Metro London ON Home Price Forecast - Jan 2021

HIGHLIGHTS

Other Canadian cities have experienced a decline in condo prices while house prices accelerated, but London and surrounding areas home values are rising in all categories.

Mortgage rates are at historic lows. However, higher unemployment largely offsets the benefits of low rates.

The second wave of COVID-19 is not yet under control. Continued high levels of infection will lead to restrictions and economic fallout.

Several vaccines show promising results, but they are unlikely to be widely available until mid-2021. A third wave of infection this Spring is possible.

This article covers:

Where are Metro London prices headed?

What factors drive the price forecast?

Should investors sell?

Is this a good time to buy?

1. Where are Metro London home prices headed?

Home Price Overview

Metro London prices have accelerated significantly in the past few months, which has pushed more potential home buyers out of the market.

People planning to sell their home will take heart because home values are at all-time highs.

Given the current recession and a Wave 2 of infections, sellers may want to push ahead and sell during the pandemic because there is no guarantee that home prices will maintain current values over the next two years.

The Coronavirus Pandemic, the resulting recession, and the potential for a second or third wave of infection are now the primary source of uncertainty for home values.

The real estate statistics for Metro London include St. Thomas, Middlesex, and Elgin Counties.

Metro London Detached House Prices

It seems unlikely that record house prices will be sustained through the next 12 months based on economic fundamentals. So far, buyer sentiment has overwhelmed the core fundamentals.

Market Risk

House price growth in London has been very high. CMHC performs a quarterly risk assessment of various Canadian markets. They don’t cover London, but they do report on Toronto and Hamilton. Hamilton is the market most similar to London, and CMHC has assessed Hamilton to be at high risk of a price correction.

The “soft landing” that government policymakers were targeting has become more elusive. We believe politicians were hoping to guide the market toward a typical annual real estate cycle with price growth in the range of 1 to 3% annually – in line with income growth.

Metro London Condo Apartment Prices

Metro London condo apartment prices are also rising, though the Benchmark price has levelled off over the summer. Today, a benchmark London condo is still affordable without help from family.

With more people working-from-home, we expect developers will begin marketing larger (i.e., 2 and 3 bedrooms) apartments to meet buyer preferences. As the supply of more generous floor plans comes to the market, it may depress the values for small floor plan condos.

At Mortgage Sandbox, we would like developers to build 4 and 5 bedroom condos because:

Not everyone can afford to buy a house for their family.

Canadians who now work from home need more room to segregate workspace from living space within their homes.

Many Canadians with longer working hours find it challenging to stay on top of necessary house upkeep (i.e., mowing lawns, clearing eaves, shovelling sidewalks).

Many people prefer to live in higher-density neighbourhoods with all the essential amenities within walking distance.

Still a challenge for first-time homebuyers

London’s house prices have become much less affordable. A homebuyer household earning $75,500 (the median Metro London household before-tax income) can get a $310,000 mortgage. That’s enough to buy a benchmark priced condo, but buying a house is out of reach for most locals.

2021 Metro London House Price Forecast

There is a lot of uncertainty in the forecasts for 2021 and 2022. Many of the forecasters we've surveyed have different expectations for:

How likely is the third wave of COVID-19 infections and associated restrictions?

Will the economy will re-open in the 'new normal' in June or December 2021?

Will the federal government succeed in achieving its aggressive immigration targets during a pandemic and with high unemployment?

Since the mortgage payment deferrals expired in October, will the anticipated distressed home sellers appear in the housing market?

As a result of their varying assumptions, some forecasters expect prices to continue rising, while others expect are more likely prices to drop.

For example:

For example, Re/MAX predicts London prices will rise 2% in 2021.

The Canadian Real Estate Association anticipates prices across Ontario will rise 16%!

Moody’s Analytics, which develops mortgage risk software for Canadian banks, predicts a modest 6.5% drop in Hamilton and a 3% drop in Ottawa. London may fall somewhere between the two.

Moody’s hasn’t attempted to pinpoint the timing of the decline in values. However, our research shows that most past declines in Canadian home values have begun between May and July. Traditionally, there is less supply (fewer listings) between February and May, which puts upward pressure on prices.

CMHC, the government housing agency, predicts a ‘peak-to-trough’ drop of between 9% and 18%. They expected government aid and mortgage deferrals would cushion the blow in 2020 and that the market would be impacted in 2021 with a 2022 recovery.

There is no consensus among economists. Market sentiment and government stimulus have led to price acceleration and record home purchases even though most economic fundamentals have faltered.

We tend to place a little more weight on CMHC and Moody's Analytics. They may be projecting lower values in the future, but:

CMHC sells insurance to banks to help limit their losses if a mortgage goes bad.

Moody’s Analytics sells software to banks to help them assess the risk of their mortgage portfolios.

Both organizations are unique in their ability to see market conditions across the regions and all the banks.

In the next section, we examine the five factors that drive these forecasts. They will help explain why several forecasters are anticipating price drops.

