Metro Toronto

Real Estate Trends and Price Forecast

HIGHLIGHTS

Metro Toronto home values have been volatile since 2021, but recent data shows signs of stabilization and even modest improvement in certain segments.

While year-over-year prices remain below last year's levels, conditions have shifted in favour of sellers over the past three months.

Multi-factor analysis identifies Metro Toronto as a moderate-risk real estate market, though risks vary by property type.

Mortgage rates have eased from their peak and continue to fall as the Bank of Canada remains in an easing cycle. Lower rates increase buyers' budgets and tend to stimulate property markets, though the full impact may take up to 18 months to materialize.

Economic uncertainty persists due to shifting immigration policies, trade wars, the war in Iran, and fluctuations in interest rates. All factors that influence future market dynamics.

This report covers:

What is the state of the Toronto property market?

Where are prices headed?

Should investors sell?

Is this a good time to buy?

1. What is the state of the Toronto housing market

Home Price Overview

Metro Toronto has a population of roughly 7.1 million and was ranked 15 of the best 100 cities in the world.

Toronto is an attractive city to live in for many reasons, including cultural diversity, economic opportunities, high quality of life, entertainment and recreation, world-class education, and good public transportation.

The Toronto real estate market is experiencing a dynamic shift. After a prolonged period of declining prices, recent trends suggest improving conditions for sellers.

GTA Detached House Market

The detached house market is currently balanced, with buyers and sellers holding equal negotiating power. However, conditions are trending in favour of sellers. Inventory levels have dropped compared to last year, which disadvantages buyers. Purchase demand has risen, and the supply of active listings has decreased.

Over the past three months, both benchmark and median detached house prices have increased, favouring sellers. Despite this short-term improvement, prices remain lower than they were one year ago, meaning buyers still hold an advantage on an annual basis.

We believe politicians hope to guide the market toward a typical annual real estate cycle with price growth in line with income growth.

Demand in the GTA has improved slightly, but affordability remains a challenge. Many people want to buy a home, but weak affordability has sidelined many potential buyers. New homebuyers struggle to get onto the first rung of the homeownership ladder, and high rates have prevented some existing owners from upgrading. Fewer households that want to move to a larger home can qualify for a new mortgage at current rates.

The low supply of active listings previously fuelled price rises. Today, while listings have dropped compared to last year, they remain higher than they were three years ago.

Metro Toronto New Construction Home Prices

The prices of new homes have been declining, meaning some homebuyers who locked in pre-sale contracts after 2021 may end up paying significantly more than recent buyers in the same development. Economic fundamentals suggest that these prices may continue to face pressure.

Pre-sales have declined notably, with apartment sales experiencing the largest decline.

While it is possible to negotiate price concessions with developers, they often resist straightforward price reductions. Instead, developers typically try to redirect buyers' attention to the location of the unit (i.e., lakeview or higher floor), smaller deposits, amenities, and overall quality. If concessions are available, developers are more likely to offer extras first, such as an additional parking spot or storage locker, or upgrades to premium fixtures, before considering a lower sale price.

