Canada’s central bank holds fire, but mortgage costs are already climbing

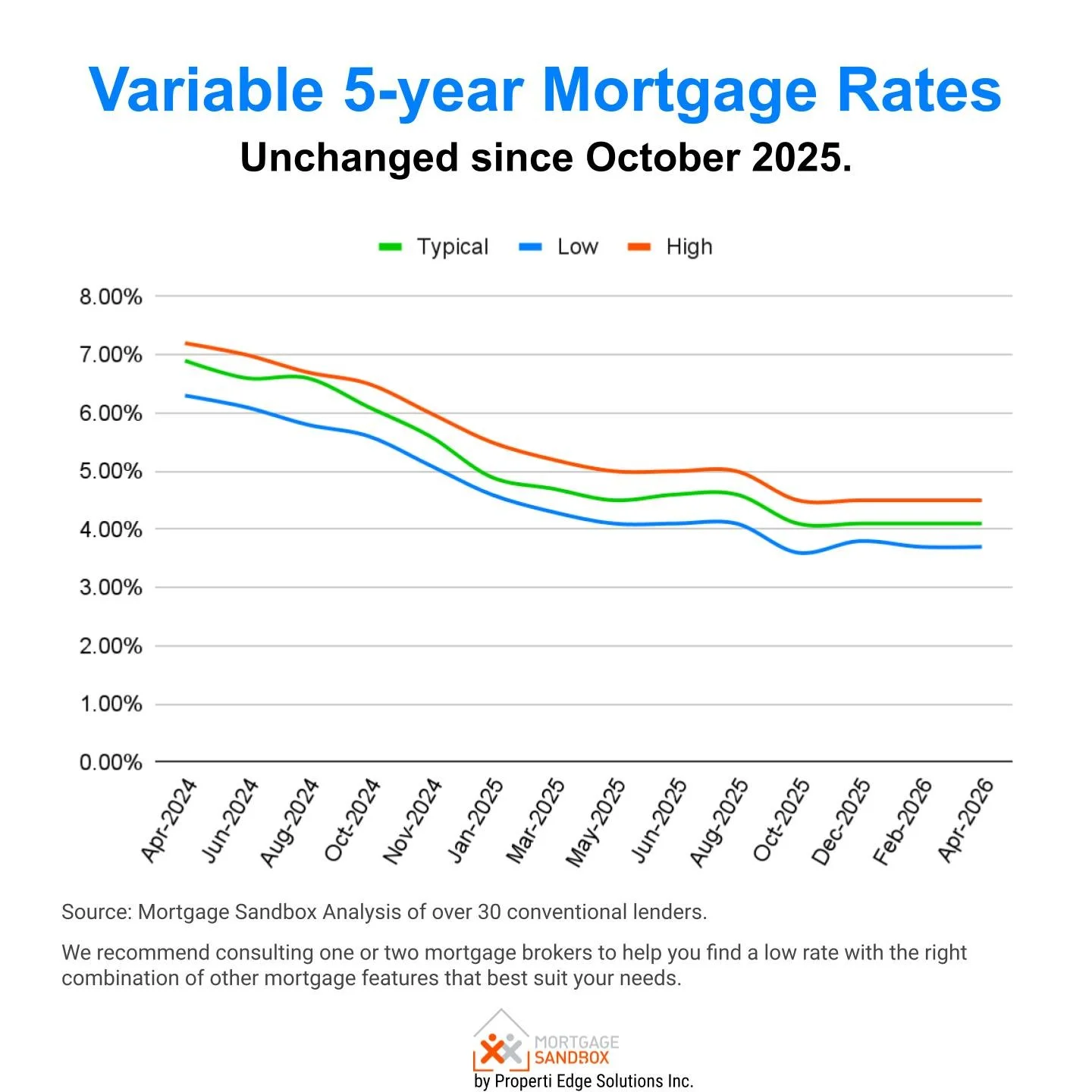

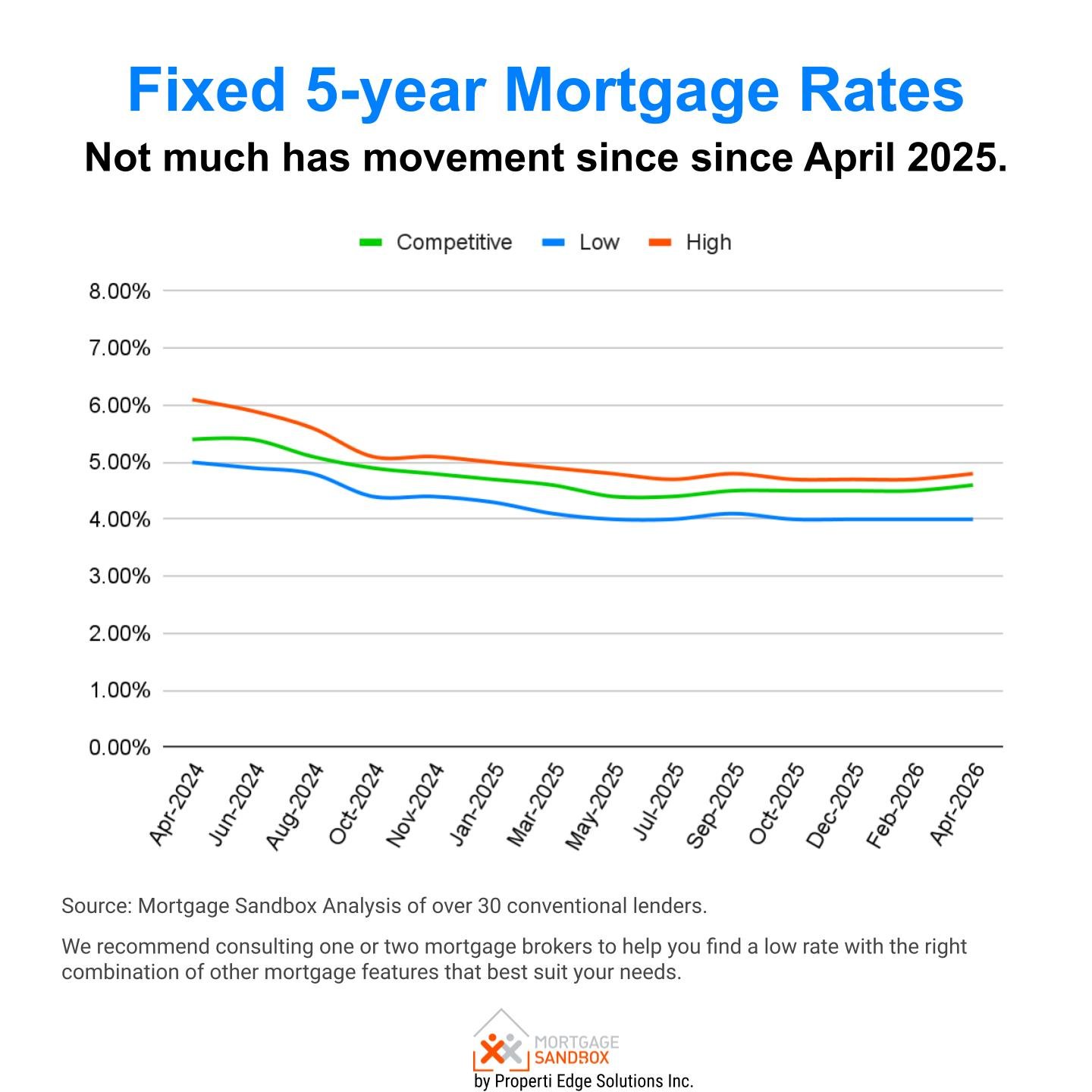

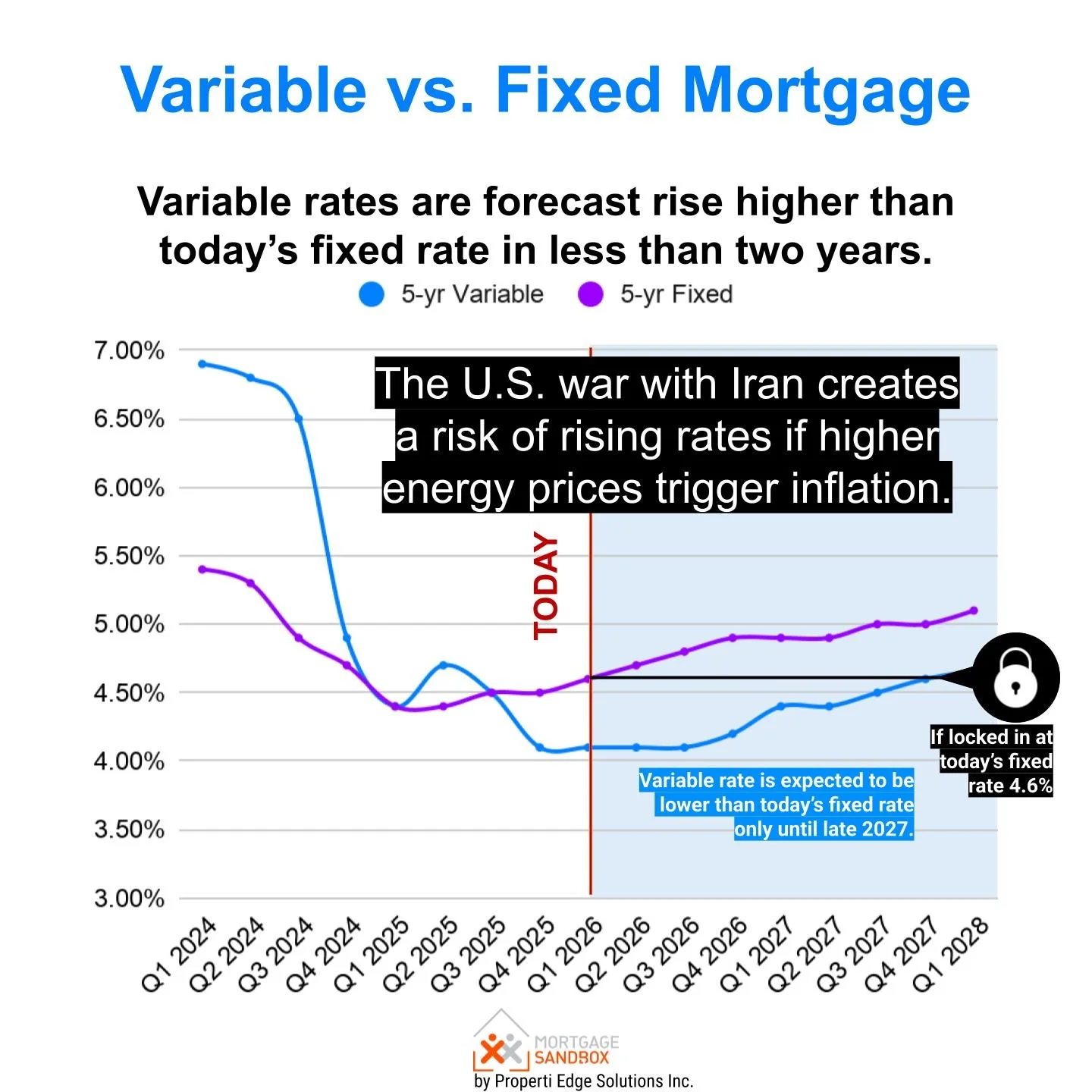

The Bank of Canada is all but certain to leave its benchmark interest rate unchanged at 2.25% when it meets on April 29. Yet for anyone borrowing to buy a home, the respite will prove fleeting. Variable rates may stay flat for a few more months, but fixed rates have already jumped. Both were poised to rise further over the next 18 months, and an outcome that has become more likely as a result of the War in Iran.

