The March 2026 Bank of Canada Rate Decision & What It Means for Your Mortgage

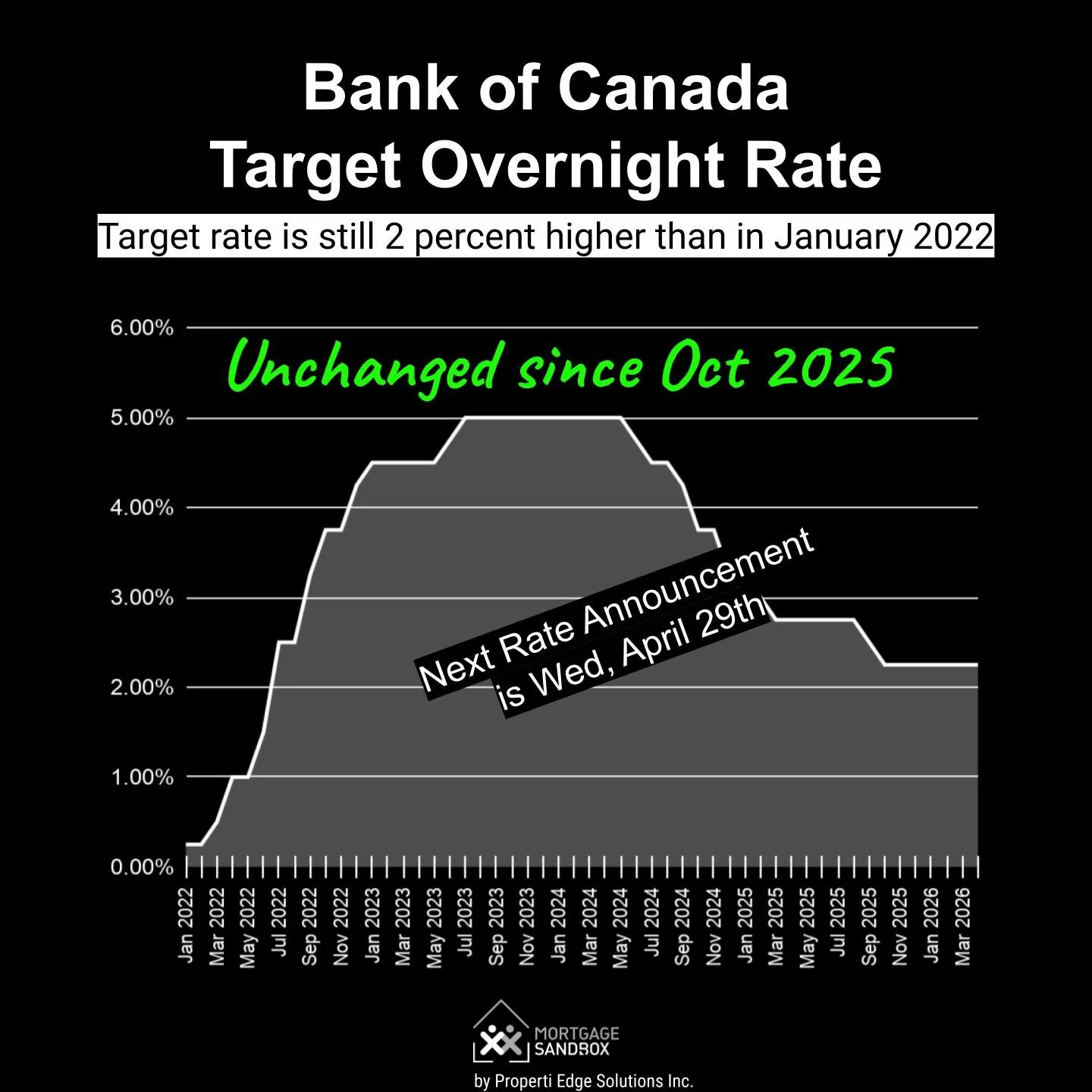

Today, the Bank of Canada announced that it is holding its key interest rate steady at 2.25%, meaning Prime rates will not change for now. Link to full announcement.

While this hold provides a moment of stability, it’s important to look ahead. The Bank’s announcement highlights two significant forces at play:

a softer Canadian economy resulting from trade disputes with the United States, and also

Inflation risks stemming from trade tariffs and the conflict in the Middle East have driven up global energy and consumer goods prices.

