Metro Hamilton Home Price Forecast

HIGHLIGHTS

|

This article covers:

Where are Metro Hamilton prices headed?

What factors drive the price forecast?

Should investors sell?

Is this a good time to buy?

1. Where are Metro Hamilton home prices headed?

Home Price Overview

Unfortunately for home buyers, Metro Hamilton prices have accelerated significantly in the past few months. Metro Hamilton, as defined by Statistics Canada, includes the cities of Hamilton and Burlington, and the town of Grimsby

People planning to sell their home will take heart in the fact that home values are at all time highs. Given the current recession and pandemic, sellers may want to push ahead and sell during the pandemic because there is no guarantee that home prices will regain the current highs any time soon.

A Coronavirus induced recession may inflict long-term economic damage and it is now the primary source of uncertainty for home values.

Metro Hamilton Detached House Prices

House price growth in Hamilton was accelerating in early 2020. The “soft landing” that government policymakers were targeting had become more elusive. We believe politicians were hoping to guide the market toward a typical seasonal real estate cycle with price growth in the range of 1 to 3% annually – in line with income growth.

Although the benchmark price is stable, the recent drop in the median home price is usually an indicator of downward price pressure.

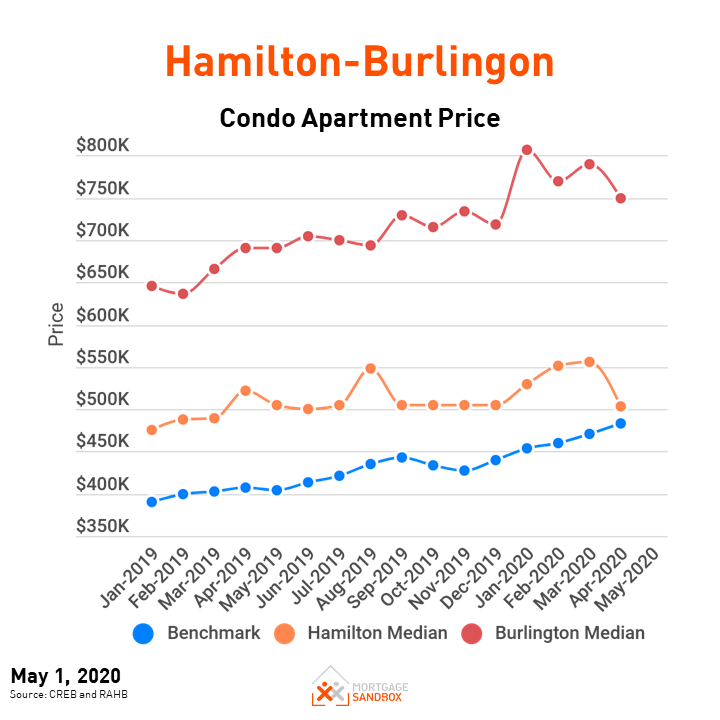

Metro Hamilton Condo Apartment Prices

Hamilton apartment prices have accelerated since 2017 and, today, a benchmark Hamilton-Burlington condo apartment is still affordable without help from family.

Entering the Coronavirus Recession, there is very little condo supply. When enough supply comes to market, the more expensive, higher quality, and larger (i.e., 2 and 3 bedrooms) apartments will drop in price, and this will depress the values downward for more modest condos.

At Mortgage Sandbox, we would like to see developers building more 4 and 5 bedroom condos. Not everyone can afford to put their family in a house, and for many parents work-related travel makes it difficult to stay on top of basic upkeep (i.e., mowing lawns, clearing eaves, shovelling sidewalks).

Still a challenge for first-time homebuyers

Hamilton's house prices have become much less affordable. A homebuyer household earning $75,500 (the median Metro Hamilton household before-tax income) can get a $310,000 mortgage. That’s enough to buy a benchmark priced condo, but buying a house is out of reach for most locals.

What about the rest of Canada?