Does this concern you? Read the Pros and Cons of Buying Pre-sale Homes

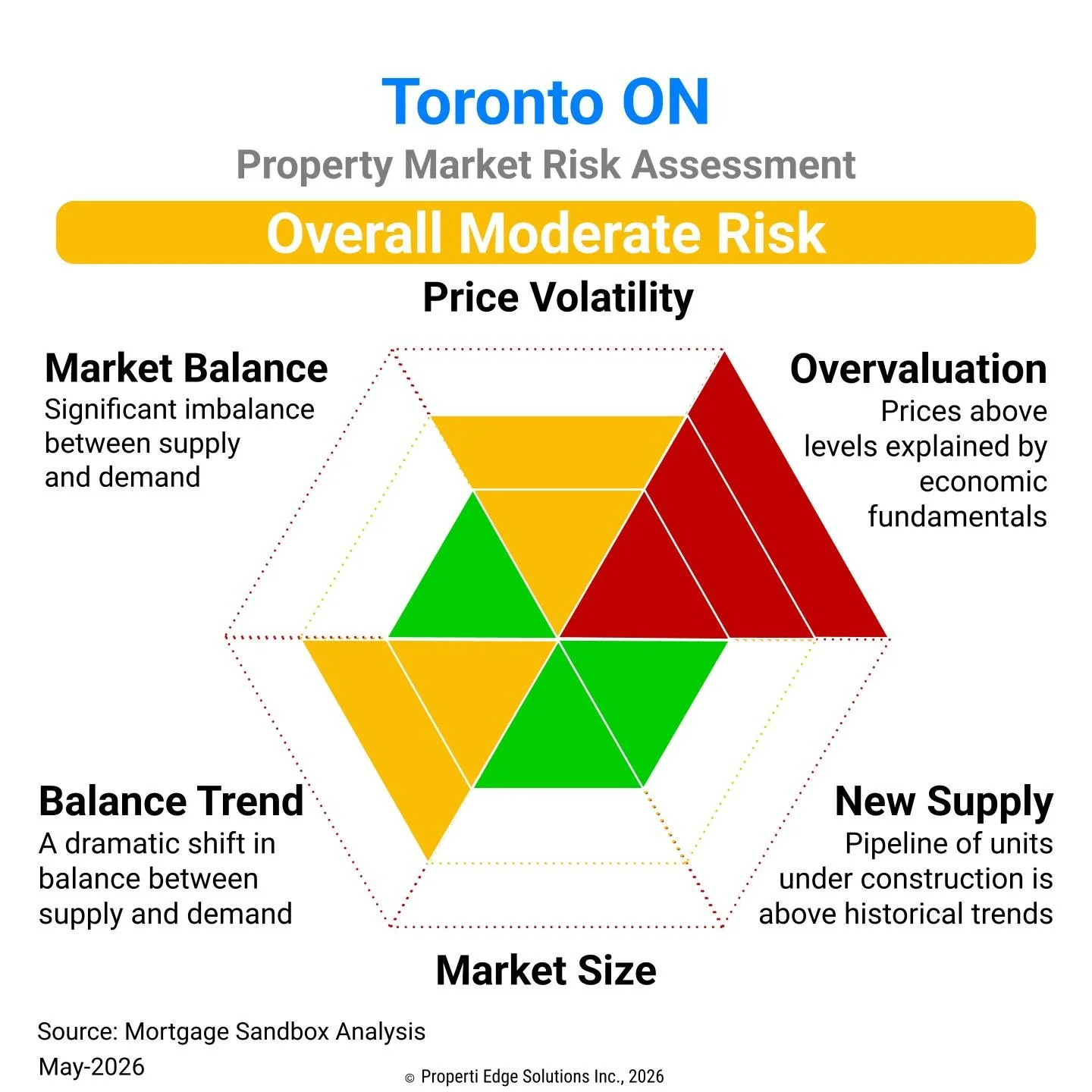

Market Risks

Based on Mortgage Sandbox Analysis, Toronto is at moderate risk of a significant market correction. Here are some key considerations.

Market Balance: The detached house market is balanced, and months of inventory are consistent with last year. The condo apartment market is also balanced with inventory consistent with last year.

Price Volatility: Prices in the detached house segment have been stable recently but remain disconnected from local income levels, indicating a potential bubble risk. Condo apartment prices are stable and considered affordable for most people, with the benchmark price within a sustainable range relative to median household income.

Construction Levels: Construction activity aligns with recent years, suggesting the market can likely absorb the current pipeline of completed units without significantly impacting prices.

Buyer Pool: Toronto is a large property market with a substantial number of potential buyers. Sellers should still be able to find interested buyers even in a slow market.

