The Great Canadian Chill | The Bank of Canada Leave Rates Unchanged | April 29 2026

For years, the Canadian economy was less a G7 powerhouse and more a collection of over-leveraged condos held together by a central bank’s largesse. That era ended definitively on April 29th.

While the Bank of Canada (BoC) opted to keep its overnight rate at 2.25%, the accompanying Monetary Policy Report was a sombre admission: the engine of Canadian growth, residential real estate, has finally stalled.

From Engine to Anchor

For a decade, housing was the primary driver of domestic demand; today, it is its heaviest drag. The Bank’s latest projections revised housing’s contribution to 2026 GDP growth downward by 0.3 points, the sharpest decline among all domestic components.

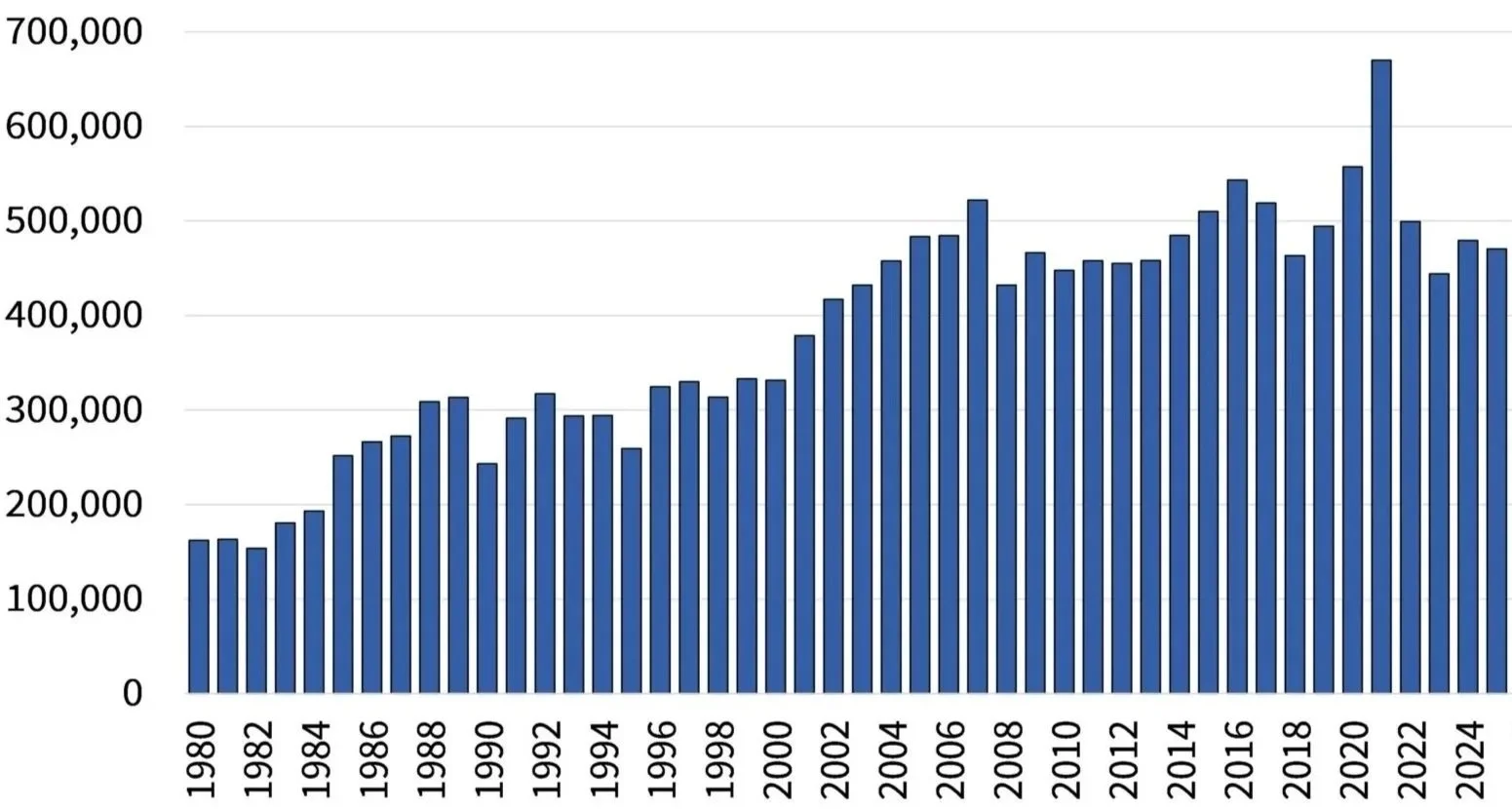

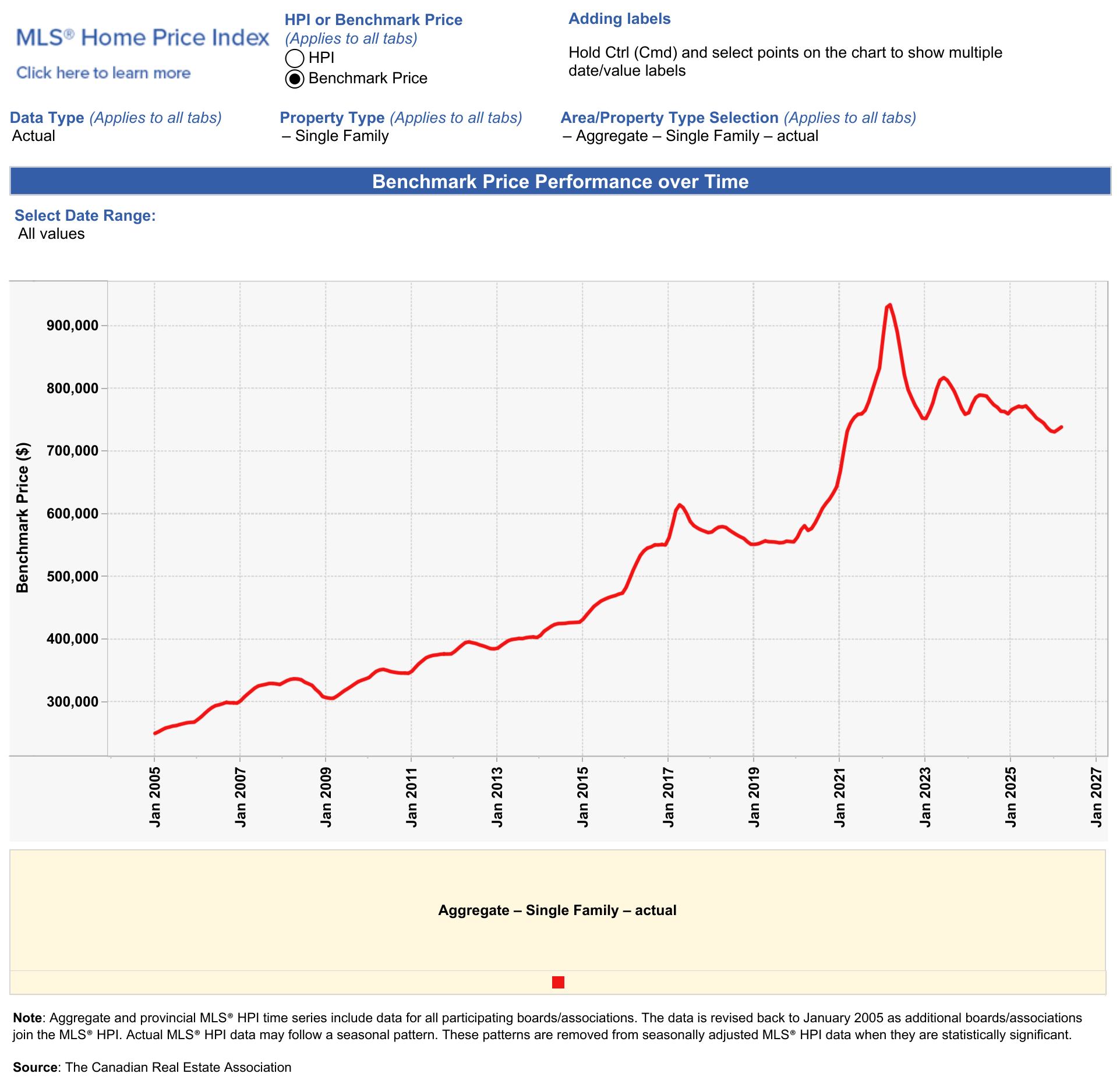

Canadian Residential Real Estate Sales

The cause is a "stagflationary" cocktail. While the central bank maintains a "patient" hold, the war in Iran has sent global oil prices soaring toward US$100 a barrel.