Read the Toronto Forecast, Montreal Forecast and the Vancouver Forecast.

2021 Metro Hamilton House Price Forecast

At the beginning of 2019, the Canadian Real Estate Association predicted house prices in Ontario would rise only 3%. In the end, the benchmark Hamilton-Burlington house price rose by 9%!!!

For 2020, the average of the forecasts used in our analysis predicts a modest rise of 6% in 2020 and 3% in 2021. The lowest forecast predicted 2020 price growth of 2% and the most optimistic called for a 10% price appreciation.

Our forecast adjustment for COVID-19

None of our primary forecast sources have issued revised forecasts that incorporate the impact of a Coronavirus Recession, so we have adjusted the range of projections based on a rule of thumb provided by Moody’s Analytics. Moody’s Analytics specializes in products to help banks analyze loan and mortgage risks.

In a recent interview, Brendan LaCerda, a Senior Economist with Moody’s Analytics, estimates that each 1% rise in unemployment results in a 4% drop in home prices. Using this ratio, if Canadian unemployment reaches a sustained 11% (a 5% increase), then home prices could drop by 20%.

We have taken a conservative approach and adjusted the 2020 forecasts down by 10% (a prolonged 2.5% rise in unemployment) for the optimistic scenario and down 20% for the pessimistic scenario (an extended 5% rise in unemployment).

How realistic are these unemployment forecasts? On April 9th, the Canadian Parliamentary Budget Officer (PBO) projects Canadian unemployment will reach 15% by June 2020, and that stay as high as 13% by the end of the year.

The PBO may be underestimating the levels of unemployment.

The U.S. Fed projects unemployment in the United States is likely to reach a peak of 30%.

A recent research paper by Alex Bick, “Real Time Labor Market Estimates During the 2020 Coronavirus Outbreak” estimates that U.S. unemployment has already reached 20% and 21% of those who still have their jobs report a decline in earnings.

Joseph Brusuelas, the Chief Economist at audit firm RSM believes the U.S. is almost certainly facing a 20% unemployment rate now.

For a more thorough comparison of the Coronavirus Recession to the Great Recession and the Great Depression and their impacts on property prices, check out our recent article: “Should I sell my home today?”

At Mortgage Sandbox, we provide a price range rather than attempting a single prediction because there are many risks in real estate that can impact prices. Risks are events that may or may not happen. As a result, we review a variety of forecasts from leading lenders and real estate firms, and we then present the most optimistic estimates, the most pessimistic prediction, and the average forecast. Want to learn more about real estate risk? We've written a comprehensive report that explains the level of uncertainty in the Canadian real estate market.

Our forecast inputs:

2. What factors drive the price forecast?

Mortgage Sandbox 5 Factor Framework

At the highest level, supply and demand set house prices and all other factors simply drive supply or demand. At Mortgage Sandbox, we have created a five-factor framework for gathering information and performing our market analysis. The five key factors are affordability, capital flows, government policy, supply, and popular sentiment.

Below we will summarize how the five factors result in the current Hamilton forecast. We also have a report on the five factors driving home prices across Ontario.

Affordability

Affordability is a function of:

Home Price Changes: Changes in the market value of the desired home.

Savings-Equity: How much disposable after-tax income you’ve been able to squirrel away plus any equity you have in your existing home.

Financing: Your maximum mortgage is calculated using income (i.e., how much money you can put toward mortgage payments) and interest rates (how big are the mortgage payments).

Increased affordability raises buyer purchasing capacity and puts upward pressure on prices while dropping affordability has the opposite effect.

How have these changed lately?

Home Price Changes

Prices are rising across the Metro Hamilton. Prices growth reduces affordability and prices some potential buyers out of the market. In an ironic twist, this means rising prices create downward pressure on prices.

Savings-Equity

Rents were rising faster than incomes, so first-time buyers struggled to come up with down payments.

To add insult to injury, the stock market has dropped dramatically because of the pandemic, so anyone who managed to save a down payment and invested it in ‘blue chip stocks’ may now find out they’ll need to save for a few more years.