Interest Rates: Interest rates are currently lower as we are in the easing phase of the interest rate cycle. Falling rates increase property buying budgets and tend to stimulate property markets. It may take up to 18 months for the full effects of this easing to be felt.

Given the mixed support for these key market drivers, the city is assessed as being at moderate risk of a market correction, though condo apartments carry less bubble risk than detached houses.

|

Not sure about your bank's renewal offer?Try our mortgage offer evaluator Powered by Properti Edge |

Metro Toronto Condo Apartment Prices

After breaking records during the pandemic, condo apartment prices in Metro Toronto are now showing signs of stabilization. The market is currently balanced, with buyers and sellers holding equal negotiating power. Conditions are trending in favour of sellers. Inventory levels have dropped compared to last year, and purchase demand has increased while active listings have decreased.

Over the past three months, both benchmark and median condo apartment prices have remained flat. Year over year, prices remain lower, favouring buyers.

Purchases have dropped off compared with the previous three years, but inventory levels have also fallen. Typically, these conditions can lead to price stabilization or modest gains.

A report by CIBC and Urbanation in 2023 found that, on average, condo investors who completed their purchases that year faced negative cash flow each month.

Three years later, with declining condo values, rising costs, and lower rents, the case for buying condos to rent them out has likely weakened further.

Buyer activity in the condominium apartment market has improved, though there has been a shift toward lower-priced units. Larger floor plans and luxury condos may sit on the market for longer.

Metro Toronto Townhouse Prices

The townhouse market is balanced, with conditions trending in favour of sellers. Inventory levels are relatively unchanged from last year. Purchase demand has increased slightly, and the supply of active listings has edged down.

Over the past three months, the benchmark townhouse price has increased in favour of sellers, while the median price has remained flat. Year over year, townhouse prices remain lower, favouring buyers.

Affordability remains a challenge for first-time homebuyers

Toronto home prices are not broadly affordable. A first-time homebuyer household earning the median Metro Toronto before-tax income can obtain a limited mortgage. Even with a substantial down payment, they would struggle to afford a typical condo apartment. For most people, buying a home requires an inheritance or a very generous gift from family.

|

How much can you afford?Our mortgage calculator takes uses up-to-date mortgage rates and estimates the price of a home you can afford. Powered by Properti Edge |

What about the rest of Canada?

Read the Ottawa Forecast, Montreal Forecast, Hamilton Forecast, and the Vancouver Forecast.

2. Where are Metro Toronto prices headed?

There is significant uncertainty in the forecasts for 2027 and 2028. Recent trends indicate softening demand in some segments, rising inventory levels, and mixed price movements. Detached and townhouse prices have seen short-term increases but long-term declines. Apartment prices show a similar pattern. Potential price increases over the next few years may be limited unless there is a substantial change in underlying fundamentals.

Our 5-Factor Analysis

We assess five forces that help explain why several forecasters are anticipating softer price performance or potential price drops: Core Demand, Non-Core Demand, Supply, Government Interventions, and Consumer Sentiment.

How do we arrive at our forecast range?

Key External Variables

Beyond the 5-factor model, external factors could have a knock-on effect on the market. These include:

Will the war in Iran lead to higher mortgage rates, as the Bank of Canada is forced to combat inflation caused by higher gas prices?

As a result of the federal government's immigration policy pivot, how much lower will population growth be compared to recent years?

Will mortgage rates reset to a new normal range higher than Canadians have grown accustomed to, or will they return to pre-pandemic levels?

Will Canada's trade dispute with the U.S. lead to weaker economic growth or a recession that would further pressure housing demand and prices?

Methodolgy

At Mortgage Sandbox, we provide a price range rather than attempting a single prediction because many real estate risks can impact prices. Risks are events that may or may not happen. As a result, we review various forecasts from leading lenders and real estate firms. We then present the most optimistic estimates, the most pessimistic prediction, and the average forecast.

Would you like to learn more about real estate risk? We've written a comprehensive report explaining the uncertainty level in the Canadian real estate market.

