Metro Victoria Home Price Forecast - Oct 2020

HIGHLIGHTS

|

This article covers:

Where are Metro Victoria prices headed?

What factors drive the price forecast?

Should investors sell?

Is this a good time to buy?

1. Where are Metro Victoria prices headed?

Home Price Overview

Metro Victoria house prices are near record highs, which has priced many potential home buyers out of the market.

People planning to sell their home will take heart because the pandemic hasn’t yet impacted home values. Given the current recession and a wave 2 of infections, sellers may want to push ahead and sell during the pandemic because there is no guarantee that home prices will regain the current highs any time soon.

The ongoing pandemic is the primary source of uncertainty for home values.

Metro Victoria Detached House Prices

The Victoria benchmark house price peaked in July. Government intervention in the market has successfully shielded the real estate market from the pandemic induced recession.

We believe politicians are hoping to guide the market toward a typical annual real estate cycle with price growth in the range of 1 to 3% annually – in line with income growth.

The rising median house price for the Capital Regional District (CRD) indicates shifting buyer preferences. A ‘benchmark’ Victoria house may be small for a family with two parents working from home and children taking online classes.

Our examination of the five factors driving B.C. home prices leads us to conclude it is unlikely that current values can be sustained through the next 12 months.

Overall, according to the CMHC, there is a moderate risk of a price correction in Victoria.

Metro Victoria Condo Prices

Metro Victoria benchmark apartment prices peaked in March have been falling recently. They appear to be falling out of favour as people seek larger living spaces where they can work-from-home.

We expect that Victoria developers will shift toward larger (i.e., 2 and 3 bedrooms) apartments to meet buyer preferences. As the supply of more generous floorplans comes to the market, it may depress the values for small floorplan condos.

At Mortgage Sandbox, we would like to see developers building more 4 and 5 bedroom condos because:

Not everyone can afford to buy a house for their family.

Many parents who work-from-home and have taken on child-minding find it challenging to stay on top of necessary house upkeep (i.e., mowing lawns, clearing eaves, shovelling sidewalks).

Many people prefer to live in higher-density neighbourhoods with all the essential amenities within walking distance.

Still a challenge for first-time homebuyers

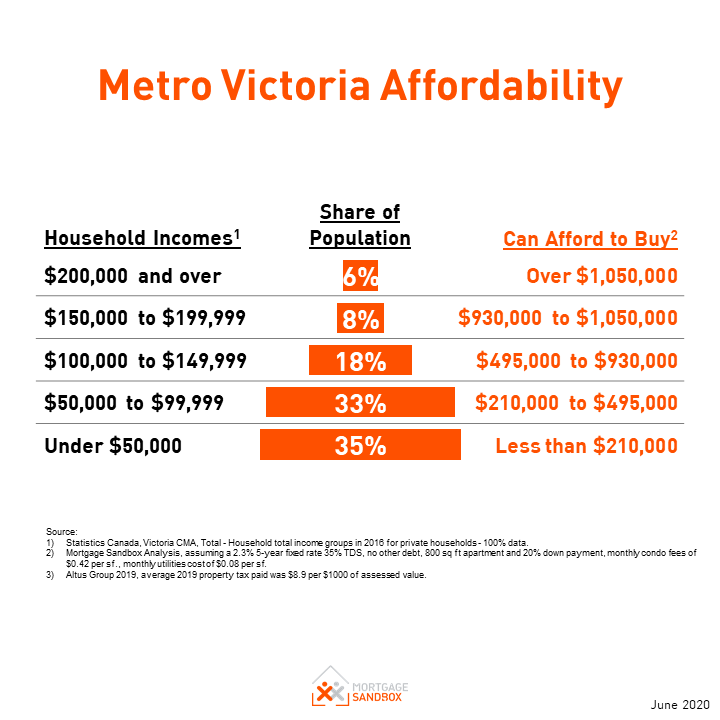

Metro Victoria's home prices are not very affordable. A homebuyer household earning $70,000 (the median Metro Victoria household before-tax income) can only get a $250,000 mortgage. For a homebuyer to purchase a benchmark priced condo, they would need to save hundreds of thousands for a down payment or receive a very generous gift from family. For most people, that is just not possible.

What about the rest of BC?

Read the Vancouver Home Price Forecast and Okanagan Home Price Forecast.