Existing homeowners benefited from price appreciation, so they had more home equity to use when buying a bigger home. That price gain may be short-lived as the Coronavirus is likely to depress prices.

Financing

Median Hamilton incomes have not changed materially, but employment levels are dropping.

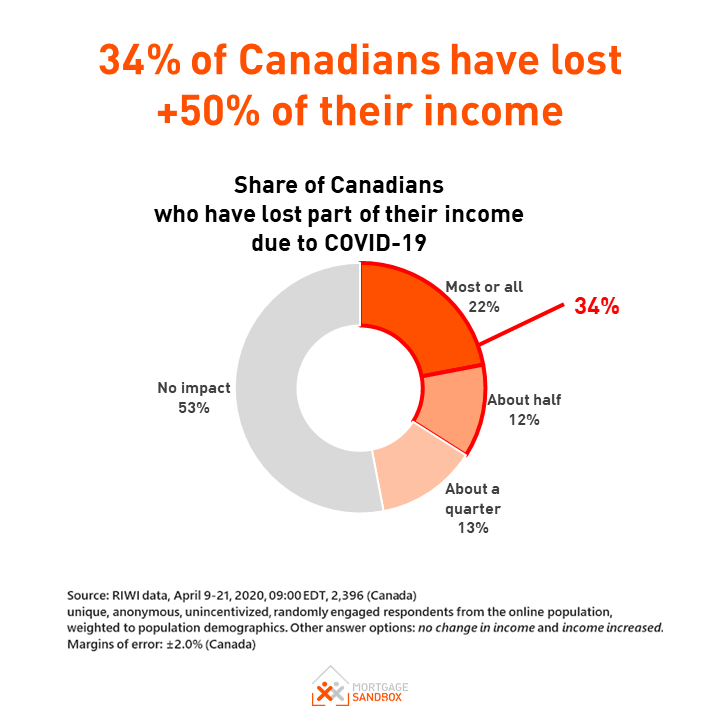

According to an April 21st article in Maclean’s Magazine, Canada’s unemployment rate rose to 22 percent. Apart from layoffs, many salaried employees who have not been laid-off have been asked to take pay cuts.

To mitigate the impact of job losses, the Bank of Canada has reduced rates dramatically, but mortgage qualifying interest rates have not fallen nearly as much.

Job losses from Coronavirus containment efforts are a more powerful force than low mortgage rates because without any income you can not qualify for a mortgage.

Overall Affordability

Despite lower interest rates, the Coronavirus Recession will reduce housing affordability because many people will lose their jobs, temporarily close their businesses, or accept pay cuts.

Capital Flows

These represent short-term investment, long-term investment, and recreational demand (i.e., homes not occupied full-time by the owner). Here is where foreign capital, real estate flippers, and dark money come into play. It also includes short-term rentals, long-term rentals, and recreational property purchases.

Capital inflows raise demand and put upward pressure on prices while capital outflows have the opposite effect. If capital sits invested in real estate nothing is bought or sold, it has no effect on the direction of prices.

Foreign Capital

Although foreign buyers are less of an influence in Metro Hamilton than in Toronto or Ottawa, current circumstances will likely reduce foreign investment.

Ontario implemented a 15% foreign buyer tax to reduce the distorting effect of Foreign Capital flows on local real estate.

Now with the travel bans that are part of Coronavirus containment efforts, we can expect there will be very little foreign investment in Canadian real estate.

Long-term Rentals

As it relates to our analysis, we expect domestic interest in long-term rental income properties will dry up so long as Coronavirus eviction bans are in place. The government has not developed an exit strategy for landlords with rent arrears when social isolation policies are lifted. How will tenants repay three to six months of rent arrears?

Rental investors will simply try to time any future property purchases for the end of Coronavirus containment period, and they will avoid properties with tenants who have outstanding rent arrears.