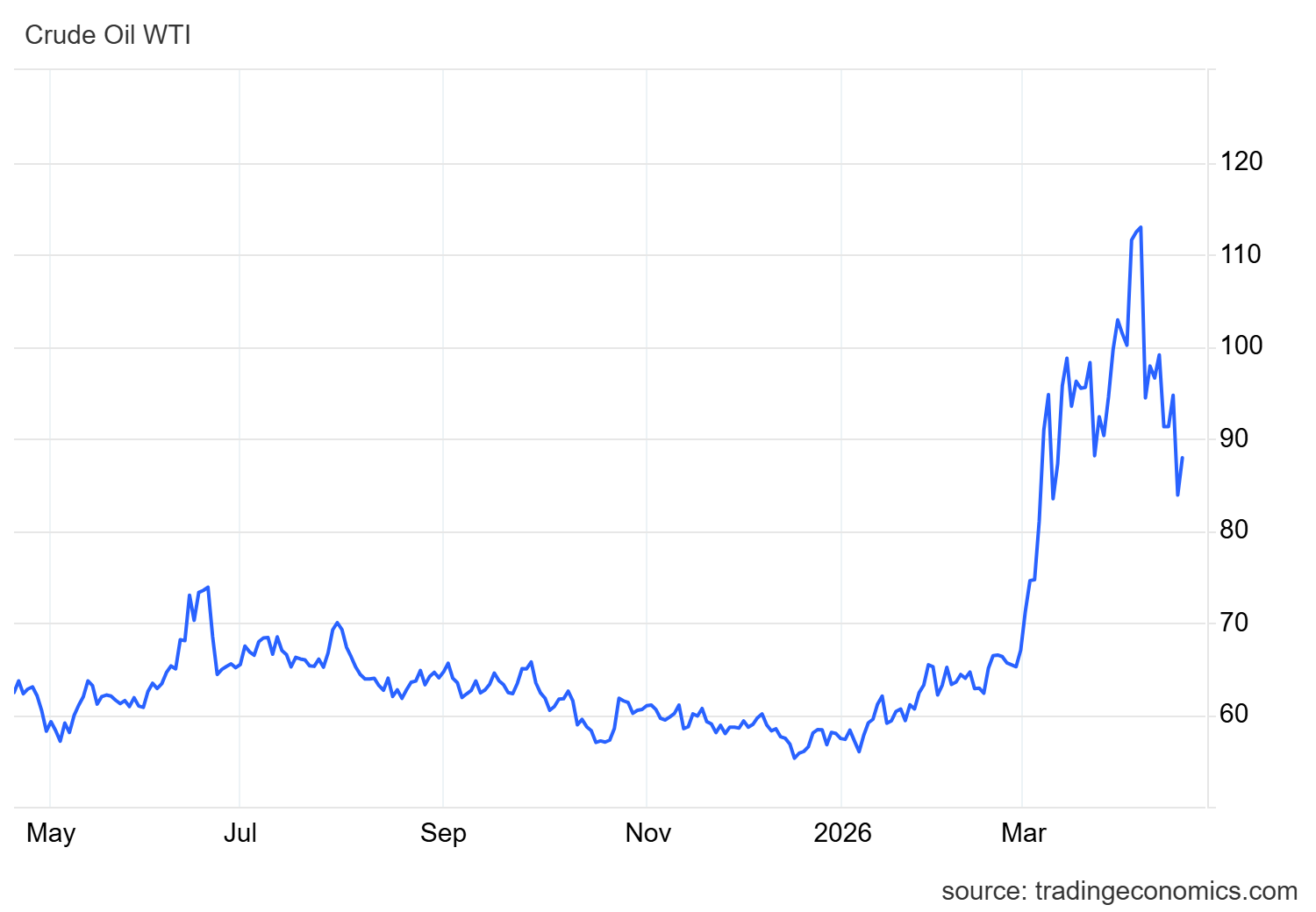

Why the oil shock is different this time

The reason lies not in Ottawa but in the Persian Gulf. Military conflict involving Iran has shut most of the Strait of Hormuz, knocking roughly 20% off global oil supplies. West Texas Intermediate crude, which traded near US$70 a barrel in early 2026, briefly touched US$110 before settling around US$90. For a net oil exporter such as Canada, this brings a temporary windfall to Alberta oil producers. But for other industries in Alberta and the rest of Canada, and for Canadian households, it means dearer petrol and heating fuel, and a fresh jolt to inflation.

Unlike the oil shock that followed Russia’s invasion of Ukraine in 2022, today’s economy lacks the surplus demand that turned higher energy prices into a wage-price spiral. Canadian employment has fallen by about 100,000 jobs this year. Growth in the final quarter of 2025 was weaker than expected. And the labour force is shrinking as the federal government reins in temporary immigration. With slack accumulating, the Bank of Canada can afford to “look through” a temporary rise in headline inflation, which is expected to touch 3% in the spring.

A reprieve that will not last

That is the short term. Over the next 12 to 18 months, the outlook turns decidedly less comfortable for borrowers. Scotiabank expects the Bank of Canada to raise rates three times in the second half of 2026. TD Bank notes that markets have already priced in at least one hike. Even National Bank, which foresees no move this year, concedes that “inflation-related anxiety” could force a tightening in early 2027.

Fixed mortgage rates, which move with Government of Canada bond yields, have already risen by 0.35 to 0.40 percent since the fighting began. And they are unlikely to fall back. Longer-term bond yields are being pushed higher by stubborn US inflation, heavy government borrowing and the risk that the Middle East conflict will drag on.

A two-week ceasefire reached in early April has calmed markets, but oil flows through the Strait of Hormuz will take months to normalize even if a permanent peace is signed tomorrow.

What should homebuyers do now?

For prospective buyers, the smartest move is to secure a 120-day pre-approval on a fixed rate. That locks in today’s rate while you shop for a property. If rates go higher, you win. If rates fall (unlikely), you can walk away. With fixed rates already elevated and bond markets pricing in further increases, a pre-approval is cheap insurance.

What current mortgage holders need to know

For existing mortgage holders not yet up for renewal, a “blend and extend” – mixing your current rate with today’s five-year fixed rate for a new, longer term – can provide insurance against further increases. A blend-and-extend allows you to renegotiate your rate early without paying a penalty fee to break the current contract.

For those facing renewal in the next six months, your existing lender will not lock in a rate early. But a mortgage broker can find a new lender willing to offer a 90- to 120-day rate hold on a transferred mortgage. Given where rates are headed, that early rate-lock is worth the paperwork.

Boxed in, but not yet ready to move

None of this guarantees a soft landing. The Bank of Canada remains boxed in. Tighten too soon, and you crush a fragile recovery. Wait too long, and inflation expectations could break loose.

For now, patience is the right call. But for anyone carrying a mortgage – or dreaming of one – patience is a luxury you no longer have.