Our forecast inputs:

3. Is this a good time to sell a Toronto property?

Annual Real Estate Cycle

The annual real estate cycle usually favours sellers in the first half of the year, and this seasonal pattern remains relevant in the current environment.

Current Strategies

From a seller's perspective, conditions have improved in recent months. With markets trending in favour of sellers, falling mortgage rates, and reduced inventory, now may be a better time to sell than in the recent past.

Professional Advice

Our analysis is at the macro, birds-eye level. There are nuances at the neighbourhood level, depending on the property type and condition.

Sellers should always consult a mortgage broker early to prioritize flexible loan conditions and reduce the risk of mortgage cancellation penalties. Also, consult more than one real estate agent. Sometimes agents will tell you what you want to hear to win the listing, then lower your expectations once you are bound to the contract. You will want a realistic assessment of which cosmetic changes are needed to increase the perceived property value, what similar properties have recently sold for, and where the market is trending.

Planning to Sell? Check out our Complete Home Seller’s Guide.

|

Need an estimated home buying budget?We will tell you what you can afford with transaction fees and taxes baked in, and fewer surprises. Powered by Properti Edge |

4. Is this a good time to buy Toronto real estate?

Annual Real Estate Cycle

The annual real estate cycle usually favours buyers in late summer and autumn, and this pattern is expected to persist into 2027 and 2028.

Current Strategies

Prices have stabilized in some segments and even increased modestly over the past three months. Supply has dropped, and purchase demand is rising. Mortgage rates are falling but remain relatively high compared to historical averages.

If you are buying your forever home and do not plan to sell for 10 years, the risks of buying now are lower than they were a year ago. However, if you are looking for a shorter-term investment, waiting could be prudent, as year-over-year prices are still down and further economic uncertainty remains.

If you are considering buying, be sure to drive a hard bargain and pay as close to market value as possible. Also, do not bite off more than you can chew when it comes to financing.

Professional Advice

Buyers should always consult a mortgage broker early in the process to obtain a pre-approval. Although current interest rates are easing, they are expected to rise within the next 9 to 18 months. With pre-approval, you can lock in a rate for 4 months before closing, helping mitigate financial risk.

It's advisable to consult multiple real estate agents. You want someone who will work with you on your terms. Buyer agents can boost their commission income by encouraging you to spend more or make decisions more quickly. Their earnings are tied to the total annual transaction volume, so they earn the same commission regardless of how much time they spend helping you.

This can lead to a perception that they prioritize closing the deal over finding a home that truly meets your needs. Additionally, while 90% of Canadians believe that owning property is a sound long-term investment, many agents offer little insight into the long-term investment potential of different areas or types of housing.

Planning to Buy? Check out our Complete Home Buyer’s Guide so we can walk you through the end-to-end process and get you ready to buy your new home!

|

Do you have a financing strategy?Try our strategy assessment to maximize your risk-adjusted investment returns. Powered by Properti Edge |

Here are some recent headlines you might be interested in:

Rate cuts seen as more likely next move for Bank of Canada: TD (Canadian Mortgage Trends | Apr 26)

Mortgages in arrears in Canada – what the numbers mean (Canadian Bankers Association | Apr 26)

Canadian Home Prices Fall 16th Straight Month on Higher Rates (Bloomberg | Apr 26)

Bank of Canada set to hold rates at 2.25% as oil shock likely short-lived (Reuters | Apr 26)

Market Outlook: Bank of Canada may cut rates despite hike expectations (BNN Bloomberg | Apr 26)

Canada's deflating housing bubble stymies wealth effect of booming stock market (Reuters | Apr 26)

Toronto's homes market stabilizes after 7 months of declining sales (Calgary Herald | Apr 26)

Here’s what the CREA now estimates the average Canadian home will sell for (BNN Bloomberg | Apr 26)

Like this report? Like us on Facebook.