Short-term Rentals

We are watching short-term rentals closely because travel bans will effectively shut down short-term rentals for the next few months (Canada’s tourist high season). Hamilton and Burlington have a surprisingly large number of AirBnBs.

House Flipping

With Coronavirus containment efforts underway, house flipping will be very risky so we expect serial flippers will stay out of the market until they see a bottom to the market.

It may be 6 months to a year before the market finds bottom and the flippers emerge to pick up some bargains.

Dark Money

Dark money is proceeds of crime or money that is transferred to Canada illegally. This includes money earned legitimately that is illegally transferred from countries with capital controls (e.g., China) and legitimate earnings moved from countries who are the subject of international sanctions (e.g., Iran, Russia, and North Korea).

In order to hide the illegal nature of the funds, it is laundered in the real estate market. Sometimes the true owner of the property is hidden by using property is bought by a Straw Buyer and other times the property is owned by a shell company.

Sometimes a real estate agent or lawyer will accept the illegal cash to help the nefarious individuals hide its true origins. In 2015, a B.C. realtor was caught with hundreds of thousands of dollars in her closet, at home.

We see no evidence of a diminished role for dark money in local real estate.

Overall Capital Flows

The net effect of all the recent changes to Capital Flows will be to reduce inflows of capital toward Metro Hamilton residential real estate, and this will put downward pressure on home prices.

Government Policy

Governments were trying to engineer a ‘soft landing’, but now they are trying to protect against a housing crash by encouraging banks to allow borrowers to defer their mortgage payments up to six months.

COVID-19 Support Measures

Mortgage Payment Deferral

A typical mortgage deferral is an agreement between the borrower and the lender to pause or suspend mortgage payments for one or two months. For the Coronavirus, they have extended this for up to 6 months.

After the agreement ends, your mortgage payments return to normal. The mortgage payment deferral does not cancel, erase, or eliminate the amount owed on your mortgage. The borrower still accrues interest that will have to be paid.

A Canadian with a $250,000 mortgage who defers their mortgage by six months adds approximately $4,000 in accrued interest to their mortgage balance.

Eviction Bans and Suspensions

The Ontario government has suspended the enforcement of evictions indefinitely and Tribunals Ontario will not issue any new eviction orders until further notice. Sheriff's offices have been asked to postpone any scheduled enforcement of eviction orders.

Releasing Provincial Lands for Development

The provincial government is going to work with municipalities to reduce red tape and plans to sell up to 243 underutilized properties for redevelopment into housing but progress is slow. In January 2019, they sold some land in London. In April 2019, they sold a property in downtown Toronto that may create 700 homes.

Overall Government Influence

Overall, the government is now doing everything in its power to save lives while avoiding a property price crash. In a year or two, once, the COVID crisis has receded they will still be trying to bring affordability to the property market.

Supply

Supply comes from two sources.

Existing sales: Existing home sales are sales of ‘used homes’. They are homes owned by individuals who sell them to upgrade, to move for work, or some other reason. Thelocal Realtor’s Association only reports existing home sales.

Pre-Sales and Construction Completions: Most new homes are sold via pre-sales before the construction has started. These are predominantly apartments and townhomes. Data on pre-sales is private and difficult to find, but construction starts (reported by the government) are a very accurate lagging indicator of pre-sale activity.

Months of Supply of Existing Homes

Supply is rising so there is less upward pressure on prices.

Essentially, a market with 5 to 9 months of housing supply listed for sale is in a balanced market where neither buyers nor sellers have a distinct negotiating advantage. In a balanced market, home prices rise moderately in the springtime and usually dip in the winter, and year-over-year price increases tend to match rises in incomes (i.e., 1 to 2% annually).

Coronavirus mortality rates (short-term impact)

We know that older Canadians are more vulnerable, and the fatality rates follow a pretty clear trend:

People aged 80 and up have an expected 14.8 percent mortality rate

8 percent of those 70 to 79 succumb to it

3.5 percent of 60 to 69 year-olds are likely to pass away

In 2020, 45% of baby boomers will be over 65 years old, and in Metro Hamilton, roughly 18% of the population is over 65 years old, but in St. Catharines and Collingwood, more than 20% of residents are in their golden years. Contrast this to Metro Toronto where less than 15% of residents are over 65.