For a commodity-producing nation like Canada, this provides a deceptive boost to national income while simultaneously gutting the consumer through gasoline-led inflation. Governor Tiff Macklem now finds himself in a "risk management" trap: raise rates to combat oil-fueled inflation and risk a total collapse of the housing market, or hold steady and watch the "hawkish" tail risks of the Middle East unanchor inflation expectations.

The Condo Apartment Conundrum

Nowhere is this tension more palpable than in the glass-and-steel high-rise powerhouses of Toronto and Vancouver. The BoC’s report highlighted an "epic glut" of small investment condos. In particular, micro-units that were built to appeal to investors and speculative buyers rather than to buyers intending to live in the unit. With record population growth and near-zero rental vacancies, Canadians were desperate to find a place to live, so lower-quality, low-livability units still commanded top rents.

These properties, once the darlings of the "infinite growth" narrative, are now flooding a market where investor interest has evaporated, and the structural floor has been pulled out from under them.

After years of record-breaking population growth, Canada is facing a sharp slowdown in new arrivals. Without the constant pressure of new demand, the "stretched affordability" in Ontario and British Columbia is no longer a temporary hurdle but a permanent barrier.

A Divided Street

The nation’s chartered banks are split on what comes next. RBC Economics favors the "patient" path, betting that excess supply in the economy will eventually cool the fires of inflation. Scotiabank, however, delivered a blistering "hawkish" critique, accusing the BoC of ignoring a "fire" in non-energy commodities and failing to account for C$38bn in new federal spending. To Scotiabank, the BoC is "buying time" with stale data while the real economy prepares for a summer of interest rate shocks.

The Briefing: Mortgages, Markets, and the War

How will 5-year fixed and variable mortgage rates diverge?

The 5-year fixed rate is currently "sticky" and under upward pressure, as it tracks bond yields that are sensitive to the "war premium" in the Middle East. Conversely, variable rates remain anchored to the BoC’s policy rate. However, with the Bank warning of "consecutive rate increases" if oil prices remain elevated, the historical "discount" on variable rates now carries a significant risk of a payment shock by autumn.

Why are Ontario and British Columbia specifically at risk?

These provinces are the most rate-sensitive due to their historically poor affordability. While affordability is better than it was in 2021, it is still worse than in the 1980s, when a typical mortgage rate was 15 percent. In a market where a "starter" home requires a two six-figure incomes, even a 0.25% move is the difference between a sale and a listing that languishes for months. The "condo glut" is a uniquely Ontarian and British Columbian phenomenon that threatens to turn the "housing drag" into a full-scale regional recession.

What is the "Iran Factor" for Canadian inflation?

Ordinarily, higher oil prices are a net positive for Canada’s terms of trade. However, the current spike is "cost-push" inflation. It raises the price of everything from groceries to transit without a corresponding increase in domestic productivity. This forces the BoC to maintain higher rates even as the domestic economy softens, a classic stagflationary bind.

What happens to property markets if population growth hits zero?

The Canadian "bull case" for real estate has long been a demographic one. Zero-to-negative population growth removes the "guaranteed" demand for rentals and entry-level homes. While this is disinflationary (assisting the BoC in the long run), it destroys the speculative premium that has historically propped up valuations in the GTA and Metro Vancouver.

How does rising unemployment (6.5%–7%) alter the BoC’s math?

Rising unemployment typically prompts rate cuts. However, the BoC noted that current job losses are concentrated in sectors targeted by US tariffs. If the Bank cuts rates to save jobs while oil prices are still fueling inflation, it risks a currency collapse. Consequently, the "soft" labour market is more likely to result in a prolonged "hold" rather than the relief of a rate cut.

The upshot is a period of painful adjustment. Canada’s housing-dependent economy is being forced into a cold shower of geopolitical reality and demographic correction. For the residents of Ontario and BC, the question is no longer when rates will fall, but how much equity will survive the wait.