canadian borrowers, effectively eliminating the prospect of cheaper financing over the medium term.

Fixed-Rate Mortgages

Fixed borrowing costs are closely tethered to the five-year Government of Canada bond yield, which reflects market expectations for inflation and monetary policy. Since the outbreak of the Middle East conflict, five-year yields have climbed by 35 to 40 basis points, holding steady between 3.0 and 3.5 percent with a distinct upward bias.

Consequently, five-year fixed mortgage rates have lifted off their 2025 lows, currently averaging between 4.0 and 4.6 percent depending on insured status. Major institutional forecasters expect these rates to drift higher, potentially landing between 4.5 and 4.9 percent by the end of 2026, and pushing toward 5.1 percent by 2028 if core inflation proves structural.

Variable-Rate Mortgages

Variable rate pricing moves in lockstep with the central bank's overnight policy rate. With the benchmark currently sitting at 2.25 percent, standard variable products are priced at prime minus a discount, yielding effective rates between 4.00 and 4.50 percent.

This environment represents the absolute floor of the current interest rate cycle. Variable policy rates are projected to hold flat through the summer before beginning an upward trajectory late in 2026. Led by Scotiabank, which forecasts three rate hikes in the latter half of this year, and supported by TD and RBC models, expectations are mounting for policy tightening. By the conclusion of 2027, variable-rate holders could face borrowing costs that are 1.00 to 1.50 percent higher than today's levels.

Real Estate Implications: Buyers and Sellers Face a New Reality

The transition from monetary easing to projected tightening is fundamentally reshaping transactional dynamics across Canadian housing markets.

| Homebuyer Impact | Seller Impact |

|---|---|

| 10% purchasing power reduction per 1.00 percent rate increase. | Properties will sit on the market longer. |

| Higher qualification stress test, and lower resulting purchase budgets. | Disconnect between legacy price expectations and buyer capacity. |

| High incentive to secure rate hold before rates rise. | Success requires data-driven pricing strategy. With ample supply, you are competing against other sellers. The opposite of a bidding war. |

The Homebuyer Budget Squeeze

Purchasing power is being systematically eroded by the shift in the interest rate outlook. Mechanically, every single percentage point increase in a mortgage interest rate reduces a buyer's maximum purchasing power by approximately 10 percent for an identical monthly capital outlay.

Furthermore, because buyers must qualify under the stringent mortgage stress test, a substantial segment of active demand is being actively priced out of the market. Buyers looking to transubstantiate transactions are highly incentivized to secure formal pre-approvals immediately to lock in current rates before the projected late-2026 upward adjustments take effect.

The Seller Real Estate Reality

The structural shift in buyer affordability has completely altered the selling environment, effectively ending the uninhibited bidding wars that characterized the earlier part of the decade. As capital costs rise, listings are lingering on the market significantly longer.

Sellers can no longer rely on aspirational pricing strategies; success in the current market requires pricing properties accurately from day one based on localized comparable data and local financing constraints. While well-presented and fairly valued homes continue to transact due to underlying housing demand and stable household net worth, overpriced listings are experiencing prolonged market stagnation as the pool of qualified buyers shrinks.