Obesity is also a COVID-19 risk factor and 26% of Ontario residents are obese.

The Coronavirus could cause an unusually large number of homes to come to market in areas favoured by retirees. Real estate prices in these areas may be particularly vulnerable.

Coronavirus short-term rentals sold or converted (short-term impact)

Travel bans will effectively shut down short-term rentals for the next few months (Canada’s tourist high season). The drop in bookings may force many owners of apartments primarily used as short-term rentals to sell their condo or repurpose it for long-term rentals adding a significant number of homes to the market in the next six months.

We surveyed over 50 Canadian real estate agents and 50% had observed a majority of short-term rentals being listed as long-term furnished apartment rentals and 25% expected AirBnBs owners would sell their homes to cash in the capital gains.

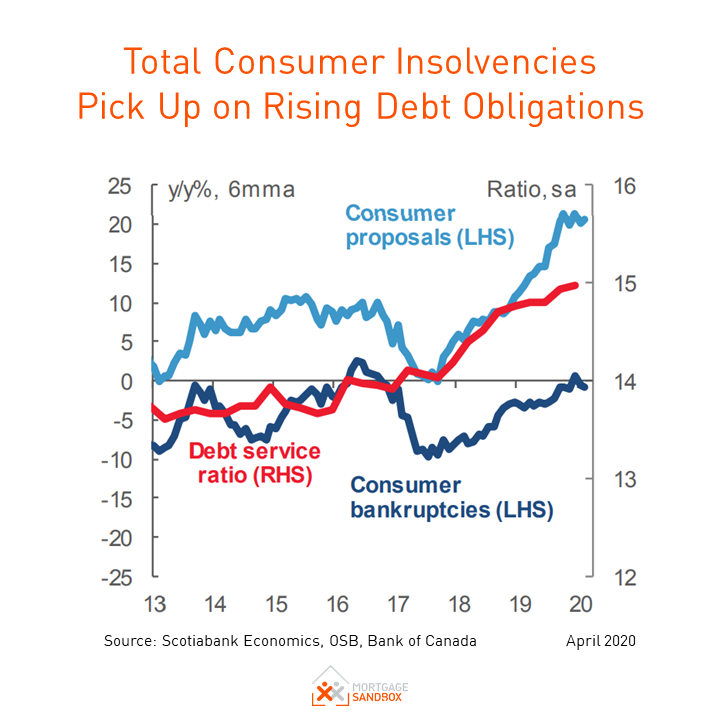

Mortgage Delinquencies and Foreclosures

The most recent data indicates that more Canadians are missing their monthly payments, and job growth has been healthy. Some economists have been warning of a recession, and even without a recession, it appears more Canadians are over-extending themselves. Surprisingly, the increases in delinquencies are led by Ontario and British Columbia, and not Alberta.

According to Equifax, the credit bureau company:

“Mortgage delinquencies have also been on the rise. The 90-day-plus delinquency rate for mortgages rose to 0.18 percent, an increase of 6.7 percent from last year. Ontario (17.6%) led the increases in mortgage delinquency followed by British Columbia (15.6%) and Alberta (14.8%). The most recent rise in mortgage delinquency extends the streak to four straight quarters.”

A recent survey by MNP reported a staggering number of Canadians are stretched to their limits:

“Over 30 per cent of Canadians say they’re concerned that rising interest rates could push them close to bankruptcy, according to a nationwide survey conducted by Ipsos on behalf of MNP, one of the largest personal insolvency practices in the country.”