2021 Metro Victoria House Price Forecast

Peering into the future, some forecasters expect prices to continue rising while others expect prices to drop.

The BC Real Estate Association (BCREA) economist predicts Greater Vancouver prices will rise 7% in 2021. BCREA is a real estate industry advocacy group.

The highest forecast for Canadian home prices in a September Reuters poll of 16 economists was price growth of 10% in 2021, while the lowest prediction called for a 10% drop. Roughly half the economists anticipated a decline while half expected a rise.

Moody’s Analytics, who develop mortgage risk software for Canadian banks, predicts an 8.5% ‘peak-to-trough’ drop in Victoria.

CMHC, the government housing agency, predicts a ‘peak-to-trough’ average price drop across Canada between 9% and 18%.

There is no consensus among economists. Market sentiment and government stimulus have led to price acceleration and record home purchases even though most economic fundamentals have faltered.

Our advice to homebuyers embarking on the most expensive purchase of their lifetime, and sellers who want to get as much equity as possible out of their homes, is to place a little more weight on CMHC and Moody’s Analytics. They may be projecting lower values in the future, but:

CMHC sells insurance to banks that limits their losses if a mortgage goes bad.

Moody’s Analytics sells software to banks that helps them assess the risk of their mortgage portfolios.

Both organizations are unique to see market conditions across the regions and all the banks.

In the next section, we examine the five factors that drive these forecasts. They will help explain why some several forecasters are anticipating price drops.

For a more thorough comparison of the Coronavirus Recession to the Great Recession and the Great Depression and their impacts on property prices, check out our recent article: “Should I sell my home today?”

At Mortgage Sandbox, we provide a price range rather than attempting a single prediction because many real estate risks can impact prices. Risks are events that may or may not happen. As a result, we review various forecasts from leading lenders and real estate firms, and we then present the most optimistic estimates, the most pessimistic prediction, and the average forecast. Do you want to learn more about real estate risk? We've written a comprehensive report that explains the level of uncertainty in the Canadian real estate market.

Our forecast inputs:

2. What forces drive the price forecast?

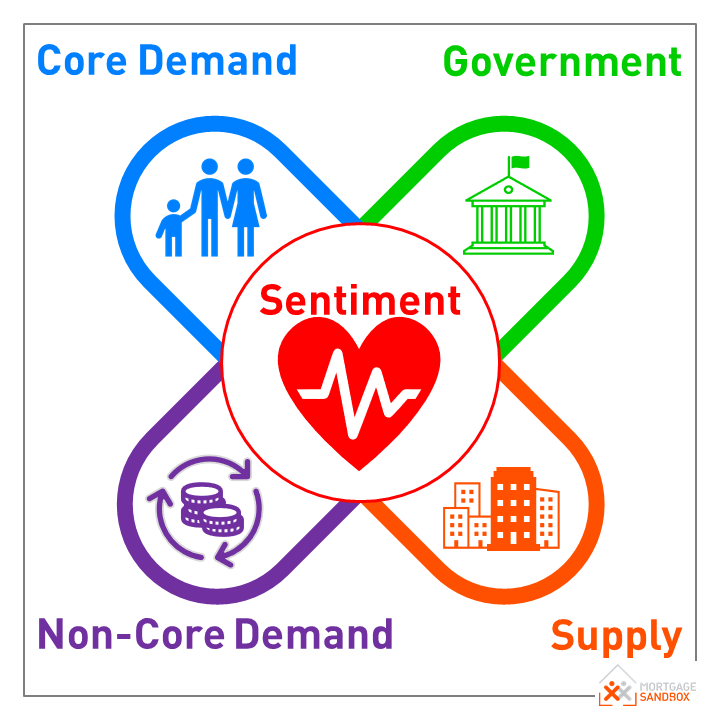

Mortgage Sandbox 5 Forces Framework

At the highest level, supply and demand set house prices and all other factors simply drive supply or demand. At Mortgage Sandbox, we have created a five-factor framework for gathering information and performing our market analysis. The five key factors are core demand, non-core demand, government policy, supply, and popular sentiment.

In the long-run, the market is fundamentally driven by economic forces, but sentiment can drive prices beyond economically sustainable levels in the short-run.

Below we will summarize how the five factors result in the current Victoria forecast.

Core Demand

Core demand is a function of:

Population Growth: The pace at which people are moving to an area. An average of roughly 2.5 people live in one household.