For a more thorough comparison of the Coronavirus Recession to the Great Recession and the Great Depression and their impacts on property prices, check out our recent article: “Should I sell my home today?”

At Mortgage Sandbox, we provide a price range rather than attempting a single prediction because many real estate risks can impact prices. Risks are events that may or may not happen. As a result, we review various forecasts from leading lenders and real estate firms, and we then present the most optimistic estimates, the most pessimistic prediction, and the average forecast. Do you want to learn more about real estate risk? We've written a comprehensive report that explains the level of uncertainty in the Canadian real estate market.

Our forecast inputs:

2. What factors drive the price forecast?

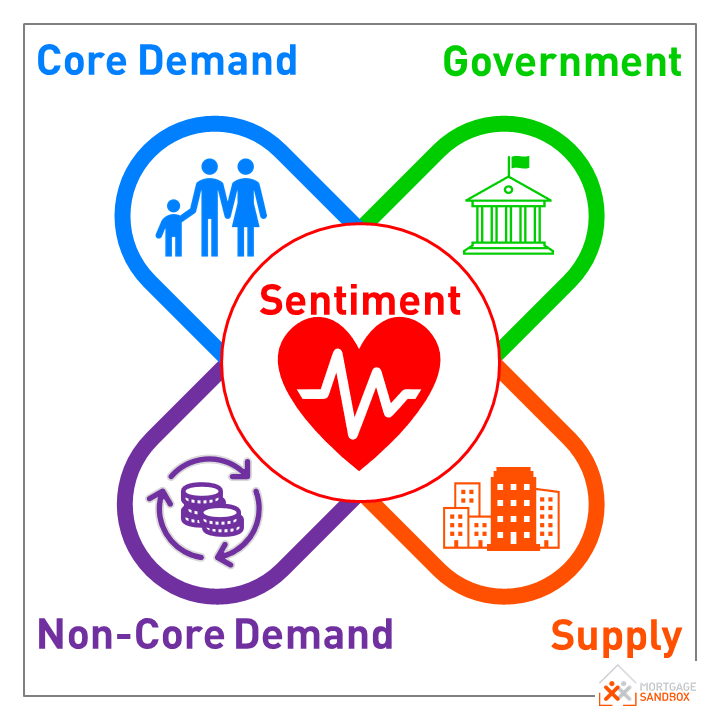

Mortgage Sandbox 5 Forces Framework

At the highest level, supply and demand set house prices and all other factors drive supply or demand. At Mortgage Sandbox, we have created a five-factor framework for gathering information and performing our market analysis. The five key factors are core demand, non-core demand, government policy, supply, and popular sentiment.

In the long-run, the market is fundamentally driven by economic forces. Still, sentiment can propel prices beyond economically sustainable levels in the short-run.

Overall, the factors leading to price gains are weakening.

Core demand: Weaker.

Non-core demand: Weaker.

Government Intervention: Weaker.

Supply: Unchanged.

Popular sentiment: Weaker but Improving.

3. Should Investors Sell?

From a seller’s perspective, more changes in the market that influence prices downward, so now may be a better time to sell than in two years, and the annual real estate cycle usually favours sellers in the first half of the year.

Sellers should always consult a mortgage broker early to prioritize flexible loan conditions and reduce the risk of mortgage cancellation penalties. Find out more about the benefits of a mortgage broker.

Planning to Sell? Check out our Complete Home Seller’s Guide.

4. Is this a good time to buy?

With accelerating prices, some homebuyers who took a cautious wait-and-see approach in 2019 may have been priced out of the market.

Prices are still trending upward, but Coronavirus containment efforts pull prices down. Prices will likely be lower in 2021. Keep in mind that the annual real estate cycle usually favours buyers in late summer.

The wild card is the Coronavirus. At this stage, it's difficult to determine how much it will impact the market.

If you are thinking of buying, be sure to drive a hard bargain and pay as close to market value as you can. As well, when it comes to financing, don't bite off more than you can chew.

Planning to Buy? Check out our Complete Home Buyer’s Guide so we can walk you through the end-to-end process and get you ready to buy your new home!

Here are some recent headlines you might be interested in:

New CMHC report says Canadian housing market could see a 14% plunge (The Star, Jan 21)

These are Canada's fastest growing communities as cities see record exodus (CTV, Jan 19)

Toronto rent was down 20.4 percent in December while real estate sales were way up (NOW, Jan 19)

Pandemic housing boom means affordability is no longer just a big-city problem (Global News, Jan 16)

Toronto, Montreal see exodus pick up pace, aggravated by COVID-19 pandemic (Globe and Mail, Jan 22)

The stresses that changed Canadian and Ottawa real estate in 2020 (Ottawa Citizen, Jan 2)

COVID-19 has made reading next year's real estate market harder than ever (CBC. Dec 14)

Interim B.C. money laundering report out, but final inquiry results will be delayed (CTV, Dec 10)

Like this report? Like us on Facebook.