Job losses from Coronavirus containment will worsen this situation. Although the CMHC can help Canadians via Canadian lenders offering options to defer payments, re-amortize mortgages, add interest arrears to your mortgage balances. It will not help overextended Canadians from their credit card debt nor will it protect Canadians who chose to finance their homes with private mortgage lenders. According to the provincial regulator, private lending accounted for around eight percent, or $10.6 billion of all Ontario mortgage transactions reported in 2017 by brokerages.

Baby Boomers Right-sizing?

According to a recent survey, almost half (49 percent) of all Ontario Boomers respondents said they plan to move into a smaller home as they near or enter their golden years, the highest rate among all provinces surveyed. Another survey from RBC says, “Over the coming decade, we expect baby boomers to ‘release’ half a million homes they currently own—the result of the natural shrinking of their ranks, and their shift to rental forms of housing, such as seniors’ homes, for health or lifestyle reasons.”

We prefer the term '‘right-sizing’ because most boomers selling a house are buying luxury apartments with large floor plans in buildings with shared pools, saunas, gyms, and party rooms. That hardly sounds like a step down.

As baby boomers begin right-sizing and list their million-dollar homes for sale, they will add supply in what is considered the luxury market. If not enough Gen-X and millennial buyers are to buy these expensive homes, there is a risk that this may depress prices at the top of the market, which will then compress prices for townhomes and condo apartments.

In the near-term, supply is tight, but in the medium-term, there are risks of excess housing supply.

Pre-sales and Completions

New Construction

There is a record number of homes under construction in Hamilton, and many are nearing completion. As these buildings complete in 2021 and 2022, and people move out of their rental or sell their current home, there will be new supply which should alleviate some of the pressure in the market.

Pre-sales

Metro Hamilton pre-sales, which are purchases of brand-new homes from developers. Typically, a developer must sell 70% of homes in a building before they can starts construction so housing starts are a good indicator of successful pre-sales.

Pre-sales were strong at the beginning of 2020 but we expect they will trend down as showrooms close during the pandemic. When social distancing measures are lifted developers will likely try to entice buyers with price discounts, move-in allowances, and cool amenities!

Popular Sentiment

Wait-and-See Strategy: There's no way of predicting popular sentiment, but as witnessed in the past two years, sentiment can shift quickly.

Nanos Canadian Confidence Index showed a noticeable drop in confidence mid-March, before a state of emergency was announced. Future index announcements will likely be worse.

3. Should Investors Sell?

From a seller’s perspective, there are more changes in the market that influence prices downward so now may be a better time to sell than in two years and the seasonal real estate cycle usually favours sellers in the first half of the year.

With Coronavirus containment efforts, open houses may be impossible. However, you can get a Realtor to help you plan small repairs and improvements to your home so that it will be ready when the real estate market thaws.

Sellers should always consult a mortgage broker early to prioritize flexible loan conditions and reduce the risk of mortgage cancellation penalties. Find out more about the benefits of a mortgage broker.

4. Is this a good time to buy?

With accelerating prices, some homebuyers who took a cautious wait-and-see approach in 2019 may have been priced out of the market.

Prices are still trending upward, but Coronavirus containment efforts pull prices down. It is likely that prices will be lower in 2021. Keep in mind that the seasonal real estate cycle usually favours buyers in late summer.

The wild card is the Coronavirus. At this stage, it's difficult to determine how much it will impact the market.

If you are thinking of buying, just be sure to drive a hard bargain and pay as close to market value as you can. As well, when it comes to financing, don't bite off more than you can chew.

Buying a home is a big decision, so check out Mortgage Sandbox's Canadian Homebuyer Guide so we can walk you through the end-to-end process and get you ready to buy your new home!

Here are some recent headlines you might be interested in:

Landlords among most vulnerable homeowners during COVID-19 pandemic (Global, Apr 21)

Virus-driven rate cut could add kerosene to housing market (BNN Bloomberg, Mar 3)

Canada must expose hidden company owners to end 'snow washing,' inquiry hears (CTV, Feb 26)

Assessing whether 2020 will bring a Canadian property tumble (CBC, Dec 19)

Like this report? Like us on Facebook.