Home Price Changes: Changes in the market value of the desired home.

Savings-Equity: How much disposable after-tax income you’ve been able to squirrel away plus any equity you have in your existing home.

Financing: Your maximum mortgage is calculated using income (i.e., how much money you can put toward mortgage payments) and interest rates (how big are the mortgage payments).

How have these changed lately?

Population Growth

B.C.’s population is almost always growing, but the rate of growth is important for our analysis.

If population growth is the same or lower than in the past, then there is less upward pressure on prices.

At the moment, population growth is lower in B.C. As a result of ongoing COVID-19 related travel restrictions, we may observe lower growth through to the end of 2020 and into 2021.

READ: Fewer People = Less Demand : Easing Population Growth to Weigh on Housing, TD Bank

Home Price Changes

House prices are near records across Metro Victoria. Prices growth reduces affordability and reduces the pool of qualified potential buyers. In an ironic twist, this means rising prices create downward pressure on prices.

As a rule-of-thumb, homeownership costs are considered unaffordable when they exceed 40% of household income.

In March 2020, Victoria homeownership costs were 58% of the median household income. In other words, Victoria's home prices had exceeded economic fundamentals in a low interest rate environment before the Coronavirus impact.

However, given that house prices are already extremely unaffordable, the recent price increases will not make homes significantly less affordable.

Savings-Equity

Equity

Existing homeowners benefited from price appreciation, so they had more home equity to use when buying a bigger home.

Savings

Rents were rising faster than incomes, so first-time buyers struggled to come up with down payments.

The stock market has dropped because of the pandemic, so anyone who managed to save a down payment and invested it in ‘blue-chip stocks’ may now find out they’ll need to save for a few more months or years.

Financing

Mortgage Rates

The Bank of Canada has reduced rates dramatically, but mortgage qualifying interest rates have not fallen nearly as much. Also, lenders have tightened their rules so that the lower rates result in interest savings, but rates haven’t resulted in a large lift in home-buying budgets.

Employment and Incomes

In a March interview, Brendan LaCerda, a Senior Economist with Moody’s Analytics, estimates that each 1% rise in unemployment results in a 4% drop in home prices.

Using this ratio, a prolonged 2.5% rise in B.C. unemployment to 7.5% would result in a 10% price drop and a 5% rise in B.C. unemployment to 10% would lead to a 20% fall in values.

The ‘official’ B.C. unemployment figures unemployed people who are not looking for work (e.g., people who work in industries that have not fully reopened like tourism or hospitality). The true ‘effective’ level of unemployment is higher than the ‘official’ number.

Even after people get re-hired, they will need to be on the job for three months before they qualify for a mortgage pre-approval. Small businesses and commission salesforce have to show 2 years of consistent income to be eligible for a mortgage. Unless banks change their lending policies, 2020 will drag down their mortgage qualifying income until mid-2023 (when they file their 2022 taxes).

Homeownership Costs

In 2020, before factoring in the pandemic, Victoria had approved an increase in property tax and deferred it because of the pandemic. Victoria is now trying to cut spending so they can lower taxes for residents.

B.C. municipalities are legally prevented from running a deficit, so residents should expect further property taxes increases or reduced services to make up for the pandemic revenue shortfalls. If cities put off infrastructure and capital spending, then the deferred costs will eventually result in higher taxes.

B.C. has also seen a meteoric rise in home insurance, which for condo owners leads to higher monthly strata fees.

Property taxes and strata fees are factored into your mortgage affordability calculations, so an increase in taxes lowers home-buying budgets.

Overall Core Demand

Despite lower interest rates, due to the Coronavirus’ impacts, short-term core demand for homes will likely be much lower as we head into 2021.

Non-Core Demand

Non-core demand represents short-term investment, long-term investment, and recreational demand (i.e., homes not occupied full-time by the owner). Here is where foreign capital, real estate flippers, and dark money come into play. It also includes short-term rentals, long-term rentals, and recreational property purchases.

Since non-core demand is ‘optional’ (i.e., not used to shelter your own family), it is more volatile than core demand.

Foreign Capital

The following factors are likely reducing foreign capital inflows:

The annual B.C. speculation and vacancy tax rate is 2% for foreign owners and satellite families.

Since some foreign buyers were circumventing the tax using Canadian shell companies and straw buyers, the BC government will launch its corporate beneficial ownership registry in May of 2020.