The Outlook: Rates Could Rise Sooner Than Expected

Before the war in the Middle East, many forecasts anticipated the next rate hike to arrive in late 2026 or early 2027. However, the potential for sustained inflation from higher energy costs could force the Bank of Canada’s hand, potentially bringing rate increases sooner than previously thought.

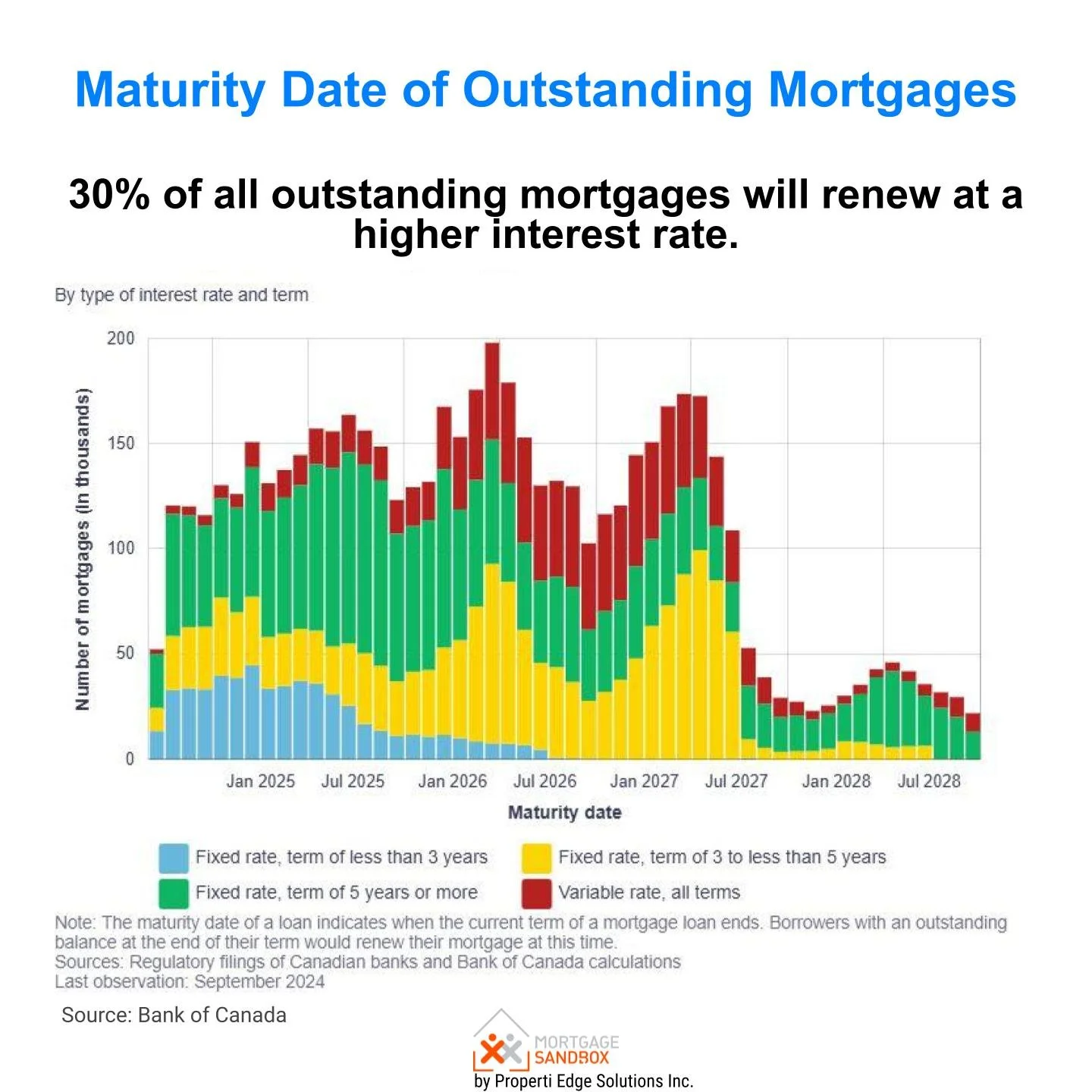

The 2026-27 Renewal Wave is Upon Us

At the same time, we are approaching an unprecedented period of mortgage renewals. Over one million mortgages are set to renew in 2026, many of which were locked in at historically low rates (below 2%) in 2021.

