Housing Market Alert: The 2026 Mortgage Renewal Wave Could Flood the Market with Listings

A major surge of Canadian mortgages is set to renew in the first half of 2026, which will force many homeowners who secured ultra-low rates during the pandemic to face significantly higher monthly payments. While experts believe that the banking system is prepared for this challenge, it is likely that many homeowners will encounter financial difficulties and may choose to sell their properties. This increase in active listings could shift the market further toward a buyers’ market, giving homebuyers greater leverage to negotiate lower prices. Additionally, some sellers who purchased homes at the market peak may find their equity is considerably at risk.

The Renewal Peak: A Million Loans and Counting

Canada is entering an unprecedented period of mortgage renewals, with the peak expected in mid-2026.

The Scale:

Following 750,000 renewals in the latter half of 2025, over one million more mortgages are set to renew in 2026, according to the Canada Mortgage and Housing Corporation (CMHC). A large segment of these loans, particularly those on 5-year fixed terms, were originated in the first half of 2021 when rates were at historic lows, often sitting below 2%.

The Payment Shock:

For many holders of 5-year fixed-rate mortgages renewing in 2026, the increase in payment will be particularly steep. Analysis from the Bank of Canada indicates that this group could experience an average monthly payment increase of 15% to 20% compared to levels seen in late 2024.

The Highest Risk:

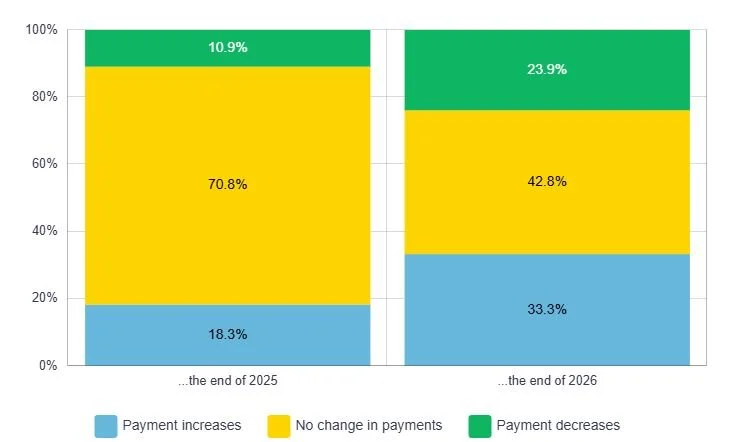

Examining the chart above, you'll notice that while the average monthly payment is expected to rise by 15% to 20%, a significant number of mortgage holders may face increases of 25% to 40%. These individuals might consider selling their homes as a result.

Around 10% of those renewing in 2026 could see their payments increase by over 40%.

The Looming Spike in Supply

While the majority of homeowners are expected to manage the transition due to the original stress test requirements and income growth since 2021, a sizable minority may find the new payments untenable, especially those who "stretched" to afford their homes at peak valuations.

The crucial question for the real estate market is:

How many homeowners will be forced to sell?

"Many who foresee financial hardship at renewal will choose to sell in the Spring of 2026," according to market analysts. This proactive selling, aimed at avoiding eventual default or simply unmanageable budget stress, could lead to a spike in active listings, boosting housing supply for buyers.

Actionable Advice for Buyers and Sellers

For those navigating the 2026 housing market, the coming renewal peak presents distinct challenges and opportunities:

For Sellers: If you anticipate financial stress from a 2026 renewal, selling today or in early spring, before a potential wave of competing listings hits, may be the wisest financial move.

For Buyers: The prospect of increased supply from forced or pre-emptive sales could lead to greater choice and potentially more balanced pricing, particularly in the first half of 2026. Be ready to act quickly if favourable inventory appears.

Actionable Advice for Mortgage Holders

Are you facing a renewal in the next 12-18 months? Check out our mortgage rate forecast. You should always begin shopping for a new mortgage 5 months before renewal. Mortgage Brokers and Lenders can lock in a favourable rate 4 months before the renewal date, giving you plenty of room to breathe.