Travel restrictions that are part of Coronavirus containment efforts.

We expect there will be relatively low foreign investment in Canadian real estate until travel restrictions are lifted.

Long-term Rentals

Rental investments are a significant driver of home prices.

During the wave 1 lockdown, the B.C. government suspended the enforcement of evictions for non-payment. Beginning September 1st, renters were then required to pay their monthly rent in full and pay any rent arrears accrued until the end of August.

For example, a tenant who typically paid $2,000 per month and couldn’t make their April, May, June rent payments would need to pay $2,800 per month for the 10 months beginning October 1st to pay back their arrears.

Some advocates now fear that there will be mass evictions and homelessness. How will tenants repay three to six months of rent arrears?

On the other side of the coin, if there are mass evictions, will landlords now struggle to find new qualified tenants?

As well, most International students are now barred from entering Canada.

All of these factors have led to falling rents across Canada.

Short-term Rentals

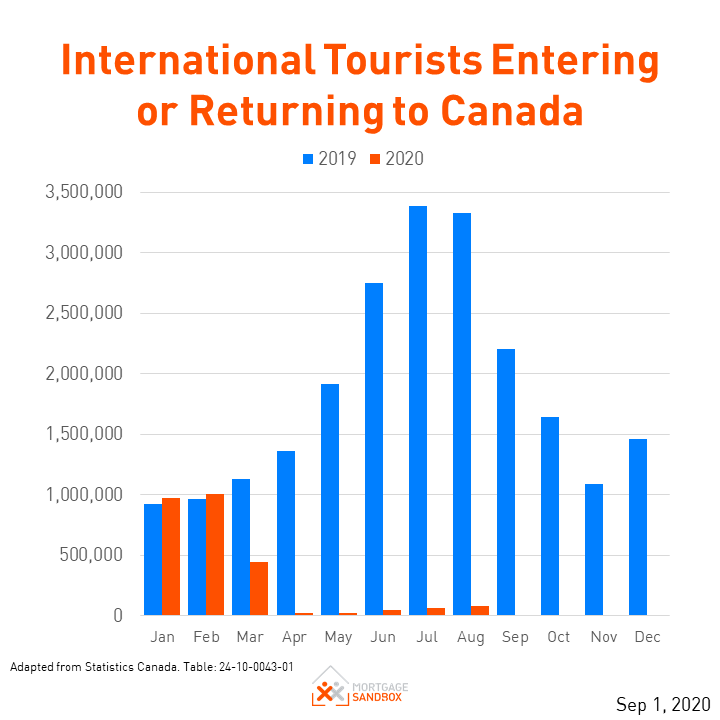

International travel restrictions will make many short-term rentals unprofitable for the foreseeable future. Statistics show that, since the travel restrictions were put in place, international travel to Canada has dropped 98 percent.

Fewer investors will be buying real estate for short-term rentals until travel restrictions are lifted.

House Flipping

With Coronavirus containment efforts underway, house flipping will be very risky, so we expect serial flippers will stay out of the market until they see a bottom to the market.

It may be 6 months to a year before the market finds the bottom, and the flippers emerge to pick up some bargains.

Dark Money

Dark money is the proceeds of crime or money that are transferred to Canada illegally. Dark money includes funds earned legitimately that are transferred illegally from countries with capital controls (e.g., China) and legitimate earnings moved from nations subject to international sanctions (e.g., Iran, Russia, and North Korea).

To hide the illegal nature of the funds, it is laundered in the real estate market. Sometimes, the property's true owner is hidden by using a Straw Buyer, and other times the property is owned by a shell company.

Sometimes a real estate agent or lawyer will accept the illegal cash to help the nefarious individuals hide its true origins. In 2015, a B.C. realtor was caught with hundreds of thousands of dollars in her closet at home.

We see no evidence of a diminished role for dark money in local real estate.

Overall Non-Core Demand

The net effect of all the recent changes will reduce capital inflows toward residential real estate for non-core uses, putting downward pressure on Metro Victoria home prices.

Government Policy

Governments have shielded Canadians and the housing market from the impacts of the pandemic induced recession using the CERB program, mortgage payment deferrals, and suspending tenant evictions. Most of these measures have now expired.

Mortgage and Housing Agency Tightens Mortgage Rules

Effective July 1st, CMHC has made changes to their mortgage rules that disqualify roughly 10 percent of potential homebuyers with Fair-Poor credit. The remaining buyers who qualify for a mortgage will be eligible for 10 to 8 percent less money.