According to the Canada Mortgage and Housing Corporation (CMHC) and Bank of Canada analysis, these homeowners could face a significant "payment shock," with monthly payments potentially rising by 15% to 20% on average, and some may see increases of 25% to 40%.

How to Reduce the Impact of Higher Rates

If your mortgage is renewing in the next 12–18 months, you don’t have to wait and see what happens. There are proactive steps you can take today to manage your payments and reduce financial stress. The key is to start planning early.

Here are four strategies to consider right now:

1. Lock in a Rate Sooner Rather Than Later

With interest rates potentially rising due to global instability, securing a rate today can provide peace of mind. Mortgage brokers and lenders typically allow you to lock in a rate up to 120 days (or 4 months) before your renewal date. If rates increase during this period, you’ll be protected. Conversely, if rates decrease, you can often negotiate a lower rate closer to your renewal date. If your lender doesn't offer a 4-month rate lock, consider speaking with a mortgage broker for assistance.

Locking in a rate does not mean you are obligated to accept it. If interest rates decrease by the time of renewal, you can choose to take the lower rate instead. Essentially, a rate lock functions more like a rate cap, which sets an upper limit on the interest rate you will receive when it’s time to renew.

2. Fixed Rate Blend and Extend

If your fixed-rate mortgage is set to renew in late 2026 or 2027, and you're not within the next four months, consider a blend-and-extend option with your current lender. A blend-and-extend mortgage in Canada is a refinancing option that enables homeowners to combine their existing mortgage rate with the current market rate, resulting in a new, blended interest rate.

At the same time, the borrower resets their mortgage term, usually back to a new five-year term, thereby avoiding significant prepayment penalties associated with breaking a fixed-rate mortgage early.

For those facing renewal in 2027, this approach could lead to an increase in the overall blended rate. For example, blending a 2% mortgage rate from 2022 with today’s 4.5% market rate allows you to take advantage of today’s rates rather than waiting until the 2027 renewal date, when rates could be even higher.

3. Variable Rate Lock-in Before Renewal

If your variable-rate mortgage is set to renew in late 2026 or 2027, rather than within the next four months, you might consider a fixed-rate lock-in option with your current lender. This option allows borrowers with a floating-rate mortgage to convert to a fixed-rate mortgage for the remainder of their term, or even for a longer period. By locking in a fixed rate, you gain security since your mortgage interest rate will be frozen at the agreed rate, making future payments predictable. This option is especially beneficial when rates are expected to rise.

For those renewing in 2027, locking in a fixed rate now allows you to take advantage of today’s rates instead of waiting until your renewal date in 2027, when rates could potentially be higher.

4. Extend Your Amortization.

In Canada, mortgage amortization is the total time required to pay off a mortgage loan in full through scheduled payments. It represents the total lifespan of the loan, the timeframe it would take to pay the loan down to zero. Amortization is most commonly 25 years. A longer amortization lowers monthly payments but increases total interest paid.

If the new rates expected at renewal result in an uncomfortably high monthly payment, you can extend the mortgage lifespan while still paying the same mortgage interest rate to lower the payments. Stretching your total mortgage repayment period (for example, from 20 years to 30 years) can significantly reduce your monthly cash outflows.

5. Make a Lump Sum Payment

This option is available only to a small group of homeowners, but even a modest lump sum payment before you renew can help reduce your principal balance. This means you'll be paying interest on a smaller loan amount when you move to a higher interest rate, which effectively lessens the impact of the rate increase. However, to see a significant reduction in your monthly payments, you would need to make a substantial pre-payment.

6. Shop Around

It is essential to shop around for the best rates. Currently, we are likely at the lower end of the interest rate cycle, making it wise to lock in a fixed rate. While rates could drop in the future, the information available today suggests higher rates are more likely. Consequently, the appeal of a variable rate decreases if we are at the peak of the rate cycle. A variable rate might be more advantageous if we were at the top of the rate cycle, allowing you to benefit as rates decline.

For new mortgages and those renewing, it's important to note that your current bank may not automatically offer you the best available rate. So, be prepared to explore other options and negotiate. Consider obtaining quotes from other lenders or a mortgage broker to understand the potential benefits of transferring your mortgage.

If you inform your existing bank or lender that you’ve been comparing rates, they will likely lower their offer. Although it can be challenging to obtain a written offer from competitors, if you do manage to secure one, your current lender is likely to match that rate.

What Should You Do Next?

The potential geopolitical shocks mean that waiting until the last minute to address your mortgage could be a costly mistake.