The purpose of the change is to protect taxpayers from having to cover the costs of bad loans.

These changes effectively offset any benefit that lower qualifying mortgage rates provide.

COVID-19 Support Measures

Mortgage Payment Deferral

A typical mortgage deferral is an agreement between the borrower and the lender to pause or suspend mortgage payments for one or two months. For the Coronavirus, they have extended this for up to 6 months.

After the agreement ends, your mortgage payments return to normal. The mortgage payment deferral does not cancel, erase, or eliminate the amount owed on your mortgage. The borrower still accrues interest that will have to be paid.

A Canadian with a $250,000 mortgage who defers their mortgage by six months adds approximately $4,000 in accrued interest to their mortgage balance.

IMPORTANT: Statistics in May, show that 7 percent of British Columbia mortgage holders applied for mortgage deferrals. Mortgage deferrals expire after 6 months, and that means by October, many of these deferrals will expire. Unless these borrowers have found new work, they will fall into default.

Short-term Rental Regulation

In the City of Victoria, short-term rentals are only allowed in principal residences. Condos or rental apartments must have permission from the landlord or strata. Bylaw officers will now be able to issue a $500 fine for operating without a licence. Other fines include $250 for failure to include a business licence number in advertising and $350 for failing to designate a person responsible for the unit.

A recent court decision upheld a strata corporation’s restrictions on short-term rentals. In the case, the condo owner was ordered by a B.C. Civil Resolution Tribunal to pay $46,400 in fines.

Speculation and Vacancy Tax

At the end of 2019, the annual Speculation and Vacancy Tax rate on foreigners quadrupled from 0.5% to 2.0%

Beneficial Ownership Registry

BC’s Corporate Beneficial Ownership Registry came into effect in May of 2020. This may help to reduce dark money in B.C. real estate.

Overall Government Influence

Overall, the government is now unwinding many of the programs supporting home values through the recession. Compared to three months ago, there is now much less support from the government to maintain home values.

If prices continue to rise aggressively or suddenly drop dramatically, we should expect policy interventions to moderate the market. Unfortunately, our inability to predict government actions adds uncertainty to future home valuations.

Supply

Supply comes from two sources.

Existing sales: Existing home sales are sales of ‘used homes.’ They are homes owned by individuals who sell them to upgrade, move for work, or some other reason. The Victoria Real Estate Board only reports existing home sales and listings.

Pre-Sales and Construction Completions: Most new homes are sold via pre-sales before the construction has started. These are predominantly apartments and townhomes. Data on pre-sales is private and difficult to find, but construction starts (reported by the government) are a very accurate lagging indicator of pre-sale activity.

Rising supply releases the upward pressure on prices caused by demand.

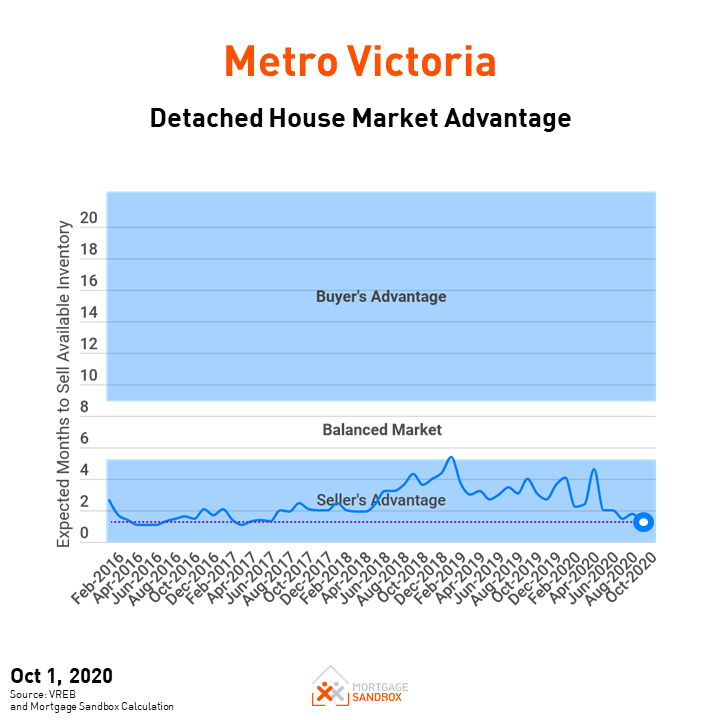

Months of Supply of Existing Homes

There are almost half as many months of home supply today as there was in January 2020.

While house listings are significantly lower, there are a record number of condo apartments for sale, and active listings are trending higher at an alarming rate. A flood of listings could cause an acceleration of price declines.

Coronavirus short-term rentals sold or converted (medium-term impact)

International travel restrictions will continue to make the short-term rental business difficult through to the end of 2021. The drop in bookings may force many owners of apartments primarily used as short-term rentals to sell their condo or repurpose it for long-term rentals adding up to 4,900 homes to the market.

We surveyed over 50 Canadian real estate agents, and 50% had observed a majority of short-term rentals being listed as long-term furnished apartment rentals. 25% expected Airbnbs owners would sell their homes to cash in the capital gains.

Mortgage Delinquencies and Foreclosures

Data indicates that more Canadians are missing their monthly payments, and it appears more Canadians are over-extending themselves. Surprisingly, the increases in delinquencies are led by Ontario and British Columbia, and not Alberta.

According to Equifax, the credit bureau company:

“Mortgage delinquencies have also been on the rise. The 90-day-plus delinquency rate for mortgages rose to 0.18 percent, an increase of 6.7 percent from last year. Ontario (17.6%) led the increases in mortgage delinquency followed by British Columbia (15.6%) and Alberta (14.8%). The most recent rise in mortgage delinquency extends the streak to four straight quarters.”

A recent survey by MNP reported a staggering number of Canadians are stretched to their limits:

“Over 30 per cent of Canadians say they’re concerned that rising interest rates could push them close to bankruptcy, according to a nationwide survey conducted by Ipsos on behalf of MNP, one of the largest personal insolvency practices in the country.”

Although the CMHC can help Canadians via Canadian lenders by refinancing mortgages, it will not help overextended Canadians who chose to finance their homes with private mortgage lenders.

Antrim, one of the larger private lenders in B.C., has lent $500 million in British Columbia. 1,529 of their mortgages are in Metro Vancouver, with an average weighted interest rate of 8%. Most of their mortgages need to be re-approved every 12 months.

Baby Boomers Right-sizing?

According to a recent survey, 26 percent of B.C. Boomers who own their home had most of their retirement savings tied up in real estate.

Nationally, many Boomers want to live in their homes forever, but that will not be possible for many. Most of them are not on track to have enough savings in retirement. The Coronavirus Recession won’t help.

An RBC survey says:

“Over the coming decade, we expect baby boomers to ‘release’ half a million homes they currently own—the result of the natural shrinking of their ranks, and their shift to rental forms of housing, such as seniors’ homes, for health or lifestyle reasons.”

We prefer the term '‘right-sizing’ because most boomers selling a house buy luxury apartments with large floor plans in buildings with shared pools, saunas, gyms, and party rooms. That hardly sounds like a step down.

As baby boomers begin right-sizing and list their million-dollar homes for sale, they will add supply in what is considered the luxury market. If not enough Gen-X and millennial buyers are to buy these expensive homes, there is a risk that this may depress prices at the top of the market, compressing prices for townhomes and condo apartments.

In the near-term, supply is tight, but there are risks of excess housing supply in the medium-term.

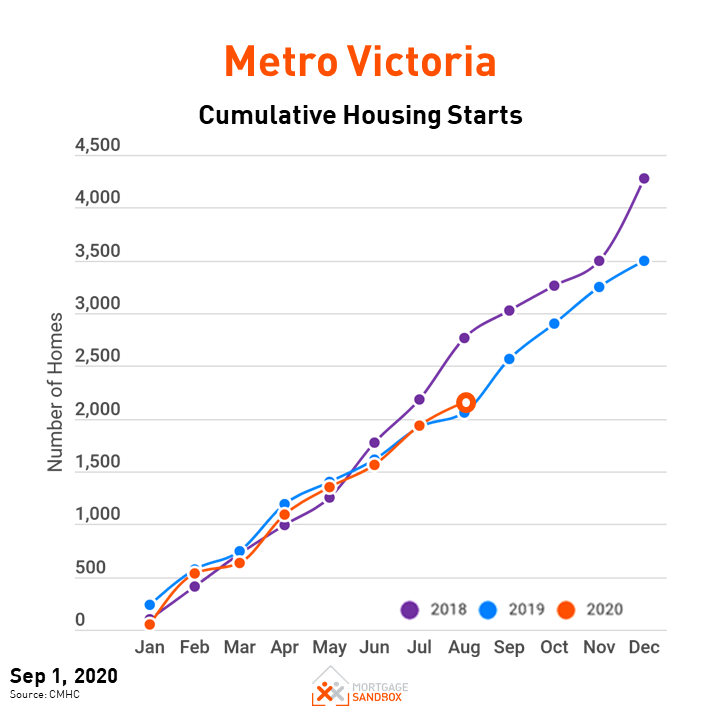

Pre-sales and Completions

New Construction

2020 has seen record home completions, and the number of homes under construction is nearly at record levels. As buildings under construction complete in 2021 and 2022, and people move out of their rental or sell their current home, this new supply should alleviate some of the upward pressure on home values.

Pre-sales

Metro Victoria pre-sales are purchases of unbuilt and completed brand-new homes from developers. Typically, a developer must sell 70% of homes in a building before they can starts construction, so housing starts are a good indicator of successful pre-sales.

Pre-sales have been comparable to 2019, but they look sluggish if compared to 2018.

Popular Sentiment

There's no way of predicting popular sentiment, but sentiment can shift quickly, as witnessed in the past two years.

Canadian Consumer Confidence

The Ipsos-Reid and Nanos Canadian Confidence Index has shown a noticeable drop in confidence. “Consumer confidence among Canadians has improved significantly, buoyed by positive views on real estate. Confidence has recovered remarkably well when compared to the 2008 Great Recession. It would appear that sentiment is the primary driver of real estate market activity because the other four drivers are materially weaker.

Coronavirus Containment

If B.C. cannot contain the second wave, we expect localized restrictions and lockdowns will depress sentiment.

Prime Minister Trudeau has clearly stated that the second wave of Covid-19 is already happening across Canada in a nationally broadcast address. Chief Public Health Officer Dr. Theresa Tam has said that "Unless public health and individual protective measures are strengthened, and we work together to slow the spread of the virus, the situation is on track for a big resurgence in a number of provinces."

A study headed by Dr. Kristine A. Moore, medical director at the University of Minnesota Center for Infectious Disease Research and Policy, warns that the pandemic will not be over soon and that people need to prepare for possible periodic resurgences of disease. Optimistically, a vaccine will not be widely available until mid-2021, and 70% of the population would need to be infected to provide herd immunity. Unfortunately, more than 30% of the population have conditions that make them vulnerable.

3. Should Investors Sell?

From a seller’s perspective, more changes in the market that influence prices downward, so now may be a better time to sell than in two years, and the annual real estate cycle usually favours sellers in the first half of the year.

Sellers should always consult a mortgage broker early to prioritize flexible loan conditions and reduce the risk of mortgage cancellation penalties. Find out more about the benefits of a mortgage broker.

Planning to Sell? Check out our Complete Home Seller’s Guide.

4. Is this a good time to buy?

Homebuyers who waited now benefit from lower interest rates and prices that are unchanged from a year ago. They can now get a larger mortgage and buy more house with their larger buying budget.

Coronavirus containment efforts may make it more difficult to visit a bank or view homes. However, if you are considering a purchase, you can get a mortgage pre-approval from a mortgage broker and ask a Realtor to monitor the market, all without leaving your home. Then you’ll be ready when the ‘fog clears.’

Looking forward to 2021, prices are unlikely to rise dramatically, so buyers shouldn’t feel the need to rush to an offer. Also, keep in mind that the seasonal real estate cycle usually favours buyers in late summer.

If you want to buy, be sure to drive a hard bargain and cover your bases with smart and educated decisions. Don’t bite off more than you can chew.

Planning to Buy? Check out our Complete Home Buyer’s Guide so we can walk you through the end-to-end process and get you ready to buy your new home!

Here are some recent headlines you might be interested in:

CMHC: Mortgage Deferrals On Toronto Real Estate 12%, Vancouver 11% (Better Dwelling, Oct 14)

Greater Victoria real estate sales remain hot through September (Victoria News, Oct 4)

Archives: When Vancouver real estate prices were falling in 1982 (CBC, Aug 18)

Like this report? Like